Hello and good morning to everyone at least in europe and good evening to steve keane who is in australia and a little advanced on time this day we are very happy to have you in this discussion today which is the first new forum for new economic economy uh shortcuts that we're doing this year 2022 and uh it seems quite natural to have uh something like This book discussed in this format and at the forum new economy as the book that we will be talking about is uh the one that steve keane has published recently and

it's called new economics a manifesto and it's about trying to to get around this what could be a new economic theory what could be a new economic thinking a new economic paradigm criticizing the old ones and putting Not very much at the forefront uh the main obstacles the main uh the main problems of the old and neoclassical model steve keane i don't have to introduce you largely most of people know you you're a professor of economics from australia you've written this very popular book on debunking economics which was a sort of a first step leading

to the current book and As you told me you have started and it's very important for for economists to do that at some time sometimes uh to try and entertain into politics um the candidate candidate for the new liberals party in australia for the senate and for the elections will come up in spring you may Perhaps say some words on that in a in a minute uh i would shortly introduce uh also both other panelists who will comment on on your introduction and petriform prime director and very famous known for a lot of inspiring ideas

around new economic thinking and peter buffinger member of the council of economic advisers or wise men Um which is funny because now you're a former wise man but maybe you're not wiser than before or even the wiser now than before so very happy to have you from university of wurzburg and i just reminded the panelists that one year ago we had a discussion with also peter and greg manchu about His famous and his very important and influential marco economics textbooks and a very lively debate with greg mancu trying to defend his thinking um i think

we will go and make another step today um trying to find what is wrong about this and what may be a new answer so um very happy to give um for you to take over steve and give us The first view of your book and then we'll start the discussion with uh the panelists thank you okay well let's talk so i'm sharing my screen now can you see my screen uh yep yep good okay and i'll actually minimize i might actually move the uh the participants bar down the bottom which seems to take up less

of my presentation space so this is the um those my current publications including A uh a couple of cartoon books and this is the new economics and uh the two websites supporting my patreon website of course which is where i publish most of my work and where i'm supported and then prophecy with keen website which has got a role in the minsky as well and what i pretty much ask in the book is a bit of an inversion of the question that um was asked by veblen in the The previous one of the previous century

the end of the end of the the 19th century why is economics not an evolutionary science what i'm asking in 2022 is why is economics neither a science nor evolutionary nor truly revolutionary and part of the reasoning i go through in the book is that it doesn't undergo scientific revolutions uh practitioners of neoclassical economics will regard rational expectations of revolution that's Basically window addressing on the same paradigm they all accept the whole exactly the same paradigm we saw back with um jevins and and uh and and val ransome and marshall back in the uh the

late uh 1800s and if you look at thomas kuhn's structure of scientific revolutions what he sees a genuine science going through is a period of normal science where accepted ideas are extended then you hit an anomaly the anomaly is resolved by a Revolution which changes how you consider the science to be so for example in physics the quantum mechanical revolution overturned the previous maxwellian vision which so energy is being continuous suddenly have energy coming in in discrete coco units called quanta and then you have a new paradigm which comes along it becomes the normal science

then it strikes an anomaly and you continue Repeating this pattern over time and if you look at the neoclassical paradigm the same idea of utility maximizing behavior profit maximising behavior uh optimization rising marginal costs falling marginal benefit etc etc it's all been there since the 1870s and there have been plenty of anomalies but never a revolution keynes came close but he was basically uh this is a kurdish power with john hicks coming in so the and the Anomalies themselves when we look at anomalies and economics they're not like in physics where they're repeatable experiments which

don't go away then there are unrepeatable events which can be ignored and forgotten which is what has happened and what you get as a result is that a new generation comes along which behave like true believers just like the people who taught them beforehand you don't get that generational change and What vip had to say about economics being helplessly behind the times in 1898 is still true in 2022 but of course it's much more critical now than it was even then now in that i have several pass to the book so i'll go through each

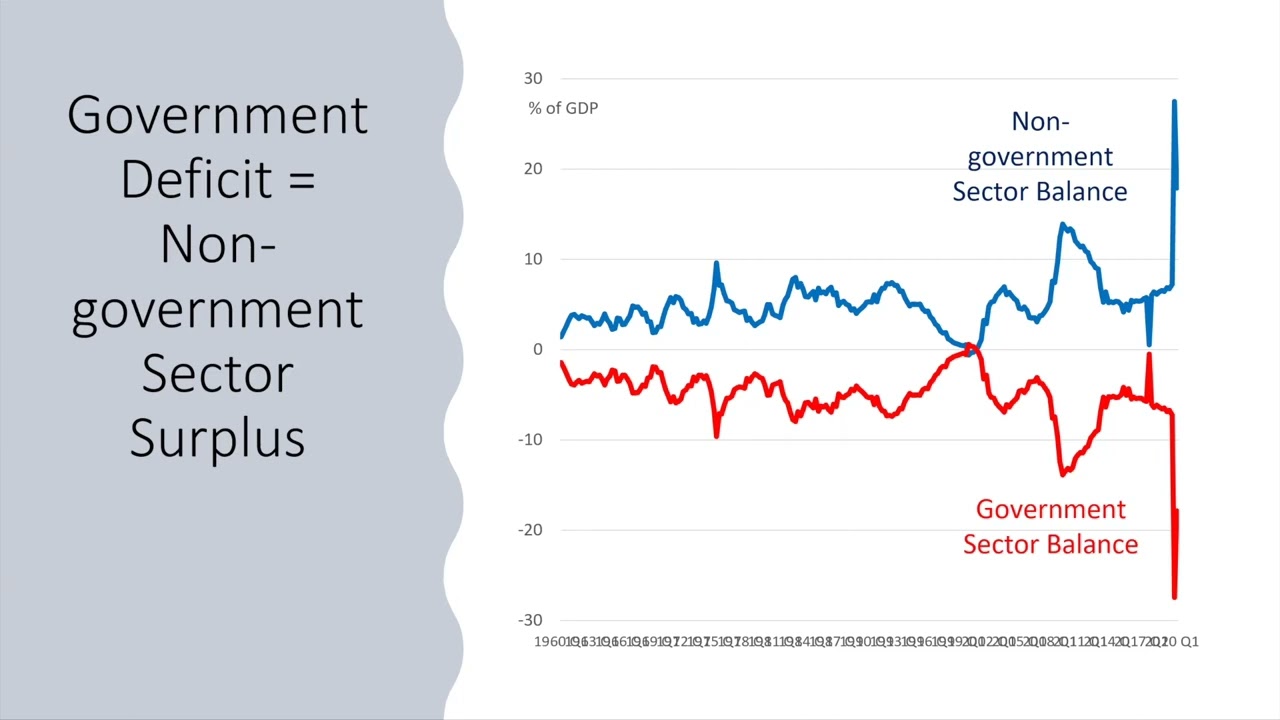

of the major segments so i spent about 65 pages talking about why money matters and if i'd draw it down to its essence as to why money matters it's because one of the few things that everybody accepts in Macroeconomics is that aggregate expenditure is aggregate income they are identical um so that's it that's the accepted principle and using that principle negotiables normally rule out any role for money or credit but what i show by using a particular application of endogenous money theory is show that credit is part of aggregate demand now i won't go through

this table in detail this is what i call a more table after you know Honor of basel more but if you show expenditure on the horizontal and income on the vertical then you can show that the the the negative section the the the the diagonal there is aggregate expenditure by each group and if if credit is coming from the financial sector of the banking sector creating money which is then spent by the recipient then credit becomes part of aggregate income this is the only piece of maths i'm going to show in the Presentation but when

you put it together in a loanable funds world you credit cancels out in the real world of endogenous money what i call bank originated money and debt credit as part of aggregate expenditure and aggregate income and therefore you cannot leave the monetary system out where of course neoclassicals try to exclude it and just talk about real economics leaving out the monetary system so credit because it's so volatile it has the dominant Role in aggregate demand and aggregate income now what that means and i illustrate this with my minsky software which i've designed to fundamentally enable

system dynamics type tools to show how monetary economy works and this is a model i use in the book at one point actually might be in a companion book which i'll talk about in a moment and what i have here is uh if you if you know paul krugman krugman talks about patient people lending to impatient People and anxious making an intermediary and what i show is that that's the case uh then with the parameters i've set this model up with there's an increase in the amount of lending there's a decrease in the amount of

gdp now then very quickly and it takes me about 30 seconds to make this change uh but just what i first emphasized debt and gdp move in opposite directions in this model and there is no change in the amount of money the money Is the black line there with a few simple changes i grew across to the real world where the the bank does the lending to the so-called inpatient person um there's no role for the patient person or for reserves in the whole lending process and what you find is simply that structural change uh

lending and gdp move in the same direction and changing the amount of debt changes the amount of money so it's a fundamental change in How we think about the world when you bring in the role of credit and money as post keynesian economists have been arguing for decades so you you it is a complete transformation of economics to bring that in and credit plays an essential role because it is so volatile and i always go back to bernanke dismissing the role of credit in the explanation of the great depression but if you take a look

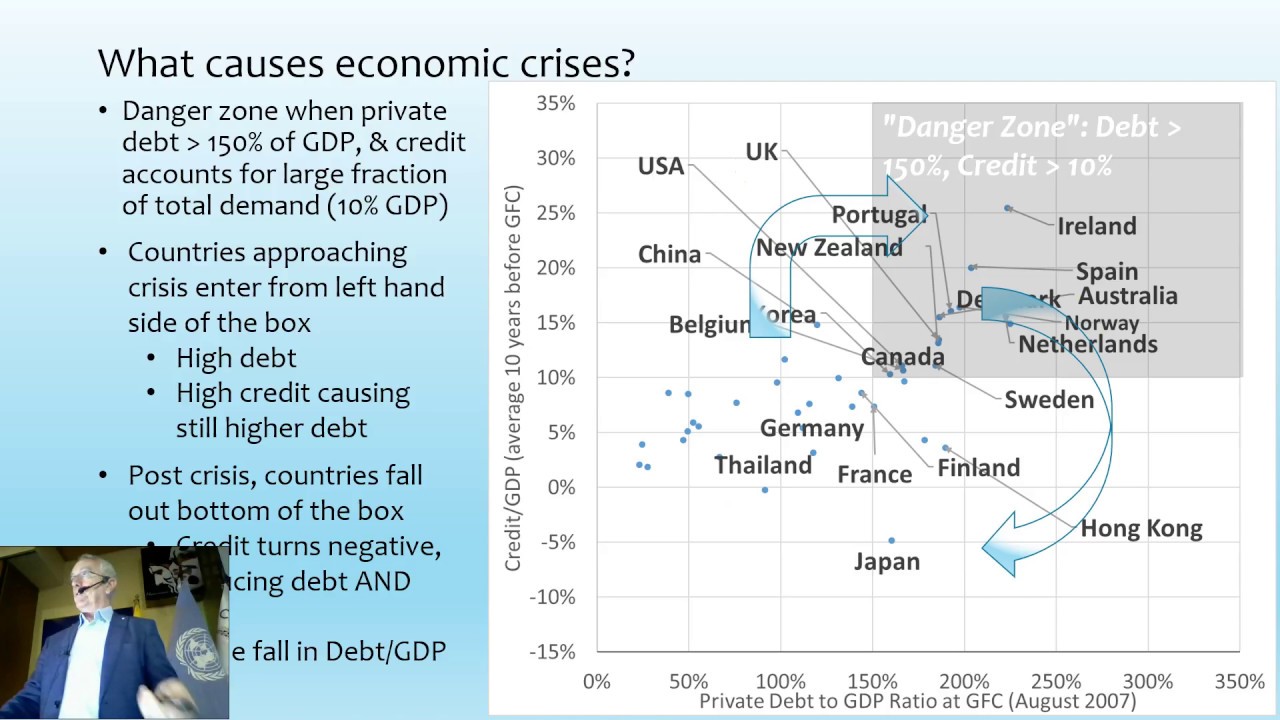

at data which actually was available to banker when he Wrote that book you look at the unemployment rate and credit which is the annual change in in in private debt uh over 1920 to 1940 you'd find a minus one eight one correlation between the two uh call me picky but i think that's a bit different from zero so it is a significant macro economic impact and it's even more obvious when you take a look at the period from 1990 to 2015 that show rising credit falling unemployment and vice versa enormous Correlation of 0. minus 0.93

and that should be even empirically that should be looked at by neoclassicals i've yet to see any of them consider it so they're basically ignoring the dominant factors in macroeconomics and i show how it's possible to bring it in in a logical coherent framework um the the probably the main one of the main elements which is novel in the book is the argument that you that there is a legitimate reason to say macroeconomics Should have indisputable foundations in the same sense that physics and chemistry and biology have indisputable foundations but they don't have to be

in fact they cannot be microeconomics because we understand complex systems these days and complex isn't that what we call emergent properties behavior can come out of a system which cannot be explained by any single component of that system or by extrapolating a single element up so What you can have is what i call the macro foundations of macroeconomics i don't put any maths in the textbook but i showed that if you take the employment rate the wages share of gdp and the private debt ratio and differentiate them with respect to time you get three strictly

true dynamic statements the employment rate will rise of economic growth exceeds the sum of change in the upwards labor ratio and population growth the wages share of gdp will rise Of wages growth faster than gdp and the debt ratio will rise if debt grows faster than gdp obvious and actually true statements you can turn that into a model very easily with a couple of genuinely simplifying genuine simplifying assumptions and what you get as i show in the book and also in a companion book is minsky's financial instability hypothesis with an added twist it wasn't predicted

by minsky that there before the crisis occurred there'd Be a period of diminishing cycles and then rising volatility afters which is what we saw during the so-called great uh great recession and that actually is a phenomenon known in chaos theory from fluid dynamics and it turns up as the foundational concept in macroeconomics you also get as you can see on this chart here the rising level of debt goes with a falling level of workers share of gdp whereas rising debt doesn't change the capitalist share of Gdp and that's another thing we see that rising debt

has gone hand in hand with increasing inequality and this is a causal explanation for that phenomenon the next major element i add is talking about the role of energy in production and if any if you any people are strictly economists they know that you have the cobb douglas production function describing output as being a function of technology times labor times capital both to powers that Sum to one um the leon tf model having output being a function of capital divided by a capital output ratio there's no explicit role for energy so what i've done there

is i explained in the book that energy is an essential input and when you put it that way you get a complete transformation to how we think about production and ironically i find myself actually liking something larry summers had to say which is an extremely rare phenomenon so let's Let's have a bit of a maybe larry can call in and take take the applause um but he talked about the financial crisis as being like a power failure and he said there'd be a set of economists who explained that only electricity if there was a power

failure it's only four percent of the economy so if you lost eighty percent of electricity you couldn't possibly lose more than three percent of gdp he said people would actually write papers like that and it Would be stupid but he said we know it was wrong even if we didn't quite know why it was wrong so what i want to illustrate is why this is correct because once you see energy as an essential input in production that if energy falls by 80 then so will gdp and the reason that matters as an example is that

if you take a look at the state where you're in right now how much other energy is contributed by non-carbon-based systems fundamentally Still mainly hydroelectricity it's less than 20 now if we're forced by an undeniable climate catastrophe let's say a collapse of the weather systems in the northern hemisphere uh which mean a breakdown in food production up there and nobody can argue against that this is climate change then what you will see is an eighty percent fall in gdp if you were lucky because if you take a look at the first level of uh the

red line is level Of renewables as a percentage of total energy production and it was only 14 back in 2017 it might be 18 now and if you take a look at what happens with change of energy versus change in gdp it is a virtually linear and one-to-one relationship so if there's a falling energy there will be a huge fall in gdp but because economists ignore it uh they've completely ignored climate change or they've they've totally misunderstood climate change and I frankly think that they're going to be guilty of eco side i think the mainstream

economists that have been involved in this work deserve to be prosecuted for eco-scientists once that's made into an actual crime as much as anybody in exxon or all the coal companies will be i deserve to because if you read naught house he says things like this and this is still how they think it is difficult to find major direct impacts on manufacturing mining Utilities finance trade in most service industries over the next 50 to 75 years that's because they can imagine you can produce output from those industries with that energy as an input and that

led to i'm assuming that 87 of industry would be unaffected by climate change and the ipcc released when richard tol was part of it repeats the same garbage i'm waiting to see what this year's report comes out and says but here There's a frequently asked question are there economic sectors vulnerable and they say manufacturing and services take place in controlled environments and are not really exposed to climate change they pretty much think only 13 of the economy is really going to expose and really only three percent is agriculture and of course we can ignore that

it's only three percent what would it matter if food production falls only lose two percent of the economy uh what i digress Uh and they do crazy things like this this is one of the data they make up their own numbers so all the empirical stuff you see and i go through this in the book in a fair bit of detail all the so-called empirical stuff is taking current data like this which is on the horizontal axis the deviation of the temperature of each average temperature of each state from the average for the united states

and on the vertical deviation of average income per capita From the average for the united states and if you fit a quadratic to that you get an extremely weak correlation and that's what they use as a prediction of the impact of climate change the correlation i get there gives me give me a coefficient of 0.00318 so for each degree and temperature change squared you get a point three percent fall in gdp and that's actually larger than naught house uses in his dice model so what it's implying is we have a six Degree increase in temperature

we'll just have an eleven and a half percent fall in gdp and what has this figure is even smaller and this actually ends up supporting trivializers like beyond longboard so longboard comes out and tells extinction rebellion and greta thundberg that all we're going to lose is two to four percent of gdp who cares now the point to me is how exactly can We imagine an economist helping with climate change if they're providing talking points for climate change deniers like lomborg and that's really the state of macri ethic macroeconomics when you read the genuine scientists on

this they're terrified about two degrees this is several major papers by hanson will steffen and tim linton saying anything around one to two degrees could be catastrophic for human life when they talk about a series Of tipping points which could each trigger each other and push us down to a hot house earth which will be antithetical to human existence on the planet so economists have trivialized this and said nothing to worry about with six degrees sinus is saying anything near two degrees and hold on to your hats we could lose the habitability of the planet

for human species we should do everything we can to avoid 1.5 degrees so mainstream economists Particularly norward house but quite a few others as well have delayed action on trial on climate change for 50 years and i think that's what's going to bring neoclassical economics unstuck they won't be brought unstuck anomalies in capitalism they will cause the collapse of capitalism and we will then have to pick up the pieces afterwards if we're lucky now uh and then why do they do us well they start from being denialists these are Some quotes i i think the

real starting point they have is that capitalism is such a flexible economic system just look at our supply and demand curves they can move really easily all over the over the blackboard so they're moddy you know the economy does the same thing isn't it hunky-dory and therefore capitalism can't be an existential threat that's how they start thinking about it and these are some quotes from this literature which is Just breathtaking human societies thrive in a wide variety of climatic zones yeah that's the current climate that's not the one we're causing non-climatic variables swamp climatic considerations

that's your starting point for most mostly respondents who are mainly neoclassical economists uh three degrees warming would be small potatoes and one of them i'm sure this is larry summers it takes a very very sharp pencil to see the difference between a World with and without climate change or with and without mitigation and that's the mental framework they're bringing to the picture and because the politicians listen to economists and are mainly trained by it that's what they actually believe but in the same paper there are three climate scientists interviewed these are these 19 people the

new so-called expert survey one of them refused to answer the question and saw them as absurd the other two in all the Scenarios they were given had estimates of damage just 20 to 30 times higher than the economists were looking at so we'll look talking about an order of magnitude maybe two orders of magnitude more damages coming out of climate change that economists are talking about whereas economists i'm saying the impact of climate change will be small relative virtually anything else you can name though so in my opinion is having looked at this work it's

not knowledge Economists should do better measurement they should simply shut up on measurement and accept what scientists have concluded and work out how to do something worthwhile now how did this stuff get published that was my real surprise when i saw it i thought i'd have to explain ramsey growth models and why they were inappropriate and stuff like that but barely even got to that point it's the assumptions that they make which are nonsense no other no Genuine science would have allowed the sort of assumptions that neoclassical economists accepted in these papers so we have

a fundamentally unscientific methodology courtesy of milton friedman and that's what's led to this impasse and economics will be the profession most responsible for the collapse of capitalism now we're talking for the future and i went look i'm also saying how do we do a new economics i want people to learn Complex systems analysis which means they have to learn as young students at least ordinary differential equations learn system dynamics and use my minsky software which i used extensively in the book forget about learning the city economics department so you're studying in your own time i'd

probably you won't get a lecture to oxford or cambridge about it but forget about that as an ambition um you'll be part of the solution rather than part of the problem If you take a new approach to economics and you get an interesting position outside economics by learning system dynamics and avoid the blame when climate change exposes neoclassical economics as fast because just as people outside economics think neoclassical economics is everything if you introduce yourself as an economist after this has happened you'll get the blame call yourself a system dynamicist instead and that's just thought

by the Way a link for those who want to go further than i cover in the book the book deliberately is written for except to be accessible to a non-technical audience it's still a fairly technical book but there are no equations in it this i've got a free book on that page which is about 250 pages worth explaining minsky and going to much more technical detail so i'd love to have students take a look at that and that will do me for my I'll hand back to ann and peter just so i can stop my

sharing yeah wow thank you very much stephen well this very very comprehensive critique and and um sum up the main ideas of your book uh going through nearly everything um you still gotta buy it yeah yeah i'm We we're not here to to make um but anyway i'll show it anyway uh so this is where you find all these bring it back a bit thomas is actually obscuring a bit yeah bring it back towards your face okay yeah whoops we've lost you oh that's okay that's it yeah try and make a copy um thanks a

lot and i hand over to anne Oh that's nice thanks so yes thanks ev so much steve um and can i say that the book is entirely accessible and thank god it doesn't have mathematics and system dynamic systems in it because for someone as simple-minded as myself that would be too much but it's a powerful book and it's very concise um it's not too long um and so i really do welcome it and i Welcome it particularly because of what steve has to say about economics and the environment um but it's equally true about economics

and the economic system the financial system um and and the devastation that is being caused and we i mean i knew steve before 2007 but you know we knew this was going to happen steve had produced these wonderful charts on the levels of private debt and how far they'd risen i Was obsessed at that point about sovereign debt and it was very clear to us that this was not sustainable that was going to blow up but when it did blow up we found ourselves really quite alone um you know central bank governors powerful economist influential

economists couldn't believe what had happened they were stunned they stood there it's relaxed quietly not knowing What to do and the problem with that is that the system far from being transformed by its failure far from being improved because of its failure actually consolidated itself i mean the bankers the financiers those who had gained massively from the bubbles and who gained from the bailout essentially um couldn't believe their luck you know none of them went to jail and they all Carried on and levels of debt are now higher than they were pre-2007 and i i

myself every day look at these numbers and can't believe that that the system is still operating essentially so we we know there's going to be another implosion another debt deflation to accompany the debt inflation that has been a feature of this last 10 years so um you know i do welcome this book and i do Hope it'll get read by a lot of people and and you won't be intimidated by steve's brilliant mathematics and systems i also just wanted to add one thing which is that one of the great crimes of economics is to neglect

its geniuses to neglect the people who really have the insights and steve is one of those one of those people that is neglected by the economics profession but goes way back um one of my heroes is john law Now john law was um was known as a a gambler he was brilliant mathematician he he would he was able to make calculations very very quickly so he was a superb gambler and speculator he was a womanizer and he was done for murder because um an obscure event that occurred in his life so you know he there

are lots of reasons not to rate Him but schumpeter says about john law who wrote about money back in 1705 and who understood money the nature of money he explained that money is the measure by which goods are valued the value by which goods are exchanged and in which contracts are made payable they are not they are it is not the measure for which goods are valued and for which goods are exchanged and and that was an insight in his book On on the land on money and trade first published in 1705 joseph schumpeter says

about john rule that i always felt he was in a class by himself he worked out the economics of his projects with a brilliance and yes profundity which places him in the front ranks of monetary theorists of all time says joseph jupiter so um you know these these are people that did have insights but that were marginalized and they Continue to be marginalized they're not given places in uni at universities and they're not published the sectarianism the ideological sectarianism and economics is a wonder to behold and and you know they should be ashamed of themselves

and and what it shows us is kind of timidity and and fear of mainstream economists occupying these positions of power in economics and unwilling to let them to let their Positions be undermined so steve is a breath of fresh air in this world of economics and i'm delighted to see this very accessible and interesting book and of course steve is one of my heroes for the reason precisely that he's exposed the fantasies the flaws in naughthouse's analysis and which is still accepted by i was listening to some sessions of the american economics association and i

heard nordhaus's Uh ideas being promoted by american economist so he's still in the center of this debate and that is terrifying for the for the whole of humanity uh never mind for the economics profession so thank you steve i think thank you anne i'll actually add one of my heroes as well the two of them cantalon and canay because again we've neglected them if we'd built an economics on their front and i do mention Them in the book it'd be a totally different economics because it would understand the role of energy and production and let's

actually quickly do a quick share of my screen just to make that point and for those of you who read andrew smith's wealth of notions tell me if the first paragraph here looks familiar this is the candle i'm writing well before smith land is the source or matter from which all wealth is drawn Man's labor provide the forms production wealth in itself with nothing but the food conveniences and pleasures of life that is almost verbatim what smith lifted and made labor the source and that just diverted us into the into the walls over the sources

of value when in fact the first people to get it right with the physiocrats if we started with them we would have a physically realistic economics so we don't just forget our heries heroes we assassinate Them and lose their ideas and they apply to to cancel on and to connect as much as it does to law okay thanks for heading uh peter yeah thank you very much thomas for inviting me again we had this very interesting discussion with mencu one year ago and now it's really fascinating to have the opportunity to discuss the book by

steve i will share my screen a little bit where is it So oh so okay can you see it yeah yeah we can yeah so let me start by saying i think this is a great book and it's really needed because it stimulates the discussion and in economics uh which is definitively needed um the main elements of the new paradigm that steve Proposes are a fundament for that the paradigm must be fundamentally monetary that the paradigm must present the economy as a complex system not as an equilibrium system the paradigm must be consistent with laws

of thermodynamics it must be grounded in empirical realism rather than the fantasy of as if assumptions about reality and it must be based on the techniques of system dynamics i think these are the key elements of the Paradigm but as i have only very limited time i want to focus on those elements but i also feel a little bit familiar with and i want to start with the with the element with the key requirement that a paradigm must be fundamentally monetary monetary and i fully agree here uh with steve i think here the revolution is

definitely needed um Because even after we've experienced experienced the financial crisis in 2008-2009 there has been no change in the in the dominant paradigm of neoclassics and i what i find here important is uh he is really my hero in this field because he very clearly differentiates between the two paradigms of what he calls real analysis which is more or less a neoclassical paradigm and with one Analysis and i think here he's really the founding father he's of course also the teacher of minsky who plays a very important role in steve's book unfortunately schumpeter is

has been very much misinterpreted in the neoclassical literature that's why we have just written a discussion paper uh which we call discovering the true schumpeter the truth which is the monetary champion Unfortunately in the standard literature he's presented as a real analysis from there so what are the main insights of schumpeter and of course the insights that you find in stevie's book well the key insight is that banks are not intermediaries but producers of purchasing power and from this of course derives the destructive power of excessive private debt which has led to the financial crisis

and as a positive Element of this insight is that there are no financial constraints for governments a point that is made in the book and which is the key insight of modern monetary theory so here i fully agree uh with mr eve and and fully agree that a revolution is is needed um what i also appreciate is to use accounting identities as consistency checks i think this is also very very Important i honestly speaking i must say i find the goodly more tables confusing but maybe it's due to the fact that i did not have

enough time to get in too much into these tables but i really have a question then to to steve the question is why does do these tables not include real assets i then i found really it's only the footnote and i i cannot imagine how one can Uh model the economy uh with these tables without real assets um i also do not fully agree with the idea that that jubilee would be non-inflationary um i think that jubilee which increases the net wealth of private households substantially would have a huge impact on their spending decisions and

so i Think this is such a dead jubilee you would have very inflationary effects which i don't think would would be a good idea so let me then go to the micro foundations of macroeconomics so steve argues there's no need to drill down to microeconomics anti-argus by simply taking card in definitions and turning them into dynamic statements we can build foundations of microeconomics i'm not really convinced that this is a Good idea that you can without behavioral equations make sensible macroeconomic models and so my question is are there really examples of empirical work which shows

that you can explain reality with such models for instance can you say something with these models about the impact of the pandemic and the reaction of fiscal and monetary policy to the pandemic this is something you can describe With these models and i must admit uh i still believe in the isl model which is very much criticized in the book i think the islm model is very much misinterpreted in the literature because it is a monetary model it has two dimensions the is curve is the goods market but the nm curve is an independent monetary

dimension and in this lm graph you have a central bank you have commercial banks Creating money you have private investors deciding to hold bonds or cash so this is a truly monetary model and i must say with this model it's very easy to explain what's going on in reality you can explain the covet shock you can explain the reaction of fiscal policy monetary policy and i think you can even explain uh modern monetary theory so i think maybe A second look at the slm model might be might be useful finally we have the neoclassics disease

and here as steve says the neoclassical theory of price being said by the intersection of supply and demand can't possibly correct and he very clearly explains how he comes to this to this statement but he also says we will not displace the neoclassical totem from People's mind without our own mathematical and visual alternatives and so i must say i don't see these alternatives i don't see in the book any simple frugal pedagogical way to provide alternative to the to the simple supply and demand analysis and i must admit uh as as a writer of a

textbook that the standard supply and demand schedules Also they have all their problems are very useful tool to explain many things that are going on uh in in the real world for instance what are the effects of a monopoly of cartels you can't explain what is effect of a minimum wage if you have a competitive labor market but you can also show what is the effect of a minimum wage if you have a monopoly on the labor market you can explain carbon pricing And all these things and throwing away the whole supply and demand apparatus

uh i think it's very difficult to say anything meaningful about many important issues in the real world so let me end by saying that yes we need a revolution but it would revolution is mainly need in macroeconomics where we need the monetary analysis as it is propagated by schumpeter it minsky instead of the real analysis neoclassics which still Dominates almost all the thinking of leading economies in this in this area in microeconomics of course new approaches are welcome but in my view they must be frugal and simple to be digestible for students so let me

end by saying that steve's manifesto really helps to stimulate the debate which is needed um here by the way this is luther which uh steve explicitly refers in in the movie but i think one should be careful not to Throw out the baby with the bath water thank you very much okay thank you i'll make some comments here if i can okay um first of all i see islam hang on a second what happened there because it's all there what's happened do this you're still there oh good pardon me i i just disappeared from i

must disappear from my screen from one or quite so what occurred there pardon me i forgot as if i could actually find My zoom window again it just disappeared so you can still hear me can you we can still see you and hear you i i can't i can neither see nor hear you which is a real problem because i wanted to show my screen and i can't actually i'll just bring up zoom and see if i can actually do it by going it's going to join it join the meeting i'm flummoxed i don't know

what's happened there uh okay leave webinar can there we go Come back i got it through zoom good okay um a whole lot of questions why did i use um what i call godly tables rather than um tea tables basically because it's impossible to do the uh guarantee that assets minus liabilities minus equity equals zero condition on every element of the t table uh i find them we have one graphic which is like a static snapshot at one point another graphic Which you might have it might have grown or shrunk another static view it's very

hard to show it dynamically whereas if i now that i can actually show my screen again this is i'll just show this particular model here this is a model of a a model where i combine the real economy as you're talking about a moment ago with the monetary economy this is the monetary model and double entry bookkeeping is by far the best Foundation for that uh but the remainder this is a goodwin growth cycle model which includes the role of private debt and uh which is actually just includes private debt as well so i bring

the two together so the flowchart elements here which is this section here is what gives you the uh the overall dynamics of the physical the real economy and it's linked with the monetary system up here the whole idea is to integrate the capacity in a model in a monetary way as Well as being able to model in a physical whereas so far we've we've really had them as two separate realms so this is two tools combined on the one canvas and in terms of saying you know we want a simple thing for our students i

think economics is too simple i'll give you a little joke here my my wife has no interest in the work that i do uh but i found out early on that she actually When she got first got married when she was actually studying an economics degree and i asked her why did you choose economics her answer was because it was easy and if you want to pass an exam in microeconomics it's just you know where do the lines intersect and what other lines you have to add and so on to answer it it's too simplistic

if you see what engineers do in first year it trivializes what economists do and i Think this is to our detriment engineers use things like system dynamics uh when a package is called simulink in particular which is this is this minsky is is a relative of that they're using differential equations they've got dynamics going on we should be modeling the economy the way it is not with statics time slots like supply and demand curves and isolam so we completely disagree on that front uh also islm if you read um Hicks and the the key papers

to read in the 1935 wages and wages and profits the dynamic problem and then islam and explanation in 79 uh 8081 he tells you that it was a neoclassical model he derived it before he read keynes and he realized in 1881 after many conversations with paul davidson uh that it was not at all keynesian and that equilibrium was incompatible with kansas own thinking so i'm afraid we've got to agree to disagree on islam i Think it should be thrown out and so does john hicks who developed it if you read that if you read please

read isil am an explanation in the journal of post-keynesian economics in the 80 i think it's 1881 or 8182 edition that's a pity that uh hicks published there because it was the thank you to paul davidson for opening his eyes over the whole thing but it meant neoclassical economists never read never read hicks's own Uh dismissal of his own tool and saying we shouldn't use it unless equilibrium is is these in only the very few situations when equilibrium actually applies so we do have a fundamental disagreement there and also in terms of things like microeconomics

and so on um yes i'd be happy if you taught microeconomics if it was honest now if you take a look at supply curves where what is the supply curve supposed to be it's supposed to be the marginal cost Curve above average minimum average cost okay so it's marginal cost curve when you look at the empirical data and this has been done by people up to an including alan blinder in the in the late 90s and i quote this in the book as well alan blinder went and surveyed what it turned out there was something

like about 15 of american manufacturing firms and he found that 89 of them reported constant or falling marginal costs now in that situation you cannot Have a supply curve it's gone there's no honesty in microeconomic textbooks that teach that and it's the only excuse for it is ignorance but funnily enough alan blinder doesn't have that excuse because he learned that and i had a bit of fun and i'm rewriting debunking economics on this front for the third and final edition i hope to start later this year in his textbook he does not mention his own

empirical research he simply Regurgitates the whole idea about diminishing marginal uh productivity and therefore rising marginal cost uh saying and actually claims it was found by observation rather than imperiological deduction when in fact it was supposedly a logical deduction from the idea of fixed inputs and variable inputs but in the real world it doesn't apply so what we teach in my textbooks is a fallacy and i'm not i think it's about time we were honest with ourselves And said why are we teaching empirical fallacies as the foundation of what is supposed to be an empirical

discipline so we're going to have to strongly disagree on that one peter and i really would like you to look at alan blander's book one of the things i find ridiculous is how economists don't read their own literature when it criticizes what they themselves believe now alan blatter's book asking about prices is published in the late 90s it's been around for his Obvious for 20 something years it's about the same generation as mass kalel's textbook if you take a look on amazon you'll find mascara's book has hundreds of reviews hundreds you'll find liners book has

one review and i wrote that review in other words what doesn't fit the the ideology is ignored and that is a travesty of economics and it's time it's stopped and that's when rizzo niwa wrote um The new in new economics we simply have to abandon fallacies which have been the foundation of this discipline for the last 130 years can i um can i just comment on peter's um presentation as well which was very clear and and very comprehensive about steve's book i just have a difference and i fear i may have this difference also with

steve When you are when you put it down in writing as banks are not intermediaries but producers of purchasing power yeah i don't think that's right i think the producers of purchasing power are the borrowers um and banks i think by putting banks at the center of this we're making the banks too powerful the fact is when when the uh when the population loses confidence and Withdraws contracts borrowing um you know that makes a huge difference to and when when the population is euphoric confident believes that everything's hunky-dory and going to go well then they

increase borrowing and when they're encouraged to do so by the authorities and in particular by um the management of interest rates That they over borrow and we see that euphoria operating at the moment but it doesn't originate with the banks it originates with those active in the economy deciding to borrow more doctor and i think it may sound like a fine distinction but for me it's an incredibly important distinction because we're looking at what the behavior of borrowers and we're not over stating the power of bankers or shadow Bankers for that matter i mean one

of the things uh steve that's missing from your book is is a discussion about the shadow banking sector which is now operating out there in the stratosphere and that is is invisible to regulators essentially and that is likely to be spewing out enormous quantities of credit um against asset values that are can't be expected to maintain their value um but Anyway i just wanted to add that that might remind you two points i should have covered with peter as well by the way but the model does include real values just you normally embed those on

the canvas and have them with system dynamics rather than in the table itself but one extension we've recently made dominsky is the capacity to handle non-financial assets so financial assets fundamentally we claim you have on Somebody else or somebody else has on you and they therefore necessarily net to zero but non-financial assets are things like a house which you own and it's not it's your asset but nobody is a liability so we've added the capacity for that in the most recent version of minsky and that then means we have a possibility of linking together the

role of the financial system in generating the valuation of non-financial assets which is an essential extension of the Logic which uh was i've done in other forms but i haven't done inside minsky before and on the jubilee sorry yes peter yeah first of all hicks and islam i think the main problem is hicks derived islm from the classical loadable funds model that's what he did but that was broad it was definitively flawed because he can never derive islm from the loanable funds model because the loanable funds model has Only one asset one general purpose sln

has money has bonds has central bank reserves and everything so higgs made a huge mistake deriving islam from is but nevertheless the model that he falsely derived is a very useful model and i can use it to explain many many things that are going on i cannot imagine with your model how you can say anything about what's happening in profit And what the central banks did and what they thought about fiscal policy can you explain anything about this if you are with your model it's quite straightforward in fact i can actually one thing i was

going to cover is the fact that i can show a jubilee is non-inflationary uh by buyer what with your model what can you say about corbett about the shocks of government how central banks reacted and official policy that's why i need a Model for to explain my students enormous amount because it did that and that that i do in extensive models because what you're looking at what you've looked at with minsky so far it's just a model of a single the banking sector view alone but the whole thing has been designed for interlocking uh what

we call godly table so this is the banking sector but i'm showing the central bank the government the treasury fundamentally and the Public which we can now show separately on on separate screens to show that how all the all the accounts interrelate and i can show the impact of central bank purchasing of of government bonds for example as part of the model very easily it took me about it less than a day to build the model you're looking at here and what i show is the impact of a jubilee and and different ways the jubilee

can be managed as both a non-inflationary And i think this is far richer than islam and peter it sounds to me like you haven't read hicks's uh paper iceland explanation i can even show you how he wrongly derived it but nevertheless please please please let's let's yeah i know what tricks wrote but he made the mistake of of deriving some slm from from the london defense model which is absolutely impossible but nevertheless The model he created this way is very useful but please show me how you can see anything meaningful about what's going on in

the pandemic with your approach there are the students sitting in your classroom you know it's just straight i think you can tell yeah i could i can define model if you what we have happening in the pandemic is an enormous fiscal stimulus where the government is creating money And put it in people's deposit accounts and that is causing increase in the reserves at the same time and that is that is where what's called the huge increase in savings has come from it turns up in the model it's extremely simple to all the straight minsky far

simpler than removing a couple of islam diagram elements i'm i'm obviously more familiar with my software than you are and i'm telling you it's easy for me to model what's Happened with the pandemic in minsky and it makes far more sense than doing it in an islam which would show a crowding out effect which we haven't seen but we've had a supply chain disruptions you can do many things but but still i don't see with all the whole approach to make a simple explanation to the students the classroom what's happened there was a demand shock

and then we had fiscal Policy reacting then monetary policy directly now this i can nicely explain with islam and and how can can you explain it i think it obscures with rslm and that's why i've done my whole work is so we have to get rid of it and i you know i mean and with hicks's statement there i mean you you're saying hicks didn't know what he's talking about i believe he did and the final line he says in the uh in the obvious the final paragraph when one turns to questions of Policy looking

towards the future instead of the past the use of equilibrium methods is still more suspects if one cannot prescribe policy without considering the possibility of the policy may be changed which is anticipating lucas's critique he then says i accordingly uh can go back to this actually earlier in the paper he says this that it's only useful where equilibrium is uh not a total Distortion and he said it should just be no more than a classroom gadget to be superseded later on by something better i think we should take his advice from 30 years ago and

get rid of it and put something which is dynamic in there rather than aesthetic equilibrium thinking that is fundamental to rslm we're going to always disagree on that you could show me easily what's happened in the epidemic with your approach you can yes i can Expect me to do it in the middle of a discussion give me give me more than five minutes to put it together i mean maybe you should we could peter can't you accept that just to to base it on loanable funds is deeply deeply flawed and deeply anti-cained in that's what

i would present about but the islm model is not lonely that's a key point has nothing to do with loanable funds in the aslm model you have banks that can create money Without relying on deposits loanable funds is that banks need deposits before they can land that's sick and at least loadable funds is a one one commodity world yeah and and the difference is in in slm the lm curve are banks that can create money without without the deposits that's that's it the financial system they can't create they can't create Money unless there are borrowers

no of course that's but that's a completely different story and an essential part of iceland is deriving it from a constant money supply which the government can vary which is i think you can can adjust islam you can have it can have a can have a horizontal aircraft you can do anything peter you and i are going to take a totally different approach to economics and the future and that's partly why i call this the new economics Okay maybe you can continue this the schedule unfortunately the final test must be that you can explain in

a simple relatively simple way what's going on in reality i think that's what matters and of course if you make assumptions which are which are not realistic it's a problem but overall but what counts in the end can you explain some of what's going on and i must take him with your approach i don't really see how how one Can somehow explain what's going on in reality i don't i think i want to have something which engine understand a student's engineer it's engineering students come out at the end of first year and understand dynamic systems

non-equilibrium behavior and and and and the actual dynamics of the real world and economic students come up with a mythical view of the system of moving lines on a flat by blackboard and i think that's why we've got simpletons in Economics rather than geniuses so i'm sorry i disagree with you fundamentally i think we have to break away from that and that's what i read in this book yeah thank you i think you're pointless we don't we won't solve the this uh issue now but it's i think it's very important to to continue to discuss

that but i would like to ask steve i mean you're very skeptical and reading your book it's it's a very straightforward point against um Mainstream and neoclassical and anything and when you quote north house for example it seems so evident i mean it's so crazy um what would you say isn't there something moving in in the domain in economics i mean i mean if you confront today's economist with these things they wouldn't agree probably Very many of them won't agree anymore uh so what can you tell us what is your view on this is there

something going on is there something even if not everyone agrees to your models but um well economics i think is a dead end and it's going to stay at a dead end while we continue building on foundations like microeconomics and frankly rslm um this is why i said we need to parrot a revolution which which economics has managed to Prevent because we come back and fall back into these old micro grounds whenever the macro lets us down show me an isola model that predicted the financial crisis i'd be fascinated to see that showing a dsg

model that did that that'd be all equally fascinating none of them did and when people like anne and myself are coming with all alternative analysis and saying we saw the crisis coming your models didn't do it why the hell are you still defending Them and this is the problem you can always get stuck in a rush if you want to get out of the rut you've got to be kicked out of it frankly and that's what i'm trying to do by bringing engineering ideas into economics i think what's happening to what thomas has said i

think it is true that economics is moving that economic students are asking questions and that there are new generations Rising who are looking at this in a different way and it is true for example here in britain our prime minister theresa may assured us that there was no such thing as a magic money tree and then the next uh chancellor uh shunak uh announced for the pandemic that there was a magic money tree that it was possible uh to finance if you like the almost nationalization of the economy um and you know these are these

are dramatic these have been dramatic Changes um throughout the pandemic that must be changing minds now of course the ideology keeps coming back uh right now our government is saying no we've got to pay for this and we need austerity and so we're about to be plunged back into recession here but for a whole year it wasn't possible to argue that there isn't a magic money tree you know it was clear that the central bank was supporting the government in providing the finance which was going to uh to to Maintain businesses and keep people keep

the economy on a life support system at the very moment moment when it collapsed through no fault of its own so so you know i think that must be thomas a changing minds but the ideology is still very deep and we don't coming through in form of policy of forecasting the financial crisis you said isom did not forecast the financial Crisis this is true but steve i looked at the two quotes that you made where you said you did forecast the crisis one is in paper from 2006 where you forecast the financial crisis for australia

but the financial australia didn't have a financial crisis and the second paper that you mentioned is from september 2007 and the other financial crisis was already there so i would be a little bit careful in making it yes i'm sure peter and i've had this many miniature moments And it was the hell out of me so i'm going to talk over the top of you and tell you when i started talking about that it began on december 18 2006 i have a conversation has happened with my wife at the time when i was asked to

do an expert witness case over predatory lending in australia and as part of that i made a throwaway line as an expert witness based on mercy's financial instability hypothesis saying levels of private that have been rising Exponentially compared to income now i knew as an expert witness in the australian legal system i couldn't make a hyperbolic statement so i thought i had to go and check the data and i'd find that i had to remove the word exponential because it surely wouldn't have been that and it i managed i did a whole lot of routines

in my private program mathcad at the time to do it took me a few hours to get there can i finish please can i finish you've asked Me a question here a challenge to my integrity i'm going to reply to you on that basis and i did it and i found that when i i've got the shock of my life when i plotted the debt to gdp ratio for australia and it was clearly exponential in fact the correlation between it the pure exponential function and the ratio of private debt to gdp from 64 to 2007

or 2005 pardon me was 0.9912 it doesn't get much closer i didn't Remove the word but i thought i've got to check the american data so i managed to get the data from the american federal reserve download that compared to gdp and i got a correlation coefficient for them for 0.97 from tonight 1952 until 2007. so my wife woke up in the morning and said there's going to be a financial crisis global and i then tried to marry the realm about it there wasn't time to go through journals so i did it through the newspapers

and I'm only stuck with australia now the reason australia didn't have a financial crisis is because it stopped the credit collapsing and the reason is stop credit collapsing is because i scared the out of the government at the time the government of kevin rudd and there were two consecutive days of the national broadcaster in australia where they interviewed miller one day and kevin rudd the next now normally in that show you get if you're not the prime minister You get what you get four or five minutes if you're lucky i got 15. the next day

the prime minister's being interrogated about my views and the day after the week after that they came up with a stimulus program doubling and trebling the growth the grant for first time buyers to keep the first home but the house housing bubble going so if you look at the credit which is what ann and i both know causes financial crisis when it goes negative in australia's case it Didn't go negative and it was because of stimulus that i scared them into doing and i criticized at the time okay that's why australia didn't have a financial

crisis and then china came to the rescue of australia china yeah okay china yeah anyhow but anyhow you give two quotes the one quote is on australia where there was no financial crisis and the second quote is from september 2007 when the crisis had already been there it's not right i wrote that in september Do you know nothing about publication lags i wrote that in july it took until the end of september to be published now please stop giving me rubbish here i get enough of that from journalists and politicians in australia i will not

accept it from somebody who calls themselves an academic if you want to look at my like quotes going back you can find i talked about australia because that was my country okay i'm nationalist enough to Worry about my own country and talk about that but i made comments about america as well and you can find debt watch reports going back to 2006 where i talk about the american situation as well now pardon me but you're being far more of a politician than i'm willing to be by making the sort of claims you're making there i'm

not going to tolerate them but they're at the beginning oh by the way mark i'm going to say mark kirsten the question he's made a very Good question about what's called ergodicity economics it's extremely important it's an alternative to the rational expectations efficient markers hypothesis nonsense that dominates finance and economics and i recommend to anybody who doesn't know about ergodic economics and take a look at the work being done by a mark and by peter by la peters about an alternative approach to finance which is far more realistic than the nonsense Neoclassicals regurgitate in the

efficient markets hypothesis okay um i would um i mean at some point i was afraid that this will be too much of a harmony discussion uh i'm convinced now that this was a wrong assumption um but still i would come back to to the point what is moving and and how what is your view of a paradigm shift in a Paradigm a new paradigm i mean is that the big revolution that will come at some point or is there something about you know moving from time to time if you look at former paradigm shifts inside

the the one you you may consider as as one but after the second world war and the new new liberal paradigm shift this has never come by one revolution at one day but a lot of movements going going Around so are there things that we would consider as positive and where you can well yes for example the work of the ole peters and already calls over the city economics i see that as a very significant paradigm shift that completely inverse the whole efficient markets hypothesis and the idea effectively you can you the idea that what

you do is given by expected expected uh value and expected utility that's that's a true paradigm shift from The finance side complex systems this is another one coming into economics and what i've what i do with my work on minsk is fundamentally showing that complex systems gives you a totally different outcome to economics and your foundation is macroeconomics not micro in fact i think micro should be as it's taught should be thrown away it's a waste of time uh although the so-called lessons are lessons about a world that doesn't exist as veterans Said many many

decades ago we have a taxonomy of perfect competition imperfect competition monopoly and oligopoly where you cannot find a single instance of that in the real world okay we have a we have a taxonomical economics which is not relevant to the actual real world we need an evolutionary one and back again sean payton was very good on that we need an evolutionary theory of competition not the static the Taxonomic one which we're going to criticize so effectively but in other words there is there is there is no revolution within neoclassical economics there are changes of paradigm

there are shifts in what the cultures used to call the protective belt assumptions around the hardcore but the hardcore of utility maximizing behavior subjective valuation everything in the real rather than the the nominal nominal the monetary world that is Untouchable and unchanged and so long as it stays there we will never have a decent economics uh and perhaps one comment from from your view on all this i mean the old let's say the yo parry and the market liberal one one of the strengths of this paradigm has been that it was the narrative was extremely

simple and many many ideas were extremely simple Now proposing to have a new paradigm which has one element one one big element complexity economics or complexity models or however you call it theory um i mean it doesn't seem so attractive as it seems maybe for us as we see the the point do you have any idea how to better bring this to a broader public to these Ideas well um you know i i i think steve's absolutely right that we're dealing with a complex system you know just like the energy system we're dealing with a

complex system and so to make it too simple for the public is is is not easy but it's for me the paradigm shift is is really to Reclaim some of the existing truths this is a bit like we know we have in in physics a theory of gravity we don't need a new theory of gravity because gravity is gravity you know the monetary system is a system that's evolved over time and it is as it is what we need for it to be is to be understood and to be accepted in the way that physicists

accept gravity in the way that aeronautical engineers understand gravity and then within that Understanding are able to invent and expand uh their their designs and their ideas but they don't say sorry but gravity doesn't exist do you know what i mean so i think part of what we have to do is to build on the truths that exist and that we've learned you know from back 1705 a great many of those truths were in my view uh contained within the work of john maynard keynes who by the way is always described as being about fiscal

Policy and is always uh having attributed to him the fact that only fiscal policy can address a crisis he was overwhelmingly concerned with monetary policy his his general theory was called the general theory of employment money interest and money it wasn't called the general theory of tax and spend um so uh so now i think in a sense we've got to build on those foundations that we know to be true and that are true for all economics and then Accept that actually we've built institutions that have gone well beyond the capacity of the economy to

cope with those institutions and i'm thinking of the shadow banking system which is chaotic and anarchic and and doesn't if you like obey the laws the the economic economically equivalent laws of gravity and and therefore endangering the whole of the of society and of the environment Because of course it's encouraging uh more and more extraction of the of the earth's finite assets so i think it's about building on existing truths and and then accommodating the changes in the institutions and the behavior that we've encouraged through these uh liberal ideas market theory ideas okay perhaps just

a question on money matters is that Something that goes i mean that more and more economists would accept as an idea in germany i think what one can see is that in in the prestigious us universities in harvard and princeton and so on uh what modern uh macro economics are still macroeconomics without money so they are still totally based on the loadable funds approach there are still no banks that Can create money independently and i think here the real revolution is definitely if you need it so i think that's that's absolutely so also the financial

crisis has shown that this loanable funds paradigm is completely obsolete it still is a dominant model in in all all uh top mainstream uh papers and and and approaches i think here we definitely need a revolution okay we have a couple of minutes left there are some questions and we promised Um to the audience to uh nobody in the questions and let the panelists know about them answer them and we'll send back for those who we can't discuss there are some very fundamental questions um like uh are you in favor i think it's uh steven

of a constant model supply system given that credit creates problems okay well just actually one of the questions there from uh ivan about so Explaining our government's ads are the uh money supply uh if you go to my um prophecy of keen website slash minsky you'll find i have some models there that illustrate that also recent recent models on my on my uh patreon page where i illustrated quite straightforwardly because once what you can show with the the double entry bookkeeping approach that i take with those tables of course you have assets on one side

and Liabilities on the other money is fundamentally the liabilities of the banking to the banking sector okay so if you want to increase the money supply create money or destroy it you must make a change on the liability side but not two changes there must be a change there from the liability side and also a change on the assets now when you look at the banking sector the banking sector creates money by increasing deposits and by increasing loans And the deposit the loans across the link so the person who borrows the money gets the deposit

as well most of the time so there's that's that's the money creation by private banks with the government the government puts money in private bank accounts and puts it in the reserves at the same time so the reserves go up and the the the deposits go up at the same time that's how government deficits create money and then what you get as a result Of that if you feed through the tables and i show that on the models you'll find inside the modeling with minsky book that i've mentioned at the end of my presentation there

which you can find on profsteveking.com minsky download that book and you'll find quite a few models discussed there so if the government runs a deficit what it's doing is transferring money from the treasury Account it did central bank to the uh reserve accounts of the private banks and that transfer effectively puts the treasury into negative equity when you look in terms of financial claims and if you look at the aggregate data that is the common place almost all treasuries around the world are negative equity in terms of purely financial assets and that's a necessity For

the creation of money so uh i do mention that extensively in that book modeling in minsky much more so than i do uh in the short one of zan said it's 25 000 words it's very very short uh but modeling for modeling minsk is about 60 000 words and lots of mathematics and lots of models inside there and you will find the answer to your question then you'll find models that illustrate it as well okay um thanks uh steve um some other Questions which were about growth and so on but i i would suggest that

you may send us comments if you want um so we can don't need to open these larger discussions now um except for one question maybe will there be a german edition german edition of the new economics you Better translate that for me yes so not yet in in the planning um but maybe so we'll see um then well i i think we had a very lively discussion very hard discussion on islm and the models i think that shows that there's a long discussion still needed and and some Discussed even between people who are maybe let's

say largely on the same side of how they view economics and and the world but that that may be part of a paradigm shift that's what we learned when we studied history of paradigm shifts that's something which takes time and a lot of elements come into place and need to be in place i don't want to be Too pessimistic but we had a seminar some time ago in paris where french historians said maybe this the financial crisis as a triggering moment for change uh was not the big one compared to the 29 banking crisis but

more uh 1914 and that leads to a very pessimistic view which is that in between in the in between the wars there was a lot of thinking about How to change but not really enough and it was only the very big crisis and then the shock of the second world war that really led first in the us and then in the rest of the world of to something which was even if you don't see the complete paradigm shift as you would like to have seen it steve but there was a new paradigm after the second

world war so we very much hope that we don't need such a catastrophe to To get to a very new paradigm shift but it shows that there's a urgent very urgency and if you look at what's happening policy and with widens program and the time scale until the middle elections you see that there's real urgency so many things for any contribution i think that leads to some this change uh whatever the outcome will be thanks steve Thanks and thanks peter for this very lively and very good discussion and see you soon