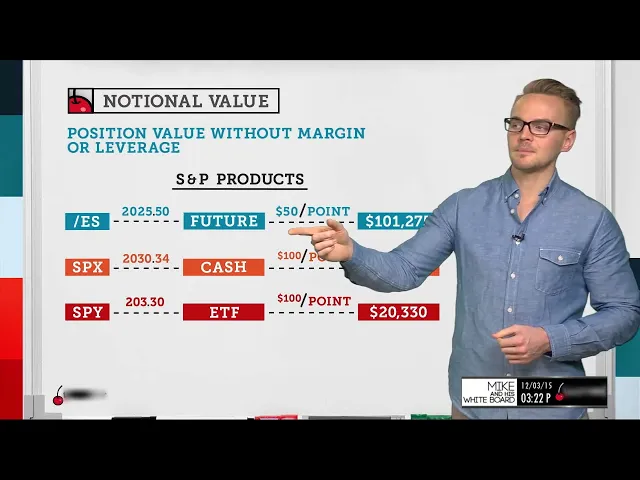

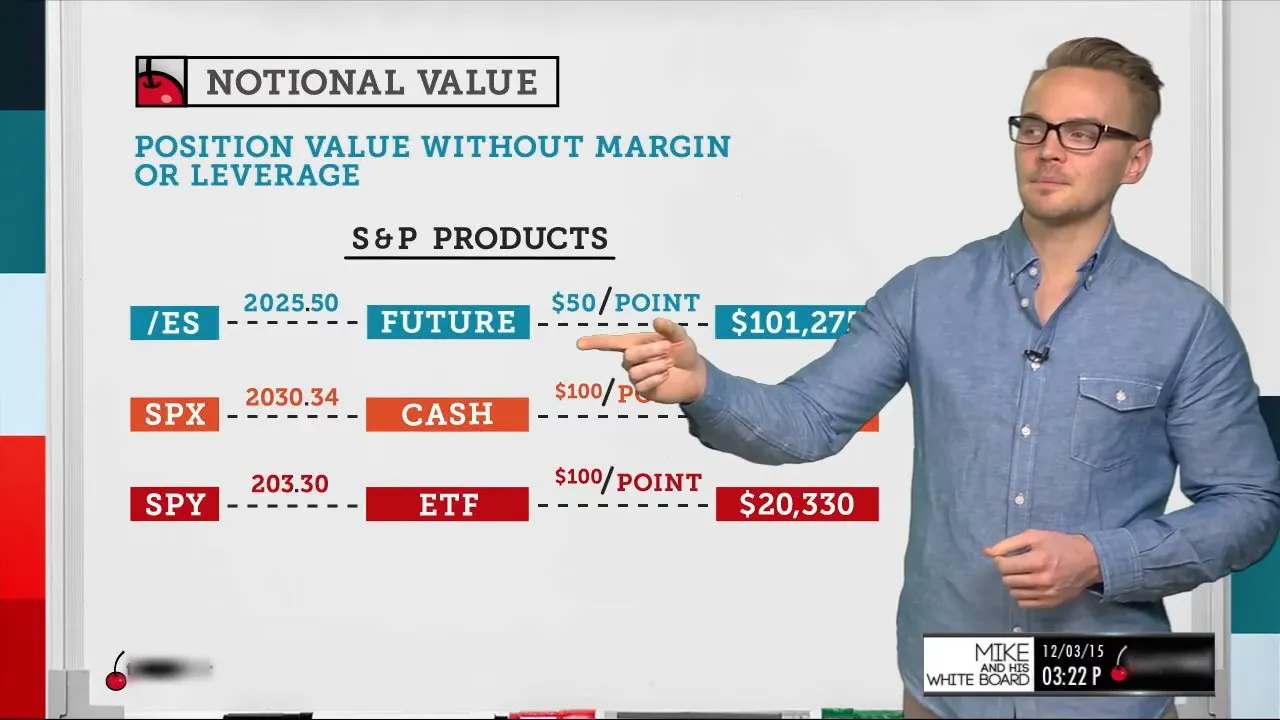

[Music] [Music] hey everyone welcome back to mike and his whiteboard my name is mike this is my whiteboard and today we're going to go over a topic that is pretty much overlooked in a lot of spaces and it's going to be notional value and one thing about notional value is that it's really important to understand especially when we're trading naked options and specifically selling naked options so let's get right into it and we'll break down notional value which is essentially the value of a position or the position value when you take out margin and you take out leverage so we're just basically looking at the raw value of the position which you can also consider to be your max loss of the position so we've got an example here and let's say we're selling an out of the money put contract so we've got the put that's below the stock price because again a put contract is the right to sell 100 shares of stock so if i'm selling the right for someone else to sell the shares to me it's going to be out of the money if it's below the stock price because if they can sell their shares at 50 there's not going to be any value with our out of the money put here but with all that said there's still going to be value extrinsic value in that put which we can take advantage of by selling out of the money options so let's say we've got this 48 put that's out of the money and let's say to sell this put it requires 800 of margin so if i'm in a margin account one of the benefits of a margin account is that it gives us additional leverage when we're selling options or even buying stock for that matter so when we're talking about puts we actually had a previous whiteboard if you missed it on buying power reduction so if you missed that one you can check it out by just clicking on find shows at the top and then scrolling down to mike and his whiteboard and it'll be there and when we're talking about margin it's basically giving us additional leverage so instead of having our notional value of 4 800 less the credit received a margin account is going to allow us to sell this put for let's say around 800 now these numbers aren't real it's just a an example here but the issue is that the margin is not going to be reflective of the notional value or my max loss so the margin is our theoretical max loss based on a certain standard deviation move but when we're looking at our actual notional value for this position when i'm selling a put at 48 and if i received a credit for it i would basically have to buy the shares at 48. so let's say the stock price goes from 50 to zero i would see a max loss of 4800 as you can see from notional value but since i sold the put and receive a credit for that i can use that to offset my max loss so what's important here is that margin is not equivalent to notional value when we're looking at naked options and the notional value is going to be reflective of our max loss and we're going to break down another example in the next slide here which is going to make this very apparent so on the next slide we're going to break down the a few s p products so a lot of the s p products that we trade are going to be the e-mini s p 500 futures contract which is slash es we're also going to look at spx which is a cache index that basically replicates the movement of that and then we also have spy which is our etf and it has the smallest notional value of the three examples here so what we're going to talk about is different notional values and different values for each point so with the e-mini s ps these numbers were taken a couple weeks ago so this was back when the es was at 20 25 50. so this is a future contract and the value of each point is 50 so if i own the futures contract it's actually tracked in quarters of a point so it's going to be 12.

50 per tick but it's 50 a point so let's say i own this futures contract at 20 25. 50 if it goes to 20 26. 50 i'm actually going to make 50.

so to calculate my notional value all i need to do is take the current value in points and multiply it by how much how many dollars that is per point so we've got 20 25 50 multiplied by 50 which gives us 101 275 dollars so that would be my notional value that i would be considering for that trade however in a margin account if i actually buy this future outright i'm not going to have to put up 101 000 i'm going to put up way less than that because trading futures gives us that leverage in that margin to be able to do that so we might see a different value in terms of buying power reduction that's used to place the trade but our notional value here is this value here so if we go to another example we've got spx which is our cache index and you'll see that our cache index is going to trade a little bit different than slash es so usually it's a little bit higher as you can see here so when i took this number it was 20 30 34 and with spx it's actually 100 a point so with that said when i take the point value 20 30 34 multiply it by 100 a point i actually get 203 000 34 cents so that would be the notional value of that position now what's interesting is that spy which is our etf is actually 10 times less than notional value of spx so this gives us a great understanding of three different products and different ways we can trade them so if i'm in a smaller account i might lean towards spy and as my account gets larger i might start trading futures or look to spx but just for the example's sake we've got spy at 203 330 and this is also 100 a point so when i multiply those together my notional value is 20 330 dollars now what's interesting about this is spy and spx are 100 a point however one point in spy is actually going to be reflective of 10 points in spx so it's important to understand that so if this were to increase 10 points to 2040 you would see spy only increase from 203 to 204 so definitely under definitely a good point to understand and hopefully this gives us a better breakdown and better understanding of true notional value and what we're actually trading regardless of leverage or margin but let's wrap it all together with some takeaways here so first takeaway is that it's important to be aware of the true value of products we're trading so like we just showed here there's different s p products that look to track the same movement but when we actually break it down to the notional value as you see in the second takeaway they're very different so it's very important to know exactly what we're trading and align that up with our account size our risk tolerance etc so if i'm not comfortable with trading naked options i might be able to define my risk and defining my risk in positions such as those underlyings is going to give me a more defined max loss and max profit as well so just understanding these is going to make us better traders in the end and one last thing is that notional value differences are especially apparent in futures contracts so for example we just talked about es how that's 50 a point well if we look at something like cl which is the crude oil futures it's actually a thousand dollars a point so understanding those differences and then how they're completely different products is going to make us better traders and allow us to understand different strategies in different ways so this has been our overview of notional value hopefully you enjoyed it thanks so much for tuning in if you've got any feedback or questions shoot me a tweet or you can send an email to support or support and we're actually done for the week but we'll be back on tuesday at 3 15.