E expected Market return why would you invest or you could be in which case you won't buy stocks it can't be collectively negative nobody would buy stocks you once you got into negative might as well leave the cash in your under your bed right okay folks you ready for the two questions how many of you have picked a Company for your valuation okay more hands than last time we're moving in the right direction so next Monday question is going to change right how many of you have not picked a company so hopefully the numbers will

shrick how many of you are not in a group yet so those 15 names that I see on the orphan list they're not orphans anymore you've been adopted there a lot of names there I it's still there so if you're no longer an orphan remove your name from that list right you're not not in that list anymore so at least people know that they need somebody for their group so today we're going to continue our discussion of risk free rates we're going to complete it but we're also going to start on this mysterious concept which

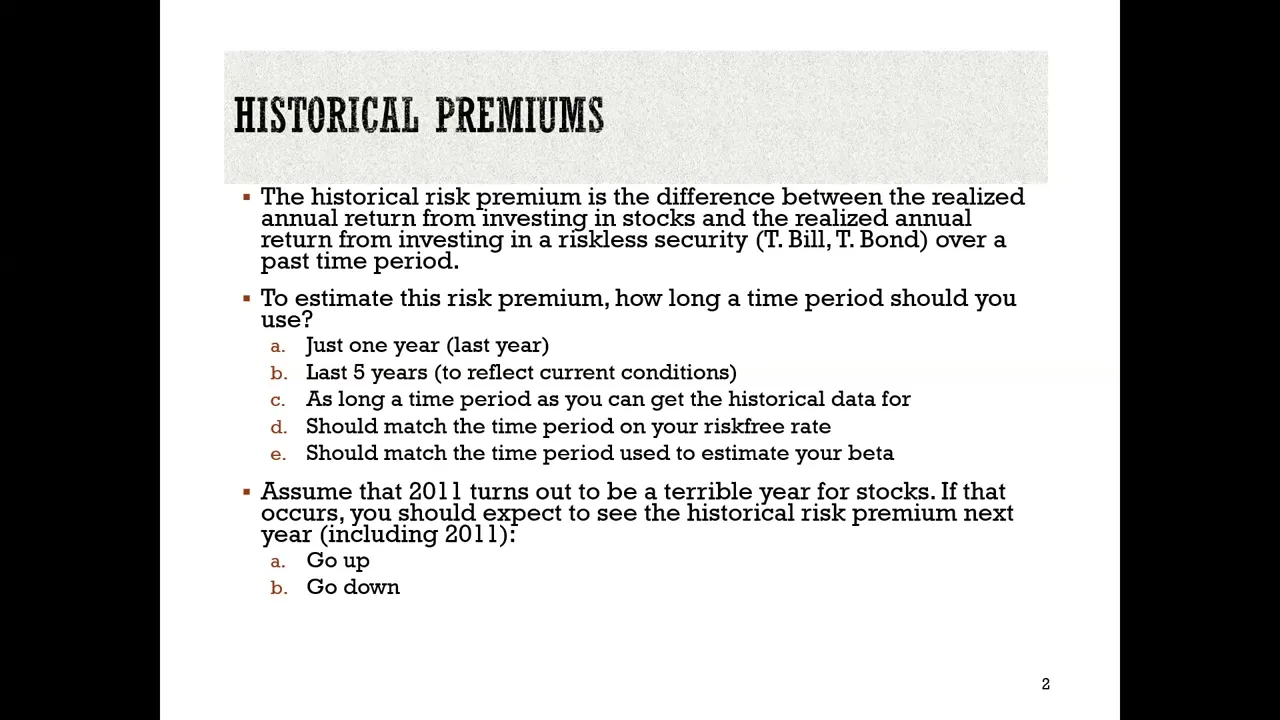

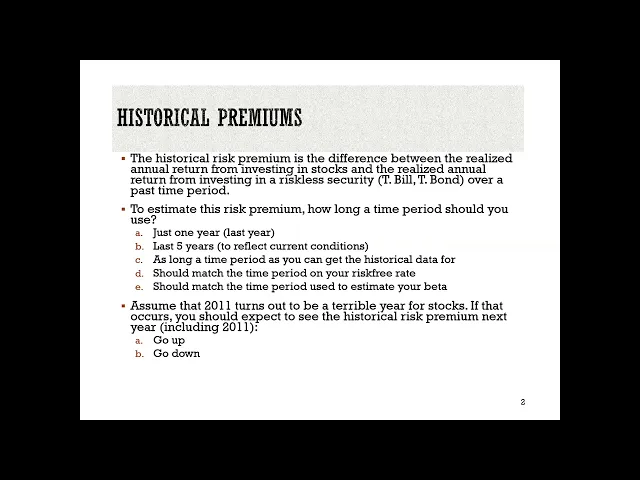

is the equity risk premium which is what you would demand over and above the risk free rate to invest in Stocks collectively so I'm going to start today's class with a test about the equity risk premium and lay the foundations so how we think about estimating it best so the tough thing about Equity risk premiums is you're trying to estimate you're trying to estimate what people think they can make on stocks over and above what you can make on something risk-free right so What's the most logical place if I asked you what do you think

you'll make on stocks over and above T bonds what's the most logical place to start Look Backwards right we have 100 Years of stock market data in the US and if you take a 100 years stock market data you can SL slice and dice it you can use a historical past and if you're doing it you're making an assumption right you're assuming that the future will look like the past but we do it in so many other Places why not this is the default way in which people estimate Equity risk Brams especially in the US

they look backwards a lot of history and they use it as a prediction for the future so let's say you decide to go down that path here's my first question you want to estimate the equity risk premium for the future you can just look at the last year what's the most recent data what did the number look like last year what did stocks do does does anybody Know 25% right roughly 25% so what was the and and you know t- bonds earned last year right minus 1.6% because the price actually went down so the equity

risk premium last year was 26.6% you want to put that as in your Equity risk it' be nice if we could make that but there's no way you're going to get that right so what's the problem with one year could be a good year it could be a bad year it could be a so clearly not one how about the last five Years you think that'll be good enough what's the question you're really asking right the statistical question how noisy is the average in statistics classes how do we measure when you comp put compute an

average of a bunch of data what do you train to put in Brackets below it to indicate to the world how uncertain you are a standard error right a stand standard deviation but a standard error basically saying it could be plus or Minus you know what a fiveyear number is going to look like the plus or minus is going to wipe it out at five years I've heard people say well if I'm going to project out cash flows the next 10 years I should look at the last 10 this is nothing to do with what

you're projecting out for so that shouldn't even enter the equation there others there you a 10year bond rate one no nothing to do that that ultimately what you're trying to do is Even if you believe the past is a good Pro estimate of the future you're trying to come up with a number that you have some degree of confidence in and I'll give away where I am there is no historical time period you could give me where I feel comfortable enough with the number you're going to give me that I can value stocks for so

I have to give you an alternative but this is how 95% of valuation the equity risk pram looks comes from looking at The so I i' I've made up a year let's say that you're coming off a terrible year for star we haven't had once since so let's make it 2022 terrible year for stocks down 20% you're Computing a historical risk premium with that year added on so basically you've been doing a track the data in the US the most widely used data set is from ibits and Associates go back goes back to 1926 just

gets updated with the most recent year so let's say you Computed through 2021 and it was 52% then 2022 happens and it's minus 20% you add the minus 20% to history historical data what is that going to do to your Equity risk premium decrease it or increase it it's going to drop it right you think so what so you're coming off a terrible year for stocks and what are you telling me I'm going to demand a lower risk premium from this point on which makes no sense at all right you come off a Terrible year

you're feeling scared you want a higher risk premium that's the second problem with historical risk beams is they cut in the wrong direction after a crisis year like 2008 or 20 22 your historical risk premium gets smaller and at the same time you're feeling more risk in the picture so what would you like you'd really like a forward-looking number that reflects the world you're in and I already said this is going to be a rocky semester because Things are happening right I don't want to go back and look at the last 100 years I going

to live in the moment I want to get a forward-looking number and I'm going to give you a way of doing it but I'm going to get you started on that right so I want somebody to be my guinea pig in this process so you're going to be my guinea pig okay so what's your name again AER is going to be my guinea pig I'm going to offer him an investment where I can guarantee a dollar in cash flows every year in perpetuity and how much would you pay for that investment okay so so $1

is your cash flow it's constant it's a perpetuity so I need a discount rate what did I say it's guaranteed in US dollars so right now that rate is going to be a t bond rate for but let's say it's 5% let's round it up right one over 0.05 which is $20 you see why $20 is a fair price right you pay $20 5% of this so you'd pay $20 I'm going to up the anti a little bit Tyler I'm going to come to you with a dollar every year forever but it's not guaranteed anymore

right don't but I'm going to let you set the price obviously would you would you pay $20 now that it's not guaranteed no less or more way less let's not go to the way less yet less right you see why right so give me a number how much would you Pay 10 bucks okay if you pay 10 $10 has Tyler given away what is R premium is looking forward with the $10 investment what are you making 10% on this investment you have a 5% Equity risk premium over the risk Cree you see where I'm going

right the way I'm going to compute a forward-looking premium for stocks is I'm not going to ask you what risk premium would you like to make I'm going to look at what you pay and when you get scared what do you do you push Down what you pay you push up your risk premium and will that number change every time the price you pay changes the risk we have a forward-looking dynamic premium a lot of do eyes to Dot and teas to cross but that's where we're going to end up on the equity risk premium

discussion we're going to start with the prevailing status quo look at the past and I'm going to tell you everything that makes me uncomfortable with using that and I'll also make a confession Before 2008 I used to let people get away using historical risk premiums post 20 8 I think you even lost the Fig Leaf we say what happened in 2008 to change that that that shift away but today we're going to talk about risk FR so before we do that though I want to kind of finish off the risk free rate discussions inspection so

let's go back to where I left you in the packet if you remember I I came up with three different ways of Estimating the default spread for Brazil remember the three ways were I could use a Brazilian dollar Government Bond compared to the USD Bond and take the difference it works only if you have a dollar Bond so if Russia has a Euro Bond I can compare to the German Euro Bond and take the difference that def fall spread that number was 3.17% the 10e Brazilian government bond rate in RI was 12.3% I subtract out

the the default Spread I come up it should be 9.13% so fix that type of 99.13% I'm subtracting out the spread from the 12.3% the second approach I looked at the CDs spread 2.82% If I subtract that from the 12.3% I get 9.48% the third approach is to use the local rating which has a default spread of 2.83% you subtract that out you get a nine so I get three different risk free rates right 9.17 to9 if I just picked based on the risk r r and you wanted to Get a high value for your

company INRI which one are you going to go with the lowest or the highest yours lowest because you want a low risk R rate I'm going to make a statement that's going to sound absurd but I'll back it up it doesn't matter which of the three you pick as long as you stay consistent see consistent what Sense little later in the process we're going to open up the box of equity risk premiums for countries like Brazil and There we will have to come up with the default spread to come up with the equity risk premium

and there I'm going to ask you what default spread did you use to get the risk free rate and I'm going to make you stick with that same default so if you pick a high default spread which gives you a lower risk free rate that's now going to show up as a higher risk premium it effectively will keep you in check and give you so don't sit here two hours trying to pick which Of these three just pick one and keep moving at least remember which one you pick and then come back to it later

in the process so we looked at three tests let's move on to fourth one let's say you've decided that you want to do evaluation in real terms I'll tell you in the US I almost never encounter valuation or a project analysis done in real terms partly because the world lives in Ninal terms in fact on April 15th try filing your tax return in real terms so I infl i' have income but I'm going to take inflation out of it and I'll pay taxes on my real income it doesn't work that way the world operates in

noral terms so it's easier to stay in normal terms when would you do things in real terms when inflation gets to be 20 25 30% you finally throw up your hands say this is Too volatile and too messy I'm going to do things in real terms so you're more likely to do this in Honduras or Argentina or Venezuela then you are in the US and to do things in real terms you need a real risk free rate and remember I showed you a real risk free rate last session the tips rate right you saying but

that's a US real risk free rate a real risk free rate actually is a real risk free rate there's no us attached to It and in a world where there are no barriers to Capital and trade and that's a big F A real risk free rate should be a real risk free rate all over the globe and here's why let's suppose I told you the real risk free rate is 2.3% in the us and 4% in Brazil and capital flowed freely tell me what's going to happen it's going toor us the capital will move from

the US until what happens the 4% moves down to 2. I know that in The real world there are barriers that prevent but if you're doing evaluation real terms I'm going to give you an escape hatch but I want you to have the explanation ready because somebody's going to challenge you on it so you're valuing a v velan company in real terms you pull the US tips rate and make that your real risk free rate you're going to get push back right it's a Venezuelan company using a real risk free rate in the US and

the only defense I can offer Is you know in a world where things converge this is as good a start as possible so it's not perfect but you can see why the tips rate can be used as a risk free rate pretty much anywhere in the world that you're doing a real valuation a real analysis a real project assessment now let's go back to a question I asked you at the start of last session right we talked about risk-free rates in different currencies and we talked about How to estimate so now we have a way

of estimating risk free rates so start of 2025 I estimated risk free rates in about 40 currencies you know I had to stop at 40 I needed a government bond rate in the local currency to get started and there only about 40 currencies where there's a local government bond rate in that currency then I cleaned up like I did for the Brazilian so the the great part of this graph are the risk-free rates in Different currencies I think you kind of answered this question last session but since it's such a critical answer I want it

to be affirmed why do risk free rates vary across currencies I didn't ask why do Government Bond rates right it's why do risk free rates vary across currencies what's the answer to that question yeah yes inflation that's it it's the only thing you're saying but don't risky Countries have high no it's if it's truly risk free I've taken out the risk effect the only thing that causes in Risk free rate so high inflation currencies will have high risk-free rates low inflation currencies will have low risk free rates and deflationary currencies will have negative risk free

rates it can happen so when you look at difference in inflation you'll essentially see risk free rates varing can risk free rates Change over time of course why because inflation changes over time this is from 2020 risk-free rates in the US Treasury rates collapsed there it is right between that's the start of 2020 through not even the start February 14th of 2020 through March 23rd across the board rates collapsed why Co shut things down inflation kind of dissipated right what what could you Go by consumption dropped off real growth of course dropped through the floor

so not only do risc free rates vary across currencies they vary across time I have some bad news for you you value a company today what's your risk free rate you're doing it in dollars 4 and a half% when is your project due May 5th you might have to at least change the risk free rate closer to that day you don't have to redo the whole Valuation but it could change your buy to a sell so don't won't pull the trigger on buy or sell till much later in this process because who knows what rates

will be 10 weeks from now rates can change across time different across currencies but if inflation is the reason why rates vary across currencies and now have an opening on how to estimate a risk-free rate in any currency remember I showed you the graph with 40 currencies which said government Bonds there are lots of currencies on that not on that list the Egyptian Pound The V and so you can go down the list you saying what do I do with those currencies here's a quick and easy way to get a risk free rate in any

currency in 2015 I was valuing an Egyptian bank and I really really really wanted to value in Egyptian PS because I never valued a company in Egyptian PS I went looking for a Government Bond Right none the Egyptian government borrows money but it borrows from the World Bank it borrows from Banks it doesn't issue bonds so here's what I did I started with the USD Bond R you saying that is so us Centric guilty is charged but I trust the t-bond rate because it's a traded rate there's demand and Supply setting it and it was

let's say 2% I'm sorry it was uh it yeah it was roughly 2% so this was risk free rates were low And then I estimated two numbers one was the expected inflation rate in the US which then was one and a half % and the second was the expected inflation rate in Egypt which is 15% let me pause right there the Egyptian inflation rate is roughly 13 a half% higher than the US and if inflation is the reason risk-free rates should be different the risk free rate in Egyptian Pound should be roughly 13.5% higher than

the USD bond rate so if you're in a hurry you take the two And you add 13 and a half you come up with 15 A5 per. you're saying what's this convoluted calculation you did rates know rates are have a compounding effect inflation is on top of real rates if you want to do it more precisely you take one plus the US dollar rree rate you take one plus the inflation rate effects and you come up with a more refine you see why if you're in a hurry I'm going to let you get away with

15 a half% after all the refine you got 15.57% do the full calculation there the effect will be large enough that you will notice at this point you have no excuse on any currency to say you cannot come up with a risk free rate in that currency as an estimation question of the numbers here what might be the number that you have trouble with t bond rate you should be able to get right inflation rate in the US is Trivial it's easy to get all you have to do is Compare two Market numbers what are

the two Market numbers that you can compare to get an inflation rate T bond rate and a tips rate make them both 10 they're both so you can take that difference which leaves you with the number that you're going to have trouble with how the hell am I going to get an expected inflation rate for Egypt try the IMF for the World Bank site they have estimates of expect inflation are they going to be wrong or 100% of the time but as long as you use that same wrong inflation rate in both your numerator and

your denominator you're going to be okay again this is not the you want to spend days on it's not worth it make an inflation judgment come up with a risk-free rate and move on so on January 1st 2022 the 10year t- bond rate in the US was 1.51% two seme two two Springs I measure my teaching life in Spring semesters That was two spring semesters ago three spring semesters ago one and a half% historic lows right so when you look at a rate like that and you're you're an analyst you say that rate looks too

low it's human nature so what do you want to do you want to replace it with something that you feel more comfortable with so in that decade when t- Bond rates were really low there were practitioners who replaced it with what they called a Normalized rate we talked about this being a subject so you could take for normaliz you could take an average over the last you know 30 years you know so basically you could replace the current rate with that or maybe you can use a current risk free rate and keep moving so the

question is should you replace a rate that looks too low or too high with something that you think is more normal what do you think what sounds more realistic if you do the first few Years risk period that you have and then adjust it four years five years down the line to what something more consistent last 10 years but should you be measuring consistency with the last 10 years or consistency with the inflation numbers you're using in your cash flows you see where I'm going right so if you tell me that inflation is coming back

after year five and rates will go up then that inflation should also be showing up in your cash flows which Means the net effect of changing your risk free rate is going to be far more neutral than you think because whatever you do to your risk free rate you should also be doing to your cash flow so if inflation is a driver my advice to just leave well enough alone you have enough on your plate already what the heck are you doing trying to forecast interest rates for the next decade leave the t- bond rate

at 2% but Then use a really low inflation rate when you do your cash flows you won't get that assist and that's going to keep your value so consistency here just means whatever inflation you're building and and that's part of the reason I would not try to replace current rates and as I said last week you tell me how old you are and I can tell you what normal looks like most of you look at a 4.5% rate and what's Your reaction looks really high why because you've lived in a world with 2% rates I

had a 71y old in my valuation class alumni are allowed to take my MBA value ation class he started in the market in he got his MBA in 1978 he looked the 4 and a half% and say what do you think you know he said it looks really low because his frame of reference is 198s T Bond rates was 6 and a half seven 7 and a half% normal is not some magical number it reflects you know that what we Define as normal is set around 30 to 35 years when we so what you see

then so what you think of as normal music is what you used to so you notice that you know when you get to be 65 you who listen to the crappy stuff what is this you know it's just a reflection of the fact that your normal got stuck on 30 and that's part of the problem here is you're you're stuck in time and you Can't really let go so I know it's tough to do an analyst break this rule all the time try trying to for I in fact in my spreadsheet I allow you to

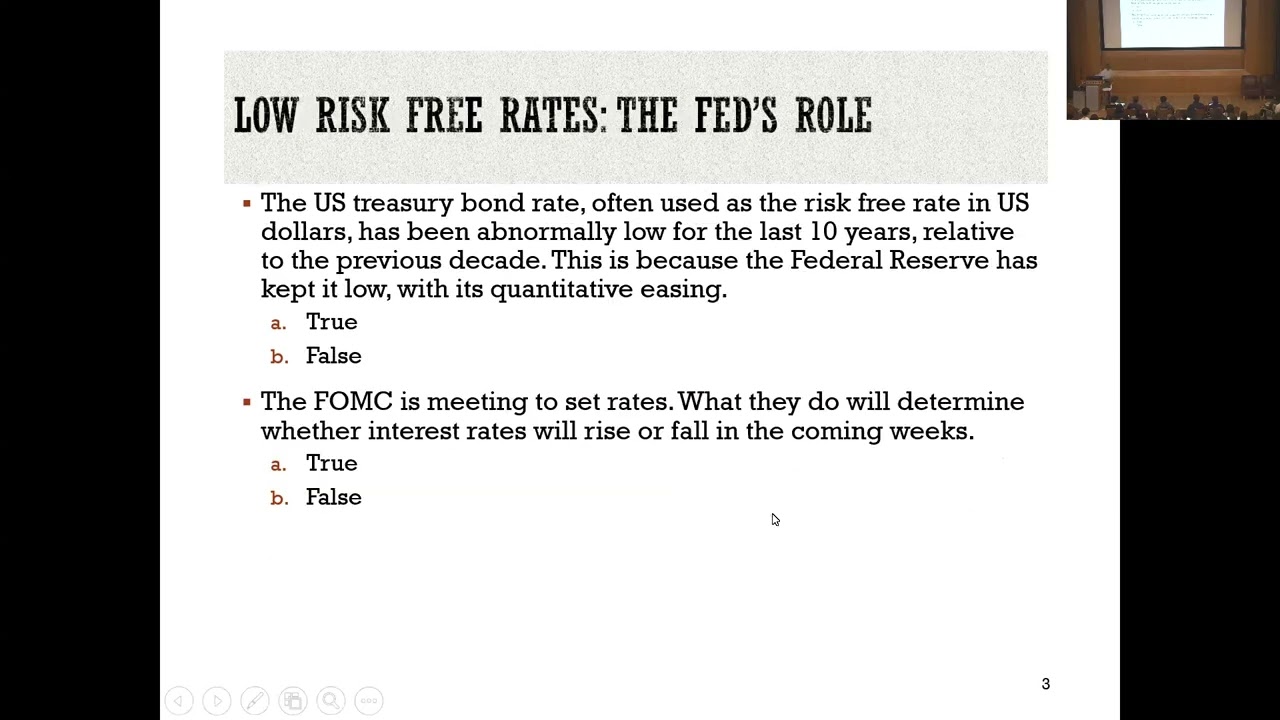

change I will give you the RO to hang yourself if you want to do it but I want you to think long before you pull that rope out and say do I really want to do this and that's the other question remember the fact that rates were low for the last decade who we blame the FED Did it everything the FED did it that's an incredibly lazy answer why ratees low the FED did it why ratees High the FED did it why ratees vola the FED did it removes all responsibility from your shoulders is why

rates change it's true rates in the last decade were low but to show you why they're low I'm going to create what I call an intrinsic risk free rate I've been doing this for a long time in terms of computing this number I'll tell you what I do what did We say goes into risk rate expected inflation and an expected real interest rate right I took the inflation rate every year I know it's reaching and but I took the so let's say the inflation rate is 3% I took the the real GDP growth in that

year say it's 2% add 3 plus two you get five that's my intrinsic risk rate that's that's basically what you're getting in these columns red number is the inflation the Green is the real GDP growth that's my intrinsic risk re rate the black line is my actual t- bond rate do you think the two seem to move together you can do the correlation if you want you can see there are your but clearly the trend lines match up the correl I think was 88% look at the last decade 2011- 20 what do you notice lowest

inflation decade in a century and in terms of real growth and Neic real growth what's low plus low low why were rates low in the last decade it wasn't the FED it was low inflation plus low real growth did the FED at the margin effect rates that's that's causing that noise around the number of course it does fact in 2022 rat shot up and people blame the FED what happened in 2022 mean you started paying for things and noticing that things were going my burrito which was at 9.99 for an entire Decade became $14.99 she's

burrito who cares but that played out across the market right we saw 8% inflation for the first time since the 1970s inflation was back and guess what the t- bond rate did it went up what did the FED do chase the market it raised rates but it was chasing the market all the way through so when you look at rates I want you to remember ultimately it's Inflation and and real growth that drives those rates a Fed at the margin can do only so if at some point in this year rates go up and you

say why isn't the FED lowering rates you can't do much if inflation is back and real growth is strong final point about risk free rates talked about currencies with negative risk free rates and it does freak people out I understand why it freaks people out it's changed I mean all these Currencies now are back to positive numbers but the Swiss rank the Euro the Japanese yen in 2019 all had negative risk rates it's kind of unnatural right it actually re created these very strange things in Europe where Danish homeowners who bought a house with a

mortgage the bank mailed them a check every month because the mortgage rate had become mildly negative it's not Something you even think about you say I borrow money and you pay me this is amazing but that's what negative rates do is it kind of turns the whole word on its head but there's a problem with negative rates right you can't go below a certain number why are you required to put your cash in a bank so if I say the rate is minus 1% you just hold as cash you keep the money right you're saying

why don't people Just keep the cash when you have negative rates let's say you have 10 million do let's say you decide to keep it all at home first don't tell me where you live because I might pass the message on you first have to hire you know all kinds of security and you know who knows we you might have things eating through paper and the currency gets eaten the problem is we we've created a world where cash we don't use cash Anymore we create the 50 years ago interest rates might not have turned negative

because we were used to carrying cash paying with cash I've been behind people in a line whose Apple pay stops working and it's almost like oh my God my life is done what am I going to how am I going to pay have you ever seen this thing called currency might want to put in your pocket just in case in a cash free Society rates can turn negative but they can't become minus 10% There's a Tipping Point where people will just hold the cash or just but rates can turn negative and if they do turn

negative the question is should you continue to use them because remember you start with the risk free rate and build up to it you start with a negative number going to come up with a low cost of equity and low cost of capital so that was the fundamental question I was asked from European analyst is hey Euro risk free Rates look negative should I make it positive you know how some of them made them made it positive they took the minus and they drew a line through it say it looks plus it's a it's magical

you can't do that right others use the normalized approach take the average rate over the last 10 years but that became a fundamental question so we'll come back and talk about it because I'll value hinin in September of 2019 the Euro risk free rate was Negative and I'll give away what I did I left it negative but then when I did cash flows and growth rates you saw that same negative phenomenon kicking there I actually found hinin to be overvalued not undervalued even though rates were negative which dispenses this whole mythology of rates get really

low or they get Negative the value is going to explode through the air just be consistent you control both the discount rate and the cash flows as long as You're consistent by assumptions you can use low rates High rates negative rates and it's all going to even out yes those banks have negative rates was that government enforced or do the banks it's Market set right it's demand and Supply the T the Euro the German Euro Bond it's demand and Supply there were Bond buyers actually willing to buy these bonds with negative rates banks in a

sense are you know triggered to that so it's it's it's got nothing to do with Government regulation just you an deflation environment negative growth the bottom falls out let's talk about uncertainty now a lot of stuff on this page but my point when you talk about Equity risk premiums is everything affects it let's go through the list first doesn't depend on your risk aversion as a person absolutely and what what determines risk aversion first yeah one is life Experience but some of it basically you're born with right I have four kids I can tell you

which one of my kids is going to be invested in fixed income for the rest of his life and which one's going to be the option Trader my oldest son he's 35 still walks down the stairs holding on to the banister I might fall now how about right now fixed income guy if you ever saw one my youngest when he was 2 years Old took off from the top step expecting to be caught before he hit the bottom option Trader to the core right so some of this you're born with second do you think age

matters are older people more RIS ofs or less risk of why because you've learned what life can dish out you're older you're more responsi is so you know what the implication is right as a market ages what should happen to equity risk premiums should actually get higher Because you know the Japanese Market has a demographic problem Equity risk are going to be higher there the Chinese market is a demographic bomb waiting to go off and if Equity risk Reams go up what we what's going to happen to stock prices they'll have to go down because

you'll have to get a higher return to compensate do you think I'm I'd be treading on dangerous territory that your sex matters men more risk ofers Than women or what do you think that young women are more risk averse than young men my four kids learned how to drive the only one of my kids whose car I would get into when they drove was my daughter because I've seen what 20-year-old men can do in a car and it is terrifying young men are actually the most dangerous risk staking group you can think of and this

is what I want you to do next time you go to Investment Bank walk into the trading room and look around and what are you going to see 25y old men maybe 30 if they're old in front of computers playing with tens of millions of dollars so after one of these trading scandals I wrote a piece on my blog it's still there suggesting how Banks can take care of this problem first is you can make your Traders more diverse that takes a long time I said here's what you need need to Do what's your only

check on a 25-year-old male taking too many risks a mother a mother not a family they don't listen to their siblings right they'll actually take more risk father who cares what he says so he said here's what you need to do you hire a Trader hire his mother too make her sit in the chair behind saying what are you doing now it'll slow the process down so what you don't don't Don't do that it's good to have your it's the greatest risk tool you can think of you say but I have to pay the mothers

hey think $100,000 a year for not having that $2 billion trading Scandal it's well worth it risk aversion varies across people does it vary across time yeah I mean remember Co you started the 2020 feeling pretty good in my March 2020 I don't know whether I have a future left It can vary across people it can vary across time second more economic uncertainty will lead to higher Equity risk premiums little later in this class maybe in the next class we're going to talk about why Equity risk premiums vary across countries okay if you're in Venezuela

you feel an immense amount of course your Equity risk Prem is going to be hard but even in a market like the us as You go through time could you feel I mean mention of a tariff does increase economic uncertain I'm not taking a political stance here it just makes the future a lot more uncertain your Equity risk premiums will reflect third inflation and interest rates I'll tell you the problem is not inflation per se that does cause rates to go up it's when inflation goes up it also becomes more unstable when inflation becomes unstable

it basically makes everything more risky Higher Equity risk bres do you think the way information comes to equity markets affect Equity risk premiums where does the information usually come from comes from companies which are required by Disclosure to reveal it and if there are holds and disclosures in that's going to affect your Equity risk PR countries where disclosure laws are not as complete will have higher risk premiums than countries without what about liquidity yeah you're In a market where you don't have much money flowing into the market Egyptian Market at one point in time you

know how they recorded trades there was a guy with a CH board I'm not kidding in front of the exchange and every time there was a trade he wrote in chalk what the trade was you want to try that in the New York Stock Exchange you couldn't keep up right but there were so few trades they could actually didn't even fill the board so You're a market where there's a lot of liquidity the equity risk premium should be lower than in the market where liquidity dries up but even in a market like the US are

there periods of liquidity dries up I remember October 2008 G could not Place its commercial paper largest commercial paper issue in the world was unable to place the commercial paper because there weren't enough people willing to buy it higher Equity Risk premiums what about catastrophic risk I won't I won't don't mean to scare you but you wake up one day and you hear about a nuclear bomb that's been La I'm I'm sure you'll have other things on your mind than Equity risk premiums but worries about nuclear war will play out as a higher Equity risk

premium so that's catastrophic risk can government policy affect Equity risk prams yeah so if you're if you have a Government whose policy is unstable it keeps CH the equity risk premiums will have to reflect and finally can central banks affect Equity risk premiums I think so and I'll tell you why a good Central Bankers should be in the old days when you children you know what you what what they used to say right they should be seen and not heard a terribly cruel thing I'm sure in Hinds side but Central Bankers should be seen and

not Heard because when they talk too much and they talk about what they're going to do they can add to the mix they can add that's a long list right you're saying everything affects Equity risk frams Welcome to the Real World that's exactly right everything that happens around you small or large is affecting Equity risk beams which means Equity risk premiums can never be a constant number this morning I was when I was teaching my my corporate finance class Somebody works at um at a regulated company came in and said is there a way I

can get a way of getting Equity risk premiums where it doesn't change much over time I want something nice and stable I said you live in a world where everything is changing picking a number that's stable might make you feel more comfortable but it's not real a good equity premium number should be unstable should reflect the times Here so let's start with the conventional way in which most people still estimate Equity risk premium they look backwards and when you look backwards there are two things you're assuming first is the things will revert back to the

way they used to be it's called mean reversion it's a very and and I'll admit it's a strong force in businesses and markets things revert back often so if you have a basketball player who Historically has shot know 45% of his three-pointers and he's shooting 20% you say well he's just having a bad patch and odds are that if you watch him over another 10 games but if it's Steph Curry that might not work why he's got a great lifetime average he's shooting well below that lifetime average this season why is assuming me version not

going to work he's getting older there's been a structural change in the Process you can sign Mike Scherzer but he's not going to win or pitch with the RAF because he's older you saying what's this got to do with historical risk breams when you look at the last 100 years of stock market in the US and you get Equity risk premium not only assuming Equity risk premiums mean revert but you're also assuming that the US Equity Market has not really changed you see why the 2008 to me was the wakeup date for this what did

2008 show Us first that the line between developed and Emerging Markets was a hazy one there was this Gray Line on any given day who knows what any Market could look like the second you didn't you shouldn't have needed the reminder but a lot of us got the reminder anyway that the US was not the global economy anymore that we were all connected at the hip in other words it was saying the structure has changed what the heck are you doing looking at 1926 through 2008 Averages but people continue to do it so let's look

at what the numbers look like on my web page I update this at the start of every year I never use it but I update it anyway so basically this is my version of the historical risk premium you might find in one of the know one of the commercial sites out it's very close because we draw on the same data it's the same market now There's my historical risk premium for the US let me rephrase it these are my historical risk premiums for the US plural is it how come you have many depends on what

slice of History I look at I can go all the way back to 1920 28 which is my starting year I could go back 50 years I could go back 10 years I could go back 20 years each slice is going to give me a different number it's going to depend on what I use as my risk-free investment t- bills are Shortterm T bonds are long-term might get different numbers it even depends on how I compute my average sounds mysterious right there are two ways you can compute average the conventional is if I have 100

Years of returns I add 100 numbers up and divide by 100 that's a simple average the second is what's called a compounded average the nature of investing is returns compound I'll give you a very simple example to bring it home let's Assume you have a $100 today you invest in something it doubles next year so what's your percentage return next year 100% And the next year the year after it hals what's the percentage return in year two then if it Hales minus 50% you know what the arithmetic average return over the next two years is

no no it's plus 25% through the magic of averaging I've convinced you that even though you start with 100 and end with 100 you made a 25% Return that's the problem with arithmetic averages the truth is you made nothing you're back to where you started and geometric averages capture that so let's look at the range of numbers here it ranges from I think the lowest value I got at the start of 2025 was 5.44% and the highest number I have is 13 and A5 per. you see why I coulded research analyst like a table like

this remember we talked about Bias what is bias we want to come up with a high number for a company you're going to pick an equity which which premium are going to pick if you want a high number for your company the lowest number or the highest number you're going to go with the lowest you want a low number for your company you pick the highest it's like being in a buffet you pick the equity risk premium want to get the answer you wanted to see it's a recipe for disaster and they forgotten Basic statistics

remember those standard errors when I tell you the historical Equity risk pre for the us over t-bot and I'm going to stick with t bonds because my risk free rates a longterm and I'm going to stick with geometric averages because discounting compounds 5.4 if you if you force me to pick a number on this table I'd pick 5.44% then I'm going to put a caveat the standard error in that number is about 2.12% somebody want to help me out there On what that clear why don't you tell me what if I have a 5.44% equity

risk premium and I so let's round it up 5.5% Equity risk 2% standard error tell me I I know nothing about statistics you have the data tell me what that tells you about the equity risk cream going forward with one standard deviation and when you do that well how much confidence do you have in your number 67 which means you can be wrong one/ third Of the time that's a lot of time I could you be give me something more precise 95% confidence two standard errors and with two standard errors what are you telling me

it could be anywhere from one and a half to 10% fat lot of good that does mean a valuation right and that's exactly what people are building valuations on a number that's got such a wide range it could be 2% it could be 10% it's backward Looking and it's definitely noisy there's a reason I haven't valued a company with a historic rpr probably in 25 years it's this re I don't trust it I don't know what it tells me about the future so the estimates are noisy and you you know I like the word noisy

but it's basically reflecting the statistical standard error see look at an even longer time period in the US you can go back to 1871 There's data going back to 1871 but there you run into a little bit of a problem you have more data but you know what the US Equity US economy and the US Equity market look like in 187 anyone come out of the Civil Wars it was an Emerging Market the market itself has changed so trying to get more data is not going to solve this problem there is no escape hatch if

you just keep digging and digging and digging trying to get more data and Second there's another problem when people use this us Equity risk PR they use it outside the US as their Equity risk Prem the most successful Equity Market of the 20th century was the US and what have we done we've estimated the equity risk Prem you would have earned in that market but let's say it was 1919 you were a wealthy person and you wanted to invest your money you had no idea what was coming the rest of The century I would think

you know the biggest Equity Market maybe Austria is said I'm going to send my money to Austria 25% of your money what happened to the Austrian Equity Market you think after the second world war got wiped out my like by Russian investment in luk oil one of the problems with using historical prems in the US is you're probably overstating your Equity risk because you've let survive it's called survivorship bi you pick the most Successful Market you reverse engineering and you're trying to apply it for the next 100 years so file that away historical RS are

under reliable but I'm going to take a little tangent here and come back to talking about better ways of estimating Equity risk groups if it's difficult to get a historical risk premium for the US it's a nightmare to get it for countries outside even European markets did not Trade they actually have this break in the historical data 1940-45 the US contined to trade but many of the markets sto trading so you you have to start if you take a market like India this the stocks have been around a long time but you go back to

1960s 1970s you had probably 20 companies that accounted for all the trading very IL liquid Market if you're lucky you might have 20 years 25 years of data and if you if you went back to the previous page and Looked at the Standard air as my time period goes from 100 years to 50 years to 10 years my Standard air gets larger no surprise purely statistic I remember a Vietnamese analyst emailed me and he said look I'm having trouble getting you know I'm valuing the company he said can you look over the valuation and I

said I will because i' never seen a Vietnamese company actually Val I was curious I look through and he has a risk premium For Vietnam an equity risk premium said where' you get it he said I Ed a historical Equity risk premium for Vietnam how long have Equity markets been in Vietnam if you're lucky maybe 15 years 12 years yeah 10 years of data he said the risk premium is 6.83% he had the second decimal point nailed down and I said you might want to estimate the standard error in that number before you use this

because the standard error is Actually 8% which means you basically know nothing about the equity risk PR by looking at the past so you can't go back because you don't have historical premiums so if I were a brazili if I wanted you to Value Brazilian company you have two choices one is you can say come back in 100 years I'll have enough historical data to estimate your risk premium but my guess is you're not coming back and I'm not going to be around the others to do something today so I'm going to give you a

pathway to estimating Equity risk beams for markets that don't have a lot of history and I'm going to use a number that we've already used in the context of risk free rates so let me do a logic exercise let's suppose you have an equity risk premium for the US right see you feel whatever you know and we talked about historical PR noise you but at least you have 100 Years of data and You're trying to estimate a risk premium for a country an Emerging Market a Vietnam or Brazil if the Equity risk Prem for the

US is 5.44% would you expect the equity risk premium in Brazil and Vietnam to be higher or lower higher right so you can only figure out a way of how much higher make our lives a lot simpler so I'll give you the first way you can come up with the equity risk premium for a Brazil or Vietnam you start with the US Equity Risk premium and remember that default spread that I used to clean up I'll bring it back into play and say I'm going to add it to my us Equity risk premium to come

up with an equity risk premium for Brazil so in um in in 2025 let's say my us Equity risk is 4.33% I'll talk about where I got the 4.33% later remember the default spread I came up with for Brazil 2.83% based on the rating you add the 2.83 3% to the 4.33% you come up with an equity risk Premium for Brazil of 7.16% so basically I start with the rating I come up with the default spread you can use a sovereign spread if you don't like ratings add it to the US premium this is if

you can call it that the state-ofthe-art of estimating Equity risk premiums at investment Banks they take they have a base premium for the US God only knows where it comes from they added the spread now do you see why took that Spread out of your government bond rate because if I did not do that you'd be double counting the same spread right once through what you call the risk free rate and once through this risk bre yeah that's well when it's used as a default spread you basically saying That's Country risk but I think you're

on to something that default spread of 2.83% is for doing what buying a Brazilian Government Bond Right but that's not what you think of doing you think of buying Brazilian equities now again I'm going to ask you in two question and I'll come back to you are Brazilian are equities riskier than Bonds in a country or safer riskier why because you're always the last guy in line so you'd expect that additional risk premium for Brazil to be greater than 2.83% to the extent that equities are Riskier than debt 30 years ago that's exactly where I

started because this is what investment bankers showed me and I say I see where you're starting but why are you stopping there the 2.83% is the default spread here's what I'm going to do to converted into an equity risk Brave I want to measure how risky equities are in Brazil and how risky bonds are in Brazil and I'm going to use a very simplistic measure of risk for equities I took the baspa which is the Brazilian Equity index I computed the standard deviation from the Brazilian in the in the equity index to be 30% then

I took that Brazilian Government Bond on which my default spread was 2.83% I computed the standard deviation that number to be 18% Let's do an algebra prom if you're buying a government bond with an 18% standard deviation you're demanding a 2.83% spread you're buying Equity with a 30% standard deviation Your spread should be roughly scaled up to capture that additional volatility the 2.83% then becomes no so you can I'm sorry I'll go to it becomes 4.25% and you essentially have an equity I'll come back to the previous page so basically it come becomes a larger

number so I've taken the default spread approach and have adjusted the default spread for the higher risk of equity he's saying what was that middle page Goldman Sachs about 30 years ago came up With a different way of trying to scale for risk they said government they didn't use the Government Bond at all they started with the US Equity risk premium and they looked up two standard deviation just like I did but the standard deviation they looked up well one was the standard deviation for the baspa 30% and the other was the standard deviation in

the S&P 500 you see what the algebra looks like that right the S&P 5 is 18% standard Deviation My Equity risk premium is 4.33% if Brazil's Equity index has a 30% standard deviation its risk premium should be much higher based on that percentage you get an equity risk premium of 7.22% already again just like the risk free rate you can see numbers changing depending on which approach I used I almost never use the default spread approach because to me it's like a bludgeon really the choice is between This approach we use just equities Bond doesn't

even enter the picture or the third approach and I'll tell you one of the reasons I have trouble with this approach when I use I use it every year to actually I use the Goldman approach to see what the numbers would look like it looks like Pakistan should have a lower Equity risk premium than the US you know why because the standard deviation in the Pakistani Equity Market is actually lower than the standard Deviation in the US why might that be sopia because there's no liquidity remember for prices to change people have to trade if

you're in a market where there's no liquidity the standard deviation will be close to zero if I use this approach any Market where nobody trades that's a safe Market it's the exact opposite but the problem with standard deviation Equity it's a joint effect of the risk of the country And how liquid it is so I've tried this and I get some really strange looking numbers Costa Rica should have a very low risk premium because nobody I guess trades in cost I guess they're all in the beach or in the rainforest I don't know what they're

doing but they're definitely not trading so when you look across these approaches and you think about what to do you're good jumping around know you can see that the different the approach You will see built into your spreadsheets is this one where I take the default spread because that's my base approach but if you push back and say I don't like the way you're scaling up I'll let you use the bond default spread the different numbers are not different enough for me to take a stand but essentially I'm adjusting your Equity risk premium for what

I think is your country risk so at the start of every Year I estimate Equity risk premiums by country I start with an equity risk PR for the US and I haven't done this yet but I have but I have a forward looking premium at the start of 2025 that premium was 4.33% let me pause right there so that's my equity for the us and this may sound us Centric but I'm going to stick with it I'm going to assume that that's the equity risk Fram for any mature Equity market so ask me the question

how do you know whether Equity Market is mature right a cheat I go to the ratings agencies and if they give you a AAA rating I say you're a mature Equity Market I know I'm Outsourcing this but do you really want to go around asking countries are you mature are you not I mean I'd get into a whole lot of trouble calling you immature this way I can blame Moody so you know what mark Market have AAA ratings name some countries which have AAA Ratings let's start close Canada I know we're right now preparing for

war and I'm going to show what the war will look like Canada AAA rating in Europe it's Germany Netherlands it's all northern Europe southern Europe don't even look it's ter terrifying when you go below that line in Asia there is only one country with a AAA rating Singapore Singapore the only AAA R Australia New Zealand AAA rating all of those countries are going to get 4.33% if you're not triaa rated then the game is on right I take your rating I come up with the default spread initially I used to try to find a Government

Bond in that country and and I finally gave up because only like 15 or governments which have government bonds so so I started using a scalar by looking at an index of emerging market equities that S&P has and an index of Emerging Market government bonds which has an ETF I think that I think JP Morgan maintains and I take the ratio at the start of 2025 that number was 1.35 you saying how do I use that let's say your default spread is 2% based on your rating 2% * 1.35 is 2.7% you add that to

4.33% I've got an equity risk P for your country sounds abstract so let's look at the numbers this is what the world look like to me at the start of 2025 pick your part of the world wherever you're from you can pick that part of the world if you from North America look elsewhere because there's not much going on in North America you got Mexico you got us even Mexico I pushed out of North America you know how much crap I get with this from people saying you put me in the wrong geography or the

your borders the worst is when people say you drew the borders wrong know I get a disproportional large Number of Indians saying you got the Kashmir border wrong look I'm not the UN I'm trying not trying to Arbiter what the borders are so draw whatever borders you want this is the most downloaded data set on my web page by far it gets used in the strangest places I remember getting an email from the New Zealand milk board I didn't even know know there was a New Zealand milk bort I got this email they said we're

using your Equity risk Premiums to set milk prices for New Zealand farmers who are they selling the milk to Zimbabwe hey but that at least they said where are you getting your Equity risk premiums and I sent them I said this is not rocket science this is what I do I start with the US premium and look up the rating so basically the class played out in a 15minute YouTube video but sometimes you get emails and not sure how to respond to Them right I'll give you one of my favorite examples I know some I

get an email from a business person in Lebanon about 12 years ago and here's how the email begins you've destroyed Lebanon I said what after 20 years of Civil War in hisbah I am the guy who did this you know what did I do and it turned out that he was a Lebanese business person was trying to sell his business and in apprais r value the business use my Equity risk premiums and you take a look At Lebanon not exactly the safest part of the world right you put in a risk it was actually not

as bad into but it was like 20% Equity risk pre what happens if you put a 20% Equity risk premium discount rate it gets really high your discount rate gets really high your value gets really low this guy felt he'd been chipped it was all my fault initially I was going to say take it up with your appraiser but I decided discretion was a better part part of Val Here I said it's not my fault see whose fault it is what drives that extra risk premium your rating your rating is the toilet you're going down

with it I said it's not my fault it's Moody's fault if you want to take it on somebody I'll send you their address it's 70 Church Street New York New York he there's no rock this is there's no intellectual Firepower band this right but it's completely transparent I'm not saying I like this country I'll give it A lower risk premium it's entire he's saying what is this box at the top this take a look at the countries in that box you got Syria you got North Korea you got Sudan these are called Frontier markets Russia

is up there now it didn't used to be Russia's made it in there you know what these countries share in common what did I need to get a country risk premium I needed a rating these are countries where there is no rating Russian the Russian Sovereign ra ings was suspended in 2022 they haven't come back it it makes my life a lot more difficult because we're not talking about a small country somewhere right we're talking about a you know and for a long time if you didn't have a rating they didn't show up on my

in my data set until I get another email I get a lot of emails from a Syrian business person must be the last business person left in Syria and he says look I'm a Syrian business person I'm trying to come up with a cost of capital for my company I'm looking for an equity risk premium for Syria I was on your website looking for it I couldn't find it why it's a very aggressive why and I said you know what you don't have a rating I can't come up with an equity risk premium and then

he comes back know five minutes later he says so what am I supposed to Do and I said you have a point you have to run a business though I'm wondering why coming up with a cost to cap for your business is high up on your priority list if you're in Syria and I'll be looking for a lot of other things but you clearly have some degree maybe you have a competitive advantage in your last name is Assad I didn't check and I said you know what I'm going to try to give you an equity

risk brain so here's what I do for countries that Don't have a rating there's a service in Europe called political Risk Service that attaches country risk scores to countries that's all they do is they measure they look at political risk economic risk so the way the risk score works there and among others The Economist does that the World Bank does it I've used PRS for a while so I'm going to stick with them a lower score is a riskier country a higher score is a safer Country so last in 2025 when you look at those

PRS scores the high the safest country in the world I think was Switzerland or Sweden or what you know it's said and then of course you get down and you get the mix and they do the frontier countries so they do Russia they do North Korea so let's take take as an example um Myanmar doesn't have a rating but has a country risk score of 56 remember I'm not a purist I'm a pragmatist guess how I came up with an equity risk cream for Myanmar I look for other countries which have scores between 55 and

60 that have ratings and an equity risk premium I found four then what do you think I did I average the four he think that is so simplistic guiltiest charge if you can come up with a creative way of estimating an equity risk PR for North Korea I would love to Hear it I haven't figured it out yet but my table my table is full you no matter where you operate in the world I have a number for you okay it's an input that I need you're saying how many companies are you going to value

that are in Myanmar I don't have to have a company in Myanmar to worry about Myanmar Equity risk frams right if you're a lumber company and you're getting your mahogany from Myanmar hey guess what you're exposed to Country risk there so as you look at these companies your countries you're going to see difference in Risk so now let's seal the deal we've got a way of getting an equity we I still haven't finished that that implied pre for the US I'll come back to it but let's talk about these Equity risk PRS and how they

play out in your company's valuation the first approach is the default Approach you see at many investment Banks is you tell me where you're Incorporated I will use the equity risk premium of the country in which you're Incorporated I can't even imagine how you defend this approach but it is the default approach so what happens if you're an Indian company you get the Indian Equity risk you're a Russian company you get the Russian Equity risk premium if you're a South African company you get the South African Equity Risk you're saying what's wrong with that could

you be a South African company know could be a diamond company the beers where do you get your revenues you don't get them in South Africa you get them in Europe you get in North America your operations could be all over and I'm giving you the equity risk for of the country in which you're Incorporated so I'm going to give you a second approach the second approach what You do is you start with the risk free rate you come up with the beta but you bring in that country risk premium of the countries in which

you operate into the process so basically if you're a high beta company you're more more exposed to Country RIS in a low beta company which I think is not an unreasonable but you're asking beta to carry one more weight to all of the other weights it's caring bet is supposed to measure exposure to interest Rate risk and macroeconomic I'm saying measure country risk as well and the third approach I'm actually going to try to isolate country risk and try to identify whether you're particularly exposed now talk about some of the things you might look at

that might make your company particularly exposed to Country risk so let's start with the country of incorporation versus where you operate this is the status quo approach where Everything is based on where you're Incorporated so if you're Incorporated in a risky country you're going to end up with a high cost of equity no matter where you do business you see what what kind of effects this is going to have if you're a South African company about 20 years ago a lot of South African companies start it's a gold mining company actually that I was talking

to moved their incorporation from South Africa to London can you do that yeah move your country over and I asked the CFO what why do you do this and he said we make us less risky I said what exactly do you do take your mines that are in South Africa move them to Yorkshire Lancashire or moving your headquarters from you know Johannesburg to London doesn't make the risk go away but that's a kind of trap you fall into and you think about where you incorporate that drives all of the Risk so I'm going to stay

with countries of operation and within the countries of operation I now have to come up with the way of estimating the equity risk premium for your company so if you have a company it's operating all over the world what's a one metric you can generally find in that company's financials that's broken down by geography revenu is often the only one so Beggars can't be Choosers use Revenue weights could that get you into trouble absolutely right there are times you worry about where are my factories where are I so the first is to take a revenue

weighted approach of where you operate bring that into your Equity risk pre the second is you might say I don't care about revenues it's where I operate that I worry about risk I'll tell you the kinds of companies where I don't look at revenues I look at where you Operate and that becomes but in each of the these case what are you doing you're taking the countries where you either sell or make and use them to come up with a weighted average so you can be a company in a safe country that's incredibly risky you

can be a company in a risky country that is incredibly safe infosis is an Indian company but it gets 93% of its revenues in the US and Western Europe conversely Coca-Cola is a US Company that get 60% of its revenues from some of the riskiest parts of the world so what we're trying to do is break out of the box of where you Incorporated using the risk thinking about what are the country and now you see why I need the entire world to Value even if my job is just valuing us companies where does Microsoft

get much of its software written probably in India even if they sold nothing in India how can I just Ignore that risk when I value Microsoft welcome to globalization this is the dark side right because effectively 30 years ago you could said I'm going to be working in the US I don't care about the rest of the world that's not going to be the case anymore because your companies are exposed so I'll give you a couple examples of Revenue weighted Equity risk frames embri you familiar with what embri does You can tell what what does

embri do jets and also corate if you take a short Hall flight in the US one of those small Jets most of the time you''ll be flying an embri jet it's a very good aircraft maker it's a Brazilian company it's Incorporated there but it gets it at least the time that it is they got 97% of their revenues outside Brazil mostly in North America selling to Airlines North America and Western Europe so in a revenue based approach the equity risk premium I'm going to get it's going to look very much like the US pre I

know there's a flaw here because embra still makes it jets in Brazil I'm ignoring the production but they don't even tell you where their factories are I'm going with revenues take a look at mbeb what does mbeb do sells beer it's part of Mev now hu it's a huge the largest Brewer in the world but Mev is the Brazilian version Of the Brewer and in this is in 2011 their revenues came from all over Latin America they're a Brazilian company but their risk comes from where they sell not from where they operate most cases I

use Revenue weights so when you value a company if it's a consumer product company if it's a you know just use Revenue ways I know that it there there but the rest of the information you don't have I'll tell you one exception if you're Ving an oil Company don't use Revenue weights why because what do you sell into a global oil market so if you're an oil company what keeps you awake at night where your oil comes from your oil comes from Nigeria guess what you know you got to worry about Nigerian country risk so

if you have a company where that's the case you might bring in where the oil comes from make those your weights So last example I I talked about Coca-Cola and how it gets revenues all over the world there's the equity risint for Coca-Cola you're saying why is it broken down by region not by country practically you know why Coca-Cola doesn't break things down by country that table would run 72 lines right many companies will break things down by region if you go back to that picture I showed You notice there a regional Equity risk premium

you know what that Regional premium is computed as a weighted average of the equity risk the country is invaded by GDP so I'm doing the Asia Equity risk premum China and India IND will be weighted a lot more than Vietnam in that premium the reason I compute them is there are companies like Coca-Cola which don't break their revenues down by country they break it down by Region and as you can see it's you know it's sometimes rad when you look at this data for your company be ready for some frustration Lisa you had a question

it'll still break it down they'll do revenues by region so if you're Accenture for instance which provides Services they have a geographical breakdown at their clients and where they get their revenues so it's not service versus Product it's more a question of you know do they do the breakdown that makes you risk less right so in a sense it that's more for production than for revenues it's not easily transferable revenues but maybe that's why the reason I don't care as much about where I infosis his factories because if India Goes to Hell in a hand

basket put 3,000 software engineers in your fly them to some island in the middle of the Indian Ocean you got your Production still back online right so that's a good question to think about and we'll talk about in the context of Lambda one final point when you look these so this is why I want you to pick a company because if you look at the footnotes for your company they will have this geographical breakdown and some companies it's incredibly frustrating in terms of how they break it down us companies are among the worst you know

the typical breakdown of Revenues for us company we get 72% of our revenues from the US and 28% from the rest of the world come on guys the rest of the world is a really big place is it Europe or is it Venezuela it makes a big difference or european companies have their own vision of hell when it comes to this right European companies will tell you we get our you know 35% of our revenues from the UK 45% from from EMA you know what EMA stands for Europe Middle East and Africa you bundle those

three this is I have no idea what you're talking about here I remember and I'll leave you with this you know so as you look at your companies and you look at the breakdown be prepared for the data not being complete work with what you have if you picked a company try doing this for your company you saw that PA's got the updated Equity risk frame see if you can get a weighted average ni Love hey how are you

![Upbeat Lofi - Deep Focus & Energy for Work [R&B, Neo Soul, Lofi Hiphop]](https://img.youtube.com/vi/THh4fT0O7IY/maxresdefault.jpg)