[Music] hey everyone and welcome back to Mike and his whiteboard my name is Mike this is my whiteboard and today we're going to talk about assignment risk so when we talk about expiration which we did yesterday if you missed that show check out fine shows at the top of scroll down to Mike and his whiteboard and you'll find it there it'll be the last one there we're going to talk about another aspect of expiration and that's going to be assignment so when we get closer to expiration generally our assignment risk grows but there's some things

to know about assignment in general so let's get right into it and we'll break it down for you so when we're talking about assignment or option assignment we're basically talking about when options are exercised prior to expiration so one thing to note is that there's a difference between buying an option and selling an option and who has control over assignment so if I'm long an option that means that I have control over assignment because I can exercise that option as long as I'm dealing with a US Equity option and not an index like we talked

about SPX and VI the other day where we those are European options so we can't exercise those early but if we're looking at a US Equity I if I'm long an option I have control and I can early exercise if I need to or want to however if I'm short an option the option owner has control so if I'm short a put or short a call or if I have a defined risk spread like an iron Condor or just a short vertical spread I have a risk in terms of assignment on that short option even

though I still have that long option that I can exercise which it gives me that defined risk aspect but it's important to note that when I'm long in option I have control because I can exercise it and if I'm short in option the owner of that option or the person that's long that option has control over assignment so basically our assignment risk when it comes to options really only comes down to short options because that's when we are not in control so if we go to the next slide here we'll break it down a little

bit further and when we're talking about buying power it's going to be different when it comes to assignment but it really doesn't change the risk profile of the trade so this is a really important topic and concept to grasp so we're going to be talking about selling a naked put and essentially when we sell a naked put our risk profile is 100 shares of stock at our break even price so let's say I sell a put and I've got a buying power reduction of $300 so let's say a stock is trading at $50 and I

sell a naked put at 45 or 440 if I've got a buying power reduction of $300 to sell that option it's most likely because I in a Marin Mar account and it gives me additional leverage when I'm selling options so my risk profile is still the same so I receive a credit when I sell that option so I've got 100 shares at my strike price but I have that credit off setting that Max loss so that's why I include the break even here so I've got 100 shares at my break even price as my risk

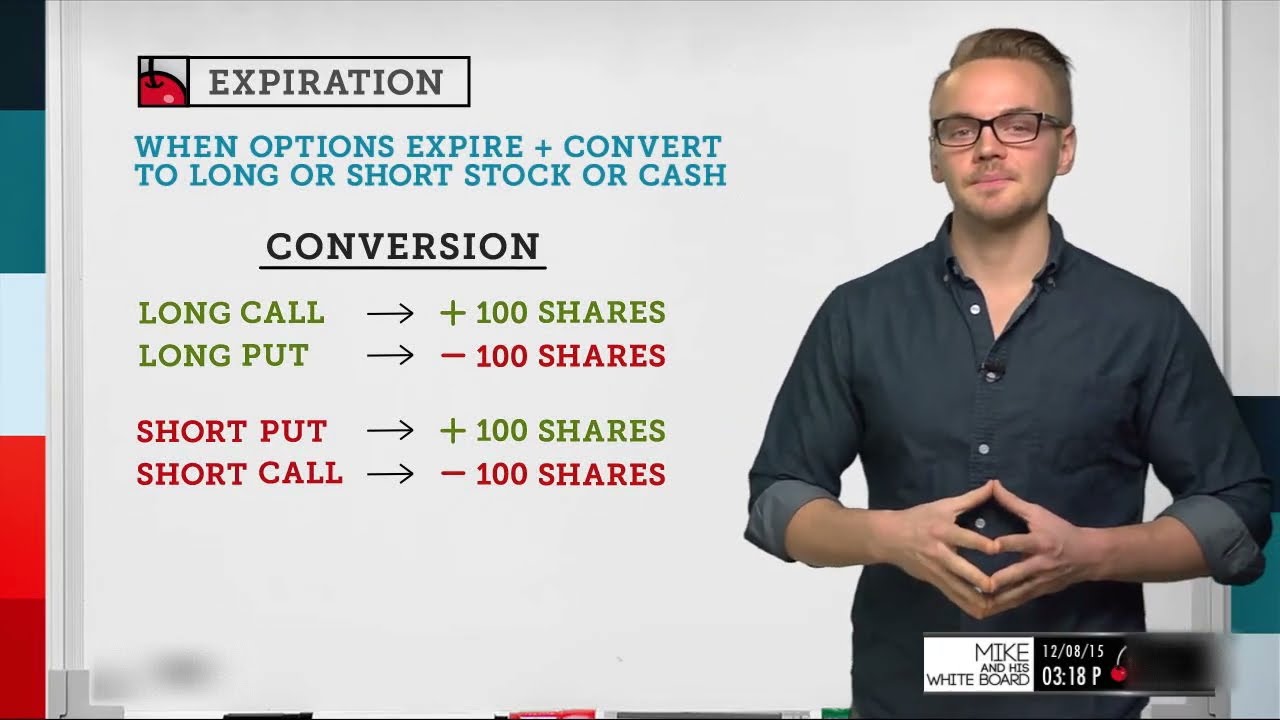

profile now let's say that put goes in the money so let's say the stock price dips below my strike price which would be bring that put in the money and now I would be long 100 shares of stock because if we just review what a put contract is it's the right to sell 100 shares of stock so if I sell that right for someone else to sell their shares to me if they exercise that option and I'm early exercised I would then become long stock because they would sell their shares to me so now if

we take a look at the risk profile my risk profile doesn't change because at expiration that short put becomes long stock regardless of it's in the money so my risk profile is still 100 shares at my break even price however now that I'm long shares I don't have that additional leverage when it comes to that option itself so let's say my buying power reduction increases so for this example we'll say that incre it's going to increase to $2,500 which is pretty equivalent to what we were talking about with that example because normally in a margin

account you get close to 2 to one on stock so that sounds about right so the big takeaway here is our risk profile doesn't really change as long as we're dealing with naked options like this however our buying power reduction will so that's the big takeaway because if I'm trading options in a margin account and that's giving me tons of Leverage so I've got $300 of buying power reduction here which is really just the cost associated with the trade entry and then I'm assigned and I am now long 100 shares and you can see my

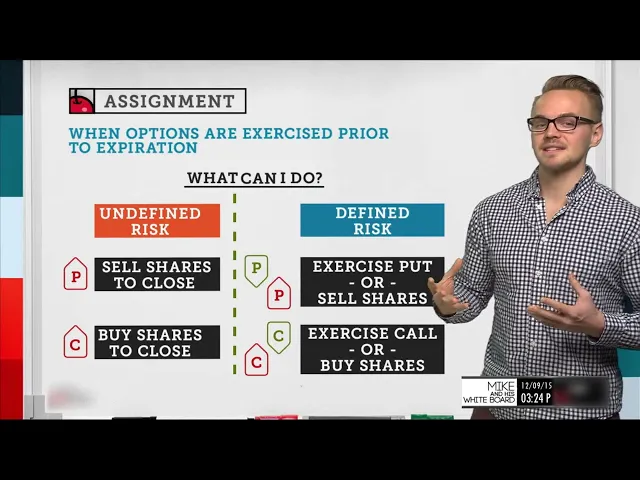

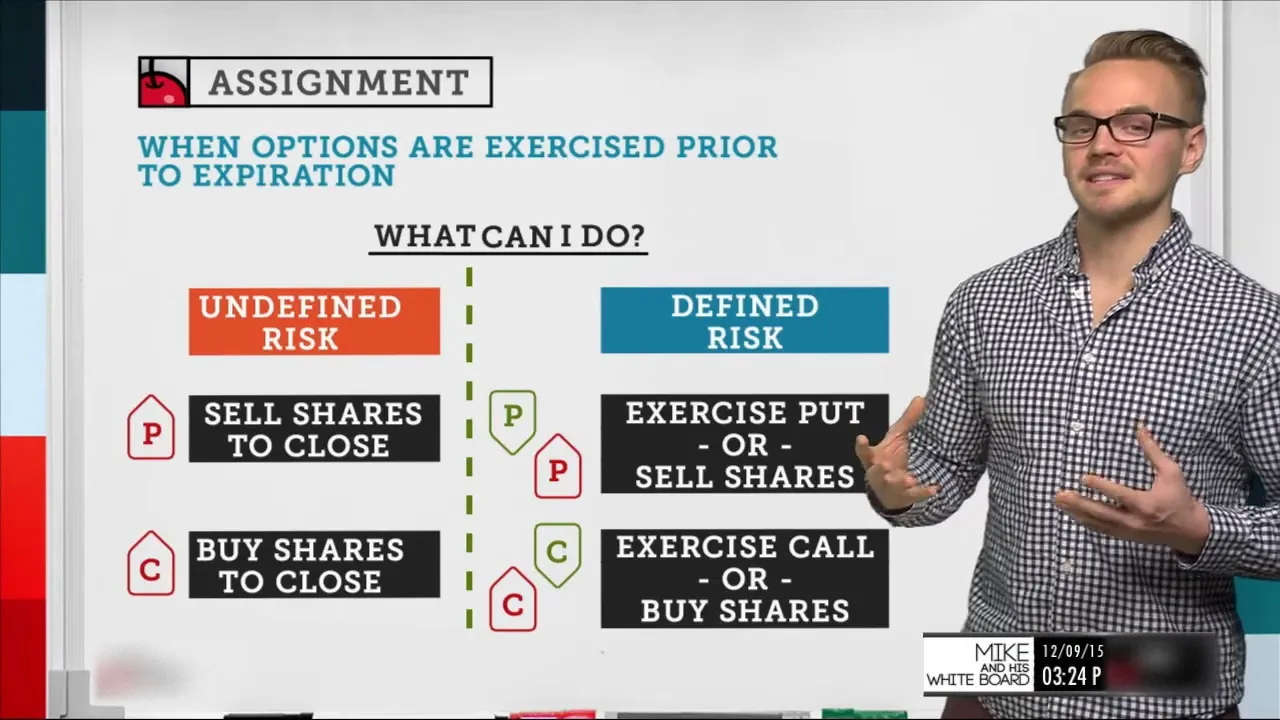

buying power reduction increases almost 10 times that amount so it's really important to keep in mind and just be aware of certain situations where we might get assigned so that we definitely have the cash value available and if not we have the means to close that trade out right away so let's go along to the next slide and we'll break this down even further so when what there's one thing we can ask ourselves and that's what can I do so if I'm assigned what can I do so we're going to walk through a few examples

here so if we've got an undefined risk trade and let's stick with that same example so let's say I sold a put so I sold a put and it went in the money and for whatever reason the option owner decided to exercise their right to sell their shares which means that I would have to buy that those shares from them so basically I'm long shares now so what can I do if that happens well I can basically shell sell my shares to close so if I'm long those shares I can just sell them to close

the position now it's going to depend on whether I have enough Capital to hold that position or not to determine whether the brokerage will get involved if I don't have enough cash and my net lick becomes negative because I'm long those shares then I'm going to be in a margin call and they're going to give me a call to let me know hey you've been assigned and now you're long these shares so you're going to have to close this position or add additional Capital to bring your net lick above zero so I can sell the

shares to close the position if that's the case or if I sold a call which is the right to buy 100 shares at a certain strike price so if I sold that right to someone else and they decide to buy the shares then that means I have to essentially sell the shares to them so I would be negative 100 shares I would have short stock in that position so if I had short stock in that position what I could do to close that position and be flat is simply buy the shares back to close so

if we look at some defined R examples let's say we've got a short put spread so let's say I've got a short put spread here and and the whole put spread goes in the money so the short putut would be exercised if they decided to exercise that early so I would be assigned those long 100 shares of stock so again what I could do is sell the shares or if my long put is in the money I could exercise that put and that's where that defined risk aspect comes into play so if the entire put

spread is in the money it makes more sense normally for me to exercise that put rather than sell the shares in the market to close it on the flip side if I've got a short call spread so I sold a call closer to the money and bought a call further out of the money I could do the same thing as undefined risk so I could buy the shares to close or if my entire call spread is in the money again I could exercise that call and it would give me that defined risk so I keep

talking about defined risk on the next slide we're going to break it down and show you more visually how we can get out of that trade so when we're talking about defined risk there's one thing to consider that's very important and this is something I didn't consider when I was new to trading so this is something that I want to hit home for everyone so let's say we're going back to that short put spread so I sold a put at 95 and I bought a put at 85 so let's say when I did that the

stock price was at 100 so let's say it was right here now if we get close to expiration and the stock price goes to 90 my short putut would be in the money here but my long put would not be so this is an example of where sometimes it can become an undefined risk trade so let's talk through what would happen if the option were to just expire in the money not even talking about assignment so let's say my short putut is in the money but my long put is not if I held this through

expiration my short putut would become 100 shares of stock at 95 but since my long put is out of the money still it would basically disappear and expire worthless so at this point if this were to happen I would be long 100 shares of stock and I would have this be exercised or it would basically expire worthless so it wouldn't really help me in any way so it's really important to understand that if just my short put is in the money it's going to act more like an undefined risk trade going through expiration but if

I'm assigned on that put so I'm assigned at 95 so I've now I've got long 100 shares at 95 5 I don't have to exercise my long put because what I can do if we think back to the previous slides I can sell the shares at the market price so instead of using this put and exercising it to sell my shares at 855 what I can do is just sh sell the shares at 90 in the market for a better price so I wouldn't need to use that put however if the if the stock price

went all the way down to 80 then I can use that 85 put to sell those shares at a better price than the market another thing to consider is dividend risk so this was another whiteboard we covered and really the dividend risk only applies to in the money short call options and really we just need to be aware of the dividend being more than the extrinsic value of that in the money call so for a further breakdown of that check out the Mike and his whiteboard episode for dividend risk and that gives a full breakdown

but basically what we need to know is is the dividend greater than the extrinsic value of our in the money call and is the X dividend date coming up and one last thing is buying power so on one of the first slides we showed that our risk profile wouldn't change in the example of a naked put that we're selling but our buying power reduction would change because there's a difference in buying power between long stock and a short option so it's crucial to understand that and just make sure that we have enough capital in the

account which is why we always leave cash in the account in case these things happen so let's go to the next slide and we will break it off off with some takeaways so option owners have control over exercising options so if I'm short in option then I might be at assignment risk but really it's only going to be if I have an in the- money option there's really never going to be a time where an option owner is going to look to exercise their out-of- the money option because whatever it is if it's a long

call that they have or a long put they can do whatever they need to do at a better price in the market if that option is out of the money so really it's going to come down to being in the money and if we're short options we'll be aware of that and we'll see if we're assigned or not secondly assignment can happen at any time but generally closer to expiration so it really all boils down to the extrinsic value in the option so this is the way I like to think of it as we get

closer to expiration the extrinsic value is going to get lower and lower so when someone as exercises something and if we're assigned with a short option basically it can be a it can be exercised to intrinsic value so basically if they have a long option that still has a lot of extrinsic value there they're going to be giving up that extrinsic value if they choose to exercise that option so normally when we're looking at early assignment it's going to be with deep in the money options or options that are pretty close to expiration that's generally

when I've been assigned and lastly be aware of dividend risk defined risk and buying power effect so with dividend risk we need to be aware of the X dividend date and we just need to make sure that the dividend is not more than the extrinsic value of our in the money call if we have one and also with defined risk if our stock price Is straddling our two options if our short option is just in the money and that goes through expiration it'll basically turn into long stock or short stock we don't have that that

defined risk aspect if our long option is out of the money so it's super important to remember that and lastly buying power effect so we've talked about it again and again but it's really important to understand that while our risk profile may not change our buying power definitely will if we go from a short put to Long stock or a short call to short stock so this has been an overview of assignment hopefully you've enjoyed it my name is Mike if you've got any questions at all you can shoot us an email at support.com support

or you can tweet me at do Trader Mike and we'll be back again tomorrow at 3:15 p.m. central Time so we'll see you then hey there hope you like this video click below to watch more videos subscribe to our Channel and check out tasty tray.com for more great research and [Applause] [Music] content