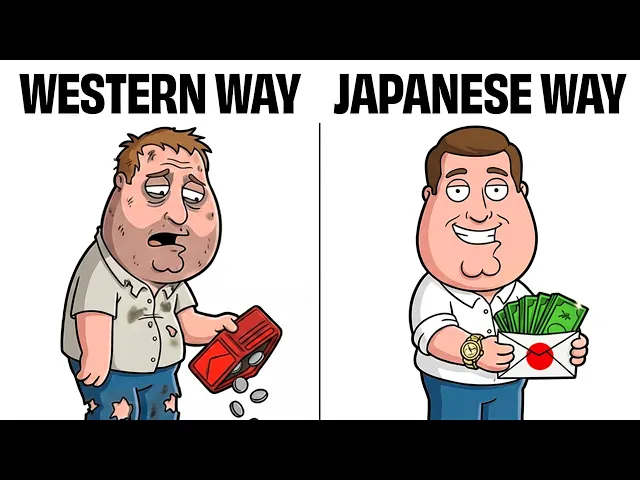

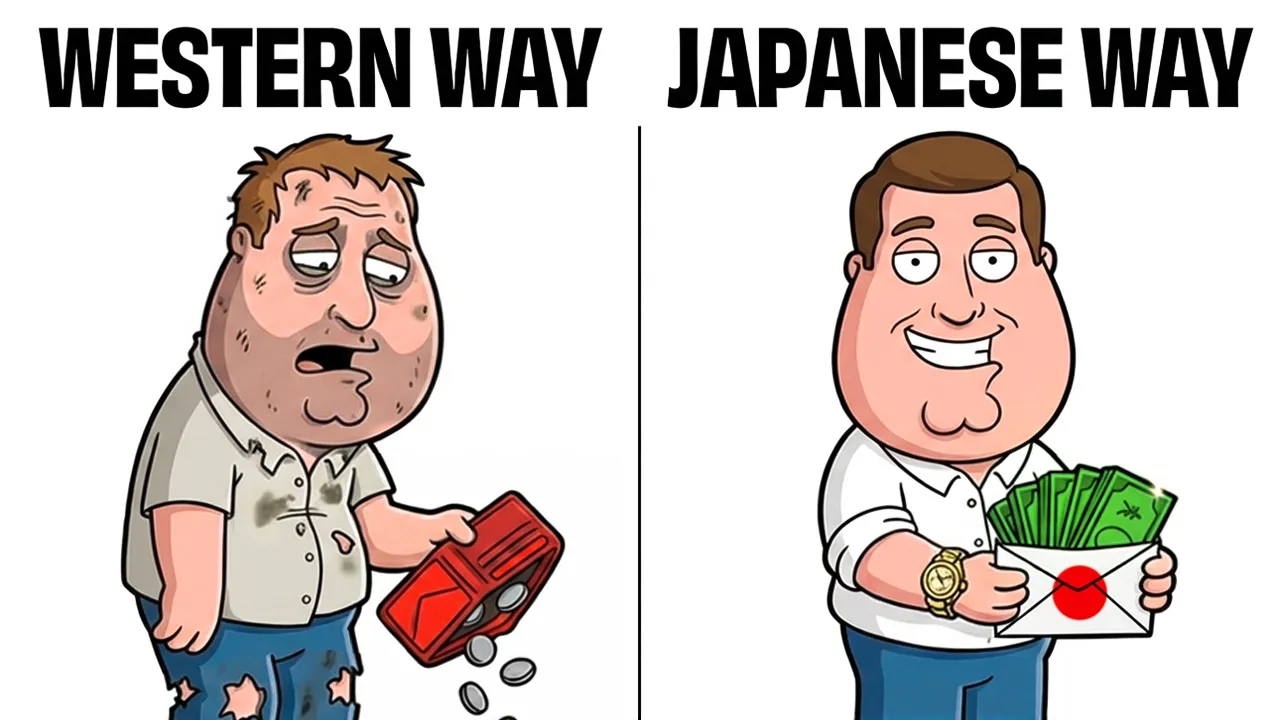

You save 4% of what you earn. Japanese working households save 37%. Same planet, completely different relationship with money.

And it starts with a notebook a woman invented in 1904 that has no app, no algorithm, and somehow outperforms every budgeting tool Silicon Valley has ever built. My name is Nick, and if you've ever wondered why your budget works perfectly in theory and nowhere else, stay with me because the answer isn't discipline. and it's a completely different operating system.

Before we get into the solution, let's sit with the problem for a second because the numbers here are genuinely embarrassing. And I mean that for all of us collectively, not as a personal attack. The average American personal savings rate right now is around 3.

9%. Meaning for every $100 that comes in, Americans save roughly four of them and spend the other 96. But here is the stat that should actually make you put your phone down.

It's not just about how much we save, it's about where we keep it. In the US, we live in a culture of leverage. As a result, the average American household keeps only about 13% of their financial assets in actual cash or savings deposits.

The rest is tied up in the stock market, locked in retirement accounts we can't touch, or simply doesn't exist because we're living on credit. In Japan, that cash number is 54. 2%.

2%. More than half of the average Japanese household's financial wealth is liquid, safe, and sitting in the bank. That is a fortress of stability.

And Japanese people aren't making dramatically more money than Americans. Their median household income is actually lower. Like, they're not living in bigger homes.

The average Tokyo apartment is around 600 square ft. They're not depriving themselves. Japan has 2.

6 6 million vending machines, one for every 23 people, the highest density on Earth. They have 55,000 convenience stores. And they spend billions of dollars on mystery shopping bags every new year.

They don't have this stability because they spend less on everything. They have it because of how they think about everything they spend. And that distinction between spending less and thinking differently is the entire video.

Meet someone we'll call Ryan. Ryan makes $68,000 a year, which is close to the American median. He's got rocket money on his phone.

He checks it occasionally, feels mildly terrible about the dining out category, and then closes the app and orders delivery anyway. He's not irresponsible. He pays his bills.

He's got a small emergency fund. He contributes a little to his 401k, but at the end of every month, there's this gap between what he planned to save and what he actually saved, and he can never quite explain where it went. He's doing everything he was told to do.

It's just not working. Ryan's problem isn't discipline. Ryan's problem is that every financial tool he's ever used was designed to record his behavior, not change it.

And there's a profound difference between those two things. Rocket Money has tracked Ryan's spending for three years. It has not once made him spend less.

It's just produced an increasingly detailed archive of his financial regrets, organized by category and displayed in a color that implies judgment. The Japanese figured out something about human psychology that Silicon Valley hasn't caught up with yet. And it starts not with a tool, but with a feeling.

Here's something that has no direct English translation. Motai. The word is about 800 years old.

Its roots are Buddhist from Japan's Kamakura period, roughly the 1200s. The literal meaning is something like the absence of substance, the loss of what makes something meaningful and whole. The concept comes from a Buddhist teaching that everything exists in relationship.

A grain of rice isn't just a grain of rice. It exists because of the farmer who planted it, the soil that fed it, the water that fell on it, the hands that harvested it, the person who cooked it. To waste that grain of rice isn't just to discard food.

It's to dismiss every connection that created it. That's matanai. Not just waste, the felt weight of waste.

The genuine discomfort of allowing something's full value to go unrealized. Now before you write this off as ancient philosophy with no modern relevance, consider this. In 2005, Wangari Mathi, the Kenyan environmentalist.

I am the first African woman to win the Nobel Peace Prize, visited Japan, encountered this concept, and walked into the United Nations holding a t-shirt with matana printed on it. She stood in front of the General Assembly and argued it was the missing fourth R. Reduce, reuse, recycle, and respect.

a single Japanese word powerful enough to travel across a language barrier and land at the UN. Now apply it to money. And here's where Americans should feel genuinely seen because we are the anti-minei nation.

The average American throws away 80 pounds of clothing per year. The average American home contains around 300,000 items. We have a $ 38 billion self-s storage industry.

Not because we don't have enough space in our homes, but because we have so much stuff that our homes can't hold all of it. So, we pay extra money every month to store the overflow of things we've already paid for and no longer use. That is motani made physical.

A countrywide monument to unrealized value. Manai applied to money means that buying something you'll use three times and forget about is motane. Upgrading your phone when the current one works perfectly is moteni.

Subscribing to something you stopped using six months ago but haven't cancelled yet. Also moti and also somehow a category most people have in their budget. The concept doesn't tell you to spend nothing.

It tells you to feel the full weight of what you spend it on. Americans have largely outsourced that feeling to a return policy. There's a Japanese art form that makesai visible.

It's called kinugi, the practice of repairing broken pottery with gold lacquer. So, the cracks become the most beautiful part of the object. A bowl breaks and instead of replacing it, you repair it and the repair transforms it into something more interesting than it was before.

The damage becomes the story. Think about how many things you've replaced in the last year because they felt old or because a new version came out or because it was slightly easier to buy new than to deal with fixing what you had. Now, imagine a culture where the patched version is considered more beautiful than the pristine one.

You'd spend a lot less money. Ryan's apartment is full of things he bought enthusiastically and uses occasionally. His closet has clothes he forgot he owned.

He has three sets of headphones. one of which works fine. He's paying $14.

99 a month for a streaming service he hasn't opened since last April. None of this makes Ryan a bad person. It makes him a completely normal American.

And normal in this context is the problem. There's a Confucian principle documented in Japan as far back as 1713 in a philosophical text called Yojokun, Life Lessons from a Samurai. It's practiced in Okinawa, one of the world's five blue zones, regions with dramatically high concentrations of people who live past 100.

The principle is called harah hachi buu. It means eat until you're 80% full. Stop before the plate is empty.

Stop before you feel satisfied. Leave room. Okinowans who practice this experience roughly 1f the rate of cardiovascular disease compared to Americans.

their obesity rate is a fraction of the American average. Researchers have linked this single habit, the deliberate decision to stop before full, to a cascade of health outcomes that extends life by years, sometimes decades. Now, here's the translation to money, and it's almost too clean to be real.

Spend to 80% of your income. Save the other 20% first. Not what's left over after spending.

The 20% leaves before you touch the rest. You build your entire financial life on the 80% that remains. That reversal of sequence, saving first, spending what's left, is the single mechanical difference between the person who always seems to have money and the person who can never figure out where it went.

Ryan's sequence is earn, spend, save whatever's left, which is usually not much. The Japanese sequence is earn, save, spend what remains. Same income, completely different outcome over 5 years.

The reason Herahhachi Buu works as a health strategy is the same reason it works as a financial one. Your perception of enough is not fixed. It adjusts to whatever you've been given.

If you consistently eat until 80% full, your stomach adjusts and 80% starts to feel like 100%. If you consistently live on 80% of your income, your lifestyle adjusts and 80% starts to feel like everything. The discomfort is temporary.

The habit is permanent. Ryan, if he moved his 20% into a separate account the day his paycheck hit before he could see it, before it could be spent, would save $13,600 this year. He has never once saved $13,600 in a year, not because he couldn't afford to, because his sequence was wrong.

Now, we get to the tool. And the reason the tool works is because of everything we just covered. The philosophy comes first.

And the notebook is just the philosophy made practical. In 1904, a woman named Hani Moco published a household accounting system in her Japanese women's magazine. Hani was Japan's first female newspaper reporter, which in 1904 was approximately as welcome as you'd imagine.

She designed the system specifically for housewives who were entirely excluded from formal finance. women who managed household money but had no framework for understanding where it went or how to take control of it. She called it Cakebo.

By 1965, half of all Japanese households kept one. Here is the complete system. At the beginning of each month, you open a notebook, a physical notebook with a pen.

Yes, an actual pen. The thing you own 14 of and can never find. And you answer four questions.

How much money do I have? of this month. How much do I want to save?

How much am I spending? And how can I improve? Every single purchase gets written by hand into one of four categories: needs, rent, utilities, groceries, wants, dining out, clothes, hobbies, culture, books, concerts, courses, experiences that grow you, and unexpected repairs, medical bills, the birthday you forgot about until the morning of.

At the end of each month, you reflect. What went well? What didn't?

What will I change? That's the whole system. No subscription, no app, no algorithm, a notebook, and four questions.

Now, I know what you're thinking. That sounds like every other budget I've tried and abandoned. But here's the thing that makes Cakebo neurologically different from every digital tool you've ever used.

And this part is backed by actual brain science, not lifestyle content. In 2024, a researchers at the Norwegian University of Science and Technology ran a study using 256 sensor EEG caps, basically extremely detailed brain scanners, comparing what happens when people write by hand versus type on a keyboard. The results were not subtle.

Handwriting activated far more elaborate connectivity patterns across the brain, particularly in regions associated with memory formation, learning, and encoding. Typing produced almost no activity in those regions. The brain treats handwriting as a meaningful act.

It treats typing as transcription. Earlier work out of Princeton and UCLA found that laptop notetakers essentially record passively. Their brains are in stenography mode.

People who write by hand are forced to process, synthesize, and engage with what they're writing because they can't write fast enough to copy everything verbatim. They have to think. Applied to cobo.

When you physically write, "Spent $43 on takeout Tuesday night, stressed, didn't want to cook," you have processed that purchase in a way that looking at a bar chart in an app simply does not achieve. The app shows you what you did. Writing it down makes you feel what you did.

And feelings, not data, are what change human behavior. The unexpected category, by the way, is doing an enormous amount of heavy lifting for most people the first time they use this system. Because when you have to write down every car repair, every medical co-ay, every I'll just put it on the card moment.

Again, you see it all in one place in your own handwriting. It it stops feeling unexpected. It starts feeling like a pattern and patterns can be planned for.

Ryan tries KBO for one month. The first thing he notices is how uncomfortable it is to write things down. Not because writing is hard, but because awareness is hard.

He's been protected from that awareness by the automation of his app. The app categorizes his delivery order as dining and moves on. Writing it down means he has to decide, is this a need, a want?

And then the question CBO insists on, why was it hunger or avoidance? That question sitting there in his handwriting is something rocket money has never once asked him. Here's where Cabo breaks from every Western budgeting framework and where it gets genuinely powerful.

Western budgeting is at its core a math problem. Income minus expenses equal savings. Hit the categories.

Reach the targets. It's rational. It's organized.

And for most people, it produces zero lasting behavior change because math doesn't motivate humans. We are not rational economic actors. We are emotional, impulsive, occasionally irrational primates who buy things for reasons we'd be embarrassed to admit out loud and then invent logical explanations afterward.

Cakeo knows this. The month-end reflection isn't, "Did you hit your number? " It's what worked this month, what didn't, what brought you genuine satisfaction, what do you regret, what is one thing you'll do differently next month.

It's a therapy session for your spending. And the act of writing those answers in your own words, in your own handwriting, is the mechanism that closes the loop between information and change. Most budgeting tools give you data.

Cabo gives you a mirror. And the four categories matter too in a way that's easy to underestimate. In most western budgeting apps, a $60 cookbook and a $60 dinner out are both dining or food.

In Cabo, the cookbook is culture and the dinner is a want. That distinction creates a different internal conversation. One is investment, one is consumption.

Both are valid, but knowing which one you're doing consistently over months creates an entirely different understanding of what your money actually means to you. And before any non-essential purchase, CBO has one more filter. Do I genuinely need this?

Do I genuinely want this? Or am I just bored? One of those three leads to a purchase.

The other two, if you're honest, do not. That's not deprivation. And that's the difference between spending with intention and spending with momentum.

Ryan, after 3 months of KBO, can tell you exactly where his money goes. More importantly, he can tell you why. And the why turns out to be the thing that was always missing.

There's a phrase inscribed on a 17th century stone basin at Ryoenji Temple in Kyoto, one of Japan's most famous Zen gardens. The phrase is Taru Wo Shiru. know what is enough.

It appears in ancient Chinese philosophy, in Buddhist teachings, and apparently on rocks in Japan, which suggests it's been considered important for a very long time. Taru Oshiu doesn't mean be satisfied with less than you deserve. It means develop the capacity to recognize when you actually have enough rather than perpetually chasing a finish line that someone else keeps moving.

Because here's the uncomfortable truth. The entire architecture of American consumer culture is engineered to prevent you from ever feeling like you have enough. Every advertisement is a structured argument that your current situation is deficient and their product is the solution.

Every social media feed is a curated display of what other people have that you don't. One-click purchasing exists specifically to eliminate the pause between desire and transaction because that pause is where buyer's remorse lives. and buyer remorse is bad for sales.

The system isn't failing. It's working exactly as designed. It's just designed for someone else's benefit, not yours.

Japan isn't immune to consumer culture. They invented significant portions of it, but they have philosophical counterweights that Americans simply don't. Aimoti creates friction around waste.

Harahhachi Buu creates a default stopping point. CABO creates a moment of deliberate awareness before the month ends. These aren't personal discipline hacks.

They're cultural defaults. The right choice has been made slightly easier and the wrong choice has been made slightly harder across every layer of daily life. The gap between having 13% of your life in cash and 54% of your life in cash isn't willpower.

It's defaults. Ryan can't control the algorithm. He can't redesign the one-click checkout, but he can add his own friction.

He can write things down. He can move money before he spends it. He can ask whether something is a need, a want or avoidance.

He can, in other words, build his own set of defaults borrowed from a culture that built them into the infrastructure centuries ago and updated for an apartment in whatever city he happens to live in. That is the Japanese way to save money. Not deprivation, not discipline, a different set of defaults, a different relationship with the things you own and a 120-year-old notebook that the neuroscience has now caught up with.

The honest summary is this. Japan didn't build a saving culture by being more disciplined than everyone else. They built it by making the right choice feel natural and the wrong choice feel uncomfortable.

Motinai makes waste feel wrong. Harahhachi Buu makes excess feel like a mistake. Cakebo makes spending feel real in a way that an automated app never can.

You don't need to move to Tokyo. You need a $3 notebook, a pen, any pen. You have so many pens, and the willingness to write down every purchase you make for one month.

Then sit with what you find. You need to move 20% of your next paycheck somewhere you won't spend it before you see it. And you need to get honest about whether the things you spend money on are building the life you want or just filling the space where that life should be.

The app will keep categorizing your spending for you. It will keep generating the charts. It will keep sending the notifications you dismiss.

None of that has worked. The notebook is waiting.