[Music] What's up, everyone? Welcome back to Mike and his whiteboard. My name is Mike, this is my whiteboard, and today we're going to talk about some adjustments for short put strategies.

So, yesterday we talked about some adjustments for covered calls, and today we're going to talk about short puts. We can get into a few other strategies in the future, so definitely send me some feedback if you like this sort of analysis. But when we're talking about short puts, we're really talking about getting long on an underlying.

So, if we think an underlying is going to go up or if we're bullish on the underlying, getting into it via a short put might be a better solution than just buying the stock outright. That's because we have a higher probability trade, and we have theta decay on our side. But what happens when the trade doesn't go our way, or when something in the market happens that changes the price of our option or gives us maybe another opportunity to get even more long?

So, we'll take a look at some of these scenarios today, and we'll start it off with the first one on the next slide here. When we're looking at the opening trade of a short put, I'd like to just review this so we get the math bearings down. So, we're taking a look at the stock price being at 70.

We've got an option expiration of 40 days, and we're looking at selling a pretty far out-of-the-money put, 10 points down, for one dollar, or one hundred dollars once it's at expiration. So, we're looking at a max profit of one hundred dollars, because again, when we're selling options that are out of the money, if they expire out of the money and we don't manage that trade any time during the life cycle of the trade, we're looking at a full max profit of whatever the credit is that we received. So, we're basically selling this option for 100, and therefore, if it expires out of the money—anywhere above this range—if the stock price goes to 60.

01, it doesn't matter at expiration; that's still going to be out of the money. So, we would get that max profit of 100. For that reason, our max loss would be five thousand nine hundred dollars, as opposed to the six thousand dollars you might assume.

While a short put does give us the right to buy 100 shares at our strike price of 60, we sold the option for one dollar, so we can use that credit, that cash credit we received, to offset our max loss by 100, which you can clearly see here. And because this is the opening trade, as we discussed yesterday, our max loss is going to be equivalent to our break-even point in this situation. So, we're going to break even if the stock price is at 59 at expiration, and that's because the short put would have intrinsic value, or real value, at expiration of one point, or one hundred dollars.

Because if I have the right to buy shares at 60 and the stock price is at 59, if I exercise that right, I'm going to be at a loss of 100. But since I collected 100 from the get-go, I'm going to break even on that trade. I would see a loss of 100 because I'm buying shares at 60, even though they're trading at 59.

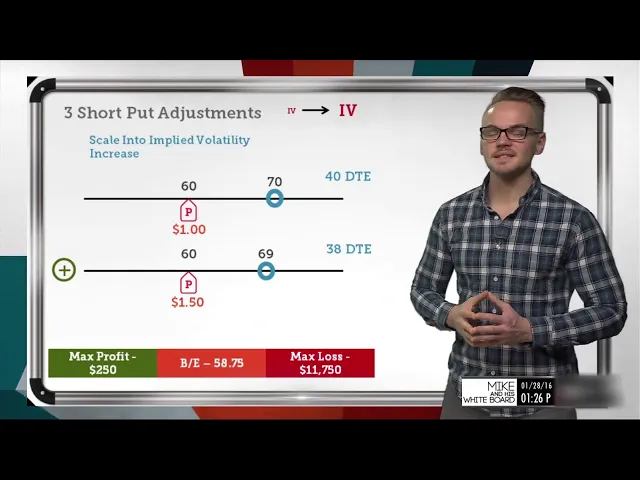

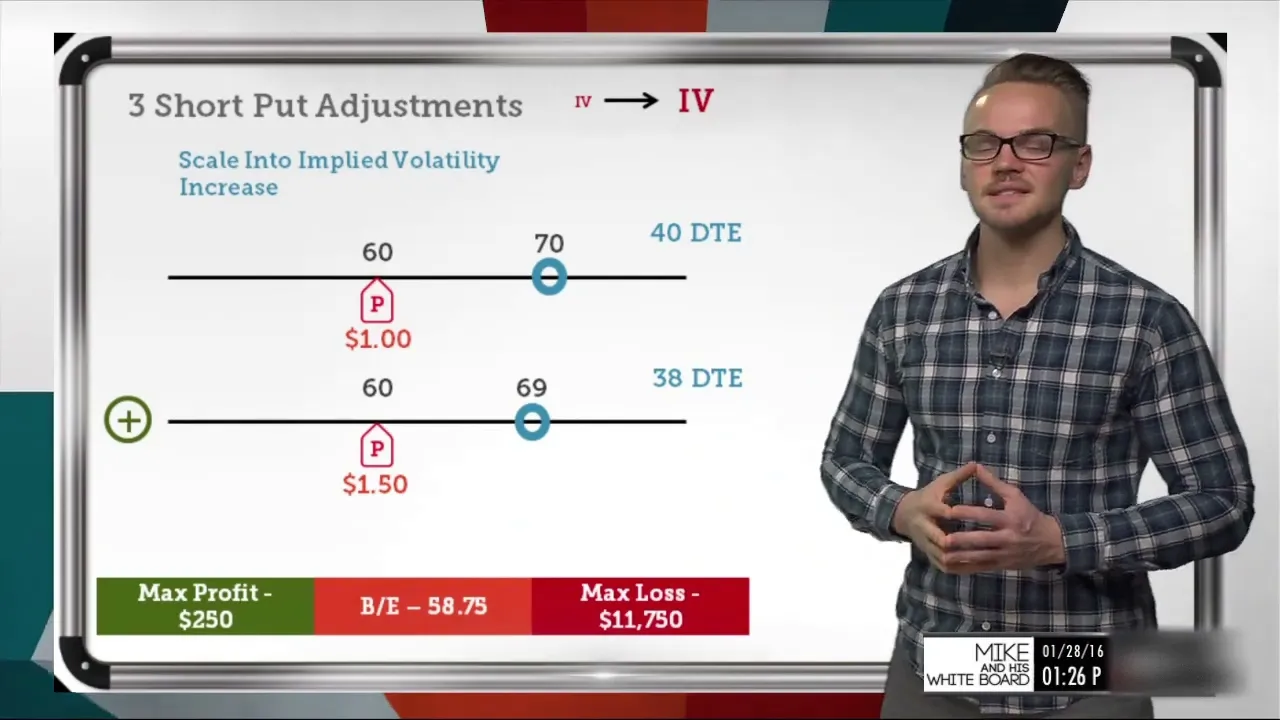

But I collected 100 to offset that loss, so my P&L on the position would be zero, and that's where we're getting our breakeven from. So, let's take a look at the next slide, and we'll look at a variation of this and what happens to the implied volatility of a certain trade like this. So, let's give an example of our opening trade being at an implied volatility of, let's say, 20 percent.

So, it's pretty low, but it's a fair implied volatility for an underlying trading for this value. So, let's say the implied volatility was at twenty percent, and two days later, we saw implied volatility increase. So, let's say that with 38 days to go, two days later, implied volatility went to 30.

So, we see the stock price has adjusted just a little bit, but the implied volatility increase has increased the value of the put by 50. So now, we're looking at a put that we sold for one dollar, and it's trading for a dollar fifty right now. So, there are a few things that might go through our heads.

So, let's just consider our opening trade. If we had sold the put for one dollar, and we're now seeing it trading for a dollar fifty, we would see ourselves at a 50 loss. And that's because if we sold an option to close that position, we have to buy it back.

So, if I sold it for a dollar and I need to buy it back for a dollar fifty to close the position or give myself a flat position in that underlying, I'm going to see a 50 loss. However, we might see that as an opportunity to get even more long. Tom always talks about tranches on the show, and what he really means by that is basically a handful of contracts.

So, if I've got a handful of contracts or my tranche size is one contract, but I'm allowing myself to get up to two contracts, maybe I would think about trading small from the get-go and just selling one contract. That gives me one more contract in terms of my position sizing to allow myself to scale into opportunity. So, that's exactly what this would be here.

We've shown that implied volatility has a mean-reverting property, which means that if it spikes up over time, we've seen that. It does come back down, and if it goes down to a very low level, we've seen over time that it should come back up. So, if we believe that IV is mean reverting and we thought that selling premium here was a good value, if we see implied volatility increase to 30 percent and that increases the value of my put by 50, then if I scale into that, let's just take a look at what my implied volatility would be.

My mean level of implied volatility for my opening trade would be 20, but if I scaled into another contract, given the size of my portfolio, and I'm okay with that, if I sold a put here at 20 implied volatility and now I can sell another put for a higher value at 30 implied volatility, I take the average of that, and my mean implied volatility level for this trade would now be 25 percent, as opposed to 20 for my original trade. So basically, it's putting my implied volatility level for this trade at a higher level, which is going to be better for me if I believe that implied volatility is going to come back down over time. What this also does is it increases my max profit to 250 dollars, as you can see in the bottom left.

So I would be collecting one dollar in my original position. I would be scaling into another contract for a dollar fifty, which would increase my max profit to 250 dollars because, again, my max profit is if these options expire out of the money, and I would keep both of these credits here. My max loss, though, is now eleven thousand seven hundred and fifty dollars, and that's because I now have the theoretical equivalent of 200 shares of stock, as opposed to just 100 shares of stock.

I'm basically doubling into this position or doubling the contract size. So it's important to note that if the stock price did go to zero, I would be liable for that max loss of eleven thousand seven hundred and fifty dollars. But normally, with a sixty-dollar or seventy-dollar stock, we wouldn't let that happen; we would probably close out prior to that.

So what's interesting is my break-even point. You might think that to calculate the break-even point, we would just add these two credits together and just slide that down based on our contract size. But since I'm now long or short two options here — so I've got two short puts on the 60 strike — a one-point move down past that level is going to double my rate of loss, as if I were to compare it to this value.

So really, what we're doing to calculate our break-even is we're taking this credit of two dollars and fifty cents total and we're dividing that by two because I know that with a one-point down move, I'm now going to lose a value of two points, as opposed to one point with just one contract. So I take my 250 credit, divide that by 2 to get 1. 25, and that's how I subtract that from the 60 strike that I'm short here to get my break-even of 58.

75. So this is one way we can scale into opportunity if a short put gives us an opportunity in terms of implied volatility increasing to increase our max profit, lower our break-even just a little bit, and give us a better implied volatility mean. So now let's look at the next slide and we'll look at what would happen if the trade went against us.

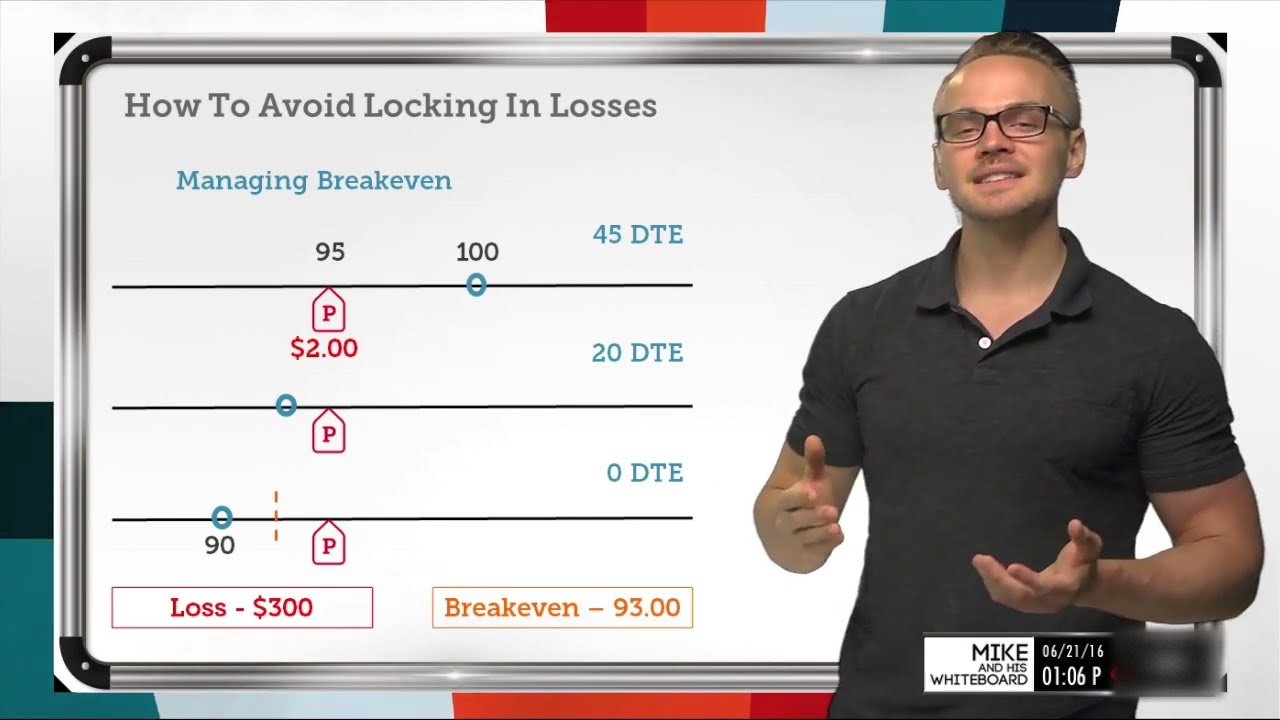

So let's say we look to just adjust the strike out in time. We're not looking at adjusting the strike in terms of up or down on the strike scale; we're looking at just moving it out in time. So let's say we had the stock at 70, our short put at 60 we sold for one dollar, and with three days left in our trade cycle, the stock price is now at 57.

We were holding on because we thought that it might expire out of the money, but now we can clearly see that we don't believe that it'll come back up above 60, so we'll look to roll out our strike in time. What's really important here is to just look at the math behind closing our current position and opening up the new one. So if I close my position for three dollars and five cents, which makes sense because if I sold it at 60, the stock price is at 57, it's got to at least be trading for three dollars.

And with only three days to go, I've got five cents of extrinsic value here, so that's a pretty fair amount. I've collected the majority of my extrinsic value in this position, but I want to roll it out in time because my assumption is still the same. So I'm able to roll it out for 3.

75. So basically, I'm collecting 75 cents of extrinsic value since there's three points, or three dollars of intrinsic value, embedded in that new short put for 35 days to go. So we look at all these values and we can see that I'm collecting a new net credit of 70 cents in addition to the one dollar credit I collected originally, which gives me a new max profit of 1.

70 there. But it makes me realize a loss of 205 because I sold my put for a dollar but I'm closing it out for 305. So the net value of that is a loss—a realized loss of 205.

But if my new position expires out of the money, or if the stock price goes above my short put, I would have a new max profit of 1. 70, and I’ve improved my break-even just a little bit from 59 in my. .

. Original position to 58. 30 in my new position, so you can see that just rolling the strike out in time can reduce our breakeven even further.

So let's go to the next slide, and we'll look at adjusting the strike out in time as well as rolling it down. Some people don't like to deal with that in the money put position, and that's totally fair. So what's really important to keep in mind is just making sure that whatever we're closing for a debit, if we're going to roll the put down to keep it out of the money, we need to extend our duration here to make sure that we're collecting more than we're paying in the debit.

So in this scenario, we're basically rolling it down to the 55 put, but we're extending our days to expiration pretty far out to 60. But since it gives us a 20 net credit, as you can see here, I still reduce my breakeven 20 cents. I'm increasing my new max profit to 1.

20 if my new short put expires out of the money, and I'm still realizing that loss of 2. 05 because at the end of the day I sold this for a dollar up here, closing it out for 3. 05 in the same expiration, and that gives me a 2.

05 net loss. So let's roll all this information together with some takeaways here. The very first takeaway is that trading small allows us to scale into opportunities.

As you saw with the implied volatility example, one person might see it as a hindrance, or they might see a loss in that portfolio position, but if someone was trading very small at the beginning and they're able to scale into opportunities, that person might see it as a new opportunity. So it's important to keep that in mind. Also, rolling a put out while keeping the same strike includes intrinsic value, so that's why it's so easy to collect a credit when we're looking to roll that same in-the-money strike.

Because the more time we're adding to the position, the more extrinsic value we'll keep while we're still including that intrinsic value of the option. Lastly here, rolling a put down and out increases extrinsic value and pop, so if we're going to roll it down to keep our put out of the money, we're probably going to have to extend our duration even further than we would if we kept the same strike, to make sure that we're selling our credit for more than the debit we're paying. Lastly, I kept this on the same takeaway as yesterday's.

When maneuvering, keep in mind pop and breakeven price, as those are going to be the two most important things when we're looking to roll defensively with strategies. So thanks so much for tuning in. My name is Mike.

If you've got any feedback or questions, shoot me an email at support@doe. com or you can shoot me a tweet at @doetradermike. Shadow traders are up next, though, so stay tuned!

Hey everyone, thanks for watching our video. If you liked this video, give it a thumbs up or share it with a friend. Click below to watch more videos, subscribe to our channel, or go to our website.