Jason bought his first house at 28 because that is what you're supposed to do. He had saved $42,000 for a down payment. He was tired of throwing money away on rent and his parents kept asking when he was going to stop renting and build some equity.

The house cost $420,000 in a suburb of Denver. He put down his 42,000 10% and financed the rest at 6. 8%.

His mortgage payment came out to $2,470 a month. Add in property taxes at $420, homeowners insurance at $180, and the HOA at $215, and his total monthly housing cost was $3,285. His rent before buying had been $1,900 for a nice two-bedroom apartment 8 minutes closer to his office.

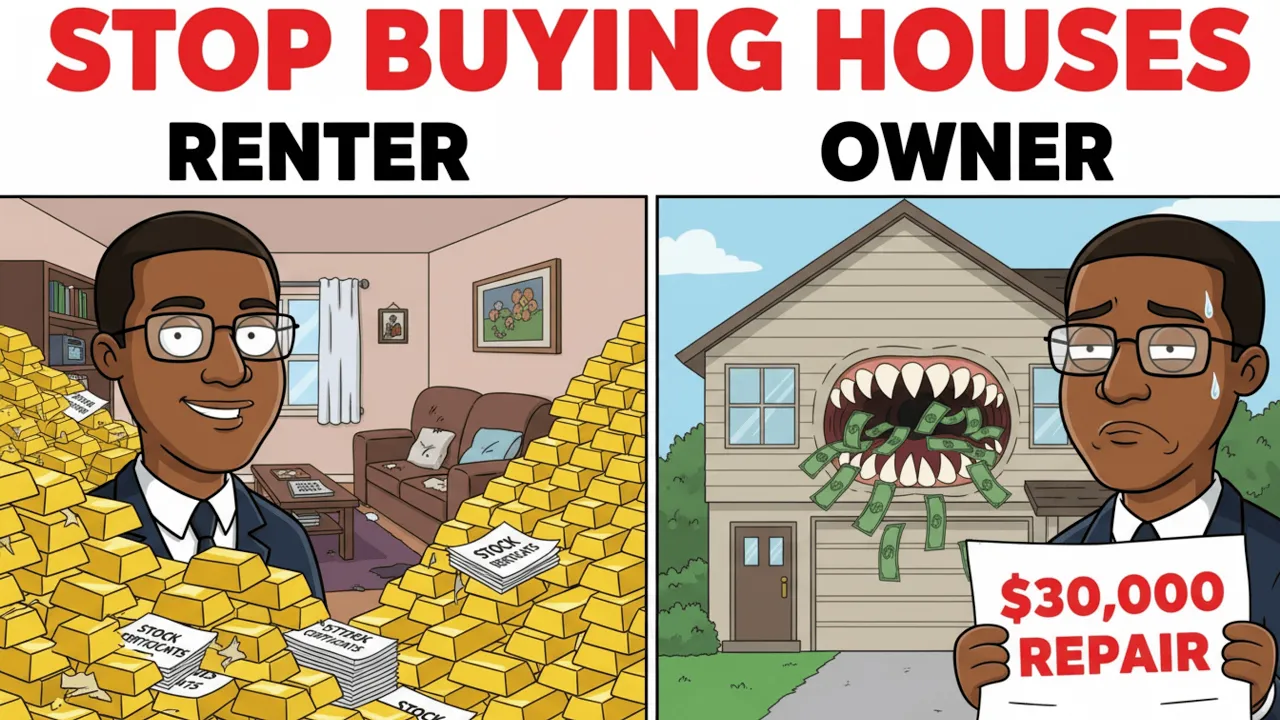

Jason did not run the numbers. He just knew the way everyone knows that buying is better than renting because rent is throwing money away and a mortgage is building equity. Four years later, Jason has spent approximately $157,000 on housing costs.

His home is now worth about $445,000, a modest depreciation in a market that has cooled significantly since he bought. His remaining mortgage balance is 352,000. His equity on paper is $93,000.

But here's what Jason does not realize. If he had kept renting at $1,900 a month and invested the difference, the $1,385 per month he would have saved into an index fund returning 8%. He would have approximately $81,000 in investments.

Add back his original 42,000 down payment, which would have grown to about 57,000 in the same index fund, and his total liquid net worth would be around $138,000. Jason's home equity is 93,000. His alternative liquid wealth would have been 138,000.

He is $45,000 poorer than if he had kept renting. And he cannot access his equity without selling the house or taking on more debt. Jason did not build wealth by buying.

He destroyed it. And the worst part is that he still believes he made the smart financial decision because nobody ever showed him the actual math. My name is Bobby and I spend way too much time thinking about the rent versus buy decision that most people get catastrophically wrong.

If you're renting and feeling pressure to buy, if you just bought and something feels off about the math, or if you're trying to figure out when buying actually makes sense for your situation, make sure to hit that subscribe button. What I'm about to show you is a simple calculation that will tell you exactly when to stop renting. and it will probably reveal that the right time is much later than everyone around you is saying.

I call it the 5% rule and it is the break even calculator that nobody in real estate wants you to know about. Here's the fundamental lie you've been told about renting. That rent is throwing money away while mortgage payments are building equity.

This framing is so deeply embedded in American culture that questioning it feels almost heretical. Your parents said it, your co-workers say it. Every real estate agent, mortgage broker, and home improvement show reinforces it constantly.

But here's what most people do not realize. When you own a home, you're also throwing money away. You're just throwing it away in different directions that are less visible than a rent check.

The 5% rule captures the total unreoverable costs of home ownership and compares them to the unreoverable costs of renting. When you own a home, you pay property taxes, money gone, not building equity. Typically around 1% of the home's value per year for a house in decent condition.

You pay for maintenance and repairs, money gone, not building equity, typically estimated at 1% of the home's value per year for a house in decent condition. And you pay the cost of capital, which is either mortgage interest if you borrowed money or opportunity cost if you paid cash. money gone, not building equity.

The cost of capital is usually around 3% of the home's value when you blend mortgage interest rates and the opportunity cost of your down payment together. Add those three components, 1% property tax, 1% maintenance, 3% cost of capital, and you get 5%. That 5% of the home's value is what you're throwing away every year as a homeowner.

It's not building equity. It's not an investment. It's the annual cost of occupying that house and it vanishes just as completely as your rent check does.

The 5% rule says this. If your annual rent is less than 5% of the home's purchase price, you're better off renting. If renting costs more than 5% of the home's purchase price, buying might make sense.

That's the break even point where the unreoverable costs of renting equal the unreoverable costs of owning. Let me show you how this calculation works with real numbers because the math is shockingly simple once you see it. Take a home priced at $500,000.

5% of $500,000 is $25,000 per year, which is $2,83 per month. That's your break even rent. If you can rent a comparable home for less than $2,83 per month, you're financially better off renting.

If renting costs more than $2,83 per month, buying starts to make mathematical sense. Now, let's apply this to real markets. In San Francisco, the median home price is approximately $1.

2 million. 5% of 1. 2 million is $60,000 per year or $5,000 per month.

The median rent for a comparable property in San Francisco is around $3,200. 3,200 is dramatically less than 5,000, which means renting in San Francisco is significantly cheaper than buying on a pure cost basis, despite what every homeowner there will tell you about building equity. In Austin, Texas, the median home price is around $550,000.

5% is $27,500 per year or $2,292 per month. Median rent for comparable properties is around $2,100. That's below break even, which means renting in Austin is still cheaper than buying.

In Cleveland, Ohio, the median home price is around $230,000. 5% is $11,500 per year or $958 per month. Median rent for comparable properties is around $1,200.

That's above the break even point, which means buying in Cleveland might actually make financial sense. The 5% rule reveals something that goes against everything you've been taught. In most major American cities, especially on the coasts and in sunb belt metros that have seen significant appreciation, renting is cheaper than buying.

The people who bought in these markets are not financial geniuses building wealth. They're paying a premium for ownership that the math doesn't justify and they're rationalizing it with the throwing money away narrative because that's easier than confronting the numbers. Now, you might be thinking that appreciation changes everything.

That even if the annual costs of owning are higher, the house will go up in value and you'll come out ahead. And this is where I need to challenge another assumption that most people treat as fact. Home prices do not always go up.

And when they do go up, the returns are much lower than most people assume. According to data from Robert Schiller, the economist who won a Nobel Prize for his work on asset bubbles, the average real return on housing, meaning after adjusting for inflation, is approximately 1% per year over the long term. Not 8% like stocks, not 5% like bonds, 1%.

The value of a typical home roughly keeps pace with inflation and adds about 1% on top. That means if you buy a house for $500,000 today, in 30 years it might be worth about $675,000 in real terms, an increase of $175,000 or about 35% total. Compare that to investing in an index fund at 7% real returns.

Your 500,000 would become approximately $3. 8 8 million. The house returned 175,000 in real appreciation.

The index fund returned 3. 3 million. People overestimate housing returns because they remember nominal prices.

They remember that their parents bought a house for 60,000 and sold it for 400,000 without adjusting for the 50 years of inflation in between. They also remember the exceptional markets. the Bay Area from 1990 to 2020, Miami in the mid200s without accounting for the many markets that barely kept up with inflation or declined.

Betting your financial future on real estate appreciation is betting that your specific market will outperform the long-term average, which is a bet most people wouldn't make if they understood what the long-term average actually is. And here's where it gets really interesting. The 5% rule already accounts for reasonable appreciation.

The 3% cost of capital assumes that you're giving up investment returns by tying your money up in the house. If the house appreciates at the same rate as other assets, you break even on opportunity cost. It's only if the house dramatically outperforms other assets that buying becomes clearly superior.

And dramatically outperforming is exactly what most houses do not do over the long term. Let me talk about the hidden costs of home ownership that make the 5% rule actually conservative in many cases because the real costs often exceed the 5% estimate. Transaction costs are enormous and usually ignored in rent versus buy calculations.

When you sell a home, you pay 5 to 6% to real estate agents plus closing costs plus transfer taxes in many states. On a $500,000 home, that is 30 to $40,000 in transaction costs. Money that completely evaporates and counts against your returns.

If you own the home for only 5 years and sell, those transaction costs eat most or all of your appreciation and can actually leave you underwater compared to renting. The break even timeline to recover transaction costs alone is typically 5 to 7 years. Meaning, if you are not virtually certain you will stay in a home for at least that long, buying is almost mathematically guaranteed to cost you money compared to renting.

Maintenance costs are chronically underestimated by new homeowners. The 1% per year rule is an average, but averages hide volatility. In year 1, you might spend nothing.

In year six, you might replace the HVAC system for $12,000, the roof for 15,000, and the water heater for 2,000. That is $29,000 in a single year. Almost 6% of a $500,000 home's value.

The furnace, the appliances, the driveway, the foundation, the plumbing, everything in a house is quietly deteriorating. And when things break, they break expensively. Renters never think about this because when the HVAC dies, they call the landlord.

Homeowners write five figure checks. opportunity cost of the down payment is the largest hidden cost and the one people understand least. When you put down $100,000 on a house, that $100,000 is no longer invested in the market.

If the market returns 8% and your home appreciates at 3%, you are losing 5% per year on that $100,000. $5,000 annually in foregone gains over 10 years. That is not just $50,000 lost.

It is 50,000 plus the compounding you missed which brings the real cost to over 75,000. Your down payment is not sitting safely in your house. It is sitting there slowly dying compared to what it could have been doing in equities.

The 5% rule captures this in the cost of capital component. But most people never think about it consciously. They think the down payment is invested in the house.

It is not. it is trapped in the house earning the house's return instead of the market's return and the difference compounds painfully over time. Let me be clear about when buying does make sense because the 5% rule is not an argument that renting is always better.

It is a tool for identifying when buying becomes mathematically rational. Buying makes sense when rent exceeds 5% of the home's purchase price, which happens in markets where home prices are low relative to rents, often in the Midwest, parts of the South, and smaller metros that have not experienced speculative appreciation. Buying makes sense when you are certain you will stay for at least 7 to 10 years, allowing you to recover transaction costs and reduce the peryear impact of those costs on your returns.

Buying makes sense when you have maxed out all tax advantaged investment accounts first, your 401k, your IRA, your HSA, and still have excess savings. Because buying a house before maximizing these accounts means choosing a 1% real return asset over accounts that provide both market returns and tax advantages. Buying makes sense when you value the non-financial benefits enough to pay for them consciously.

the stability, the ability to modify your space, the psychological ownership, the community roots while understanding exactly what premium you are paying for those benefits. The problem is not that people buy homes. The problem is that people buy homes under the delusion that they are making a financial investment when they are actually making a lifestyle purchase that often costs more than renting the equivalent property.

If you want to own a home because you want to own a home because you want to paint the walls and plant a garden and never deal with a landlord, that is a valid choice. But you should make that choice with clear eyes about the financial trade-off, not with a false narrative about building wealth while renters throw money away. Here's the framework for making this decision in your own life.

Because I want you to leave this video with a specific process rather than just a general understanding. First, find the price of a home you would actually buy. Not a fantasy home, but the realistic home you would purchase in your market given your down payment, income, and preferences.

Second, calculate 5% of that price and divide by 12 to get the monthly break even rent. Third, compare that number to what you would actually pay to rent a similar property in the same area with similar space and quality. If rent is lower than the break even number, you are financially better off renting and investing the difference.

Fourth, if you are considering buying anyway, ask yourself honestly whether you will stay for at least 7 to 10 years. Not whether you hope to stay, but whether you are genuinely confident that your job, your relationships, and your life circumstances will keep you in that specific location for nearly a decade. If the answer is uncertain, the transaction costs alone will likely eat any gains from ownership.

Fifth, calculate what you could accumulate by renting and investing the difference over the time period you plan to live there. Compare that liquid, accessible wealth to the illquid home equity you would build. Most people who do this calculation honestly discover that the renting and investing path produces more net worth.

They just never did the calculation because the cultural narrative told them buying was obviously superior. Right now, you probably see yourself as someone who is either a renter aspiring to be an owner or an owner who made a smart financial decision. Both of those identities are built on a narrative that may not be mathematically true.

The 5% rule doesn't tell you what to do. It tells you the truth about your trade-off. a truth that the real estate industry, mortgage lenders, and your homeowning friends have no incentive to share with you.

Renting is not throwing money away. Renting is paying for housing, just like owning is paying for housing, just through different channels with different cost structures. The question is not which one feels more responsible or more adult or more aligned with how your parents lived their lives.

The question is which one in your specific market at your specific price point with your specific circumstances produces more wealth over the timeline that matters to you. Jason believed he was building wealth. He was actually destroying it compared to the alternative because nobody ever handed him a calculator that told the truth.

Now you have that calculator. The 5% rule is simple enough to run in your head for any property you consider. And once you see the break even line clearly, you'll never again feel pressure to buy a house before the math actually makes sense.

No matter how many people tell you you are throwing money away by renting, you are not throwing money away. You are making a decision. Make it with numbers, not narratives.

I've spent way too much time thinking about this stuff so you don't have to. If this changed how you see renting and buying, hit that like button and subscribe. I'll see you in the next one.