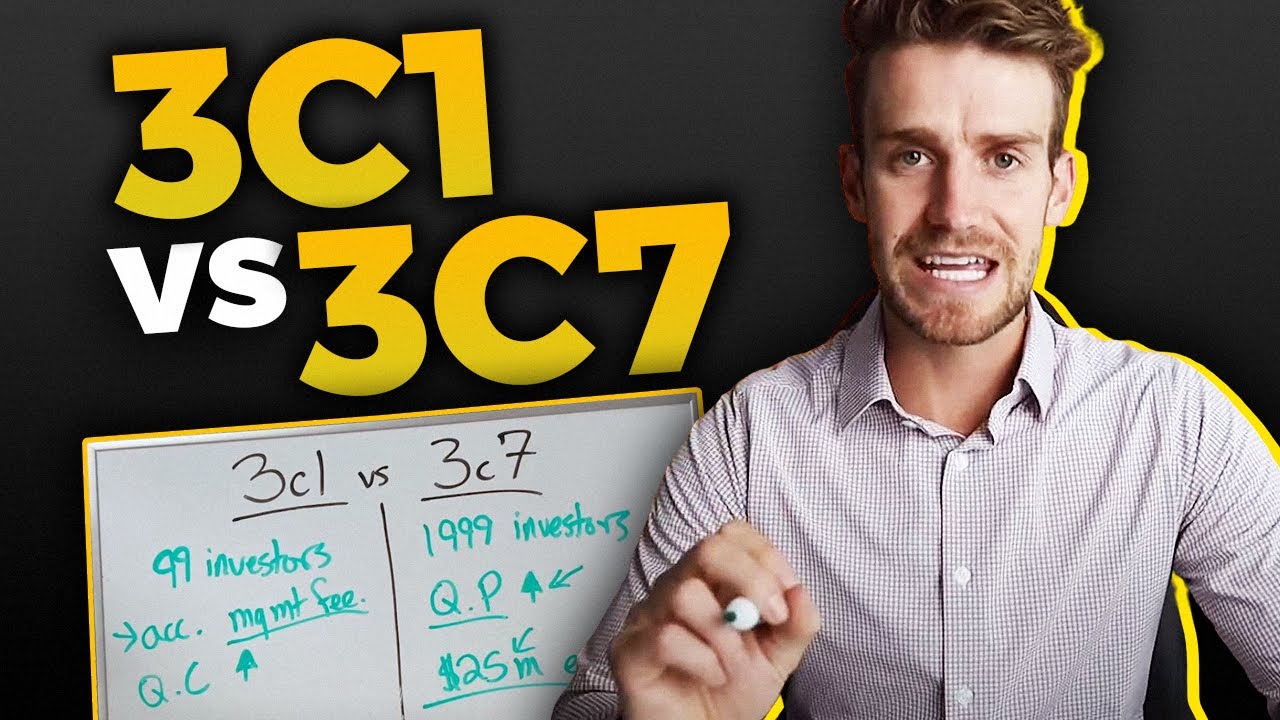

[Music] foreign okay so in the last lesson we started talking about regulatory exemptions we kicked it off with the fund and we talked about the first fund exemption 3c1 now we're going to keep the ball rolling and continue into the second type of fund exemption 3c7 so think of this one kind of like a cousin to 3c1 with one major difference just like 3c1 this exemption is available if the fund a does not publicly offer its Securities same deal as last time and here's where it differs just slightly all investors have to be a thing

called qualified purchasers so what's a qualified purchaser basically think of this like the accredited investor we talked about in the last lesson but with a higher bar this time it's like a super accredited investor qualified purchasers are usually institutional investors like endowments foundations pensions maybe a corporation and generally speaking they're just people or certain entities that hold five million or more in assets or in some cases other types of entities that hold 25 million dollars or more in assets in other words qualified purchaser basically just means a lot of money even more so than a

typical accredited investor at the end of the day when it comes to exemption 3c7 just know this you can't list publicly and your investors must be qualified purchasers now remember how with our cousin 3c1 the fund needed to have fewer than 100 investors well for funds that want to seek exemption 3c7 there's no limit on the number of investors there is a different law that still requires you to register with the SEC if you go over 2 000 investors but that's rare that's another thing we're not going to spend time on that here basically in

the end if you're a first-time fund manager it's typically much more common to just go with Section 3c1 but as with anything in this area talk to your lawyer beforehand Okay so we've talked about the exemption for the fund now let's go back up the ladder and talk about the same thing for the fund manager if you manage a fund you are legally known as an investment advisor and like we talked about before the default for investment advisors is that you have to register with the SEC unless you meet the requirement for certain exemptions for

most small and emerging VCS they typically seek an exemption so they can keep their compliance costs down so if you're a fund manager and you want to seek an exemption there are two main exemptions you need to know about they are one the private fund advisor exemption and two The Venture Capital advisor exemption so let's start with that first one this one's pretty easy private fund managers are exempt from registering if they meet one key criteria which is that you need to manage 150 million dollars or less in assets and that's across all different funds

you manage it doesn't matter if those are VC funds private Equity Funds or some other type of fund there's just a cap on how much Capital you can manage in total simple enough right now let's take a look at the second one if you only advise Venture Capital funds which remember that's the definition we touched on earlier then guess what you automatically qualify under this exemption no matter how many total assets you have under management if only everything was that easy okay back up the ladder let's look at exemptions for the last one which is

the fundraising process itself like we talked about earlier when a private fund takes money from investors in exchange for an ownership stake in that fund often referred to as an LP stake the law considers this a private Securities offering and remember by default Securities offerings must be registered with the SEC unless say it with me there's an exemption if your fundraise qualifies for one of these exemptions there's a fancy term for it your raise is now called a private placement so when you hear people say private placement that's all they mean a fundraise that does

not have to be registered with the SEC now we can talk about exemptions all day thankfully we're not going to when it comes to fundraising the most common one that people tend to seek is this thing called SEC regulation D or if you're one of the cool kids like a lawyer you call it reg d in reality Ray D has a whole bunch of different parts but for you the rising VC fund manager the two most relevant sections you're going to want to know about are Rule 506b and Rule 506c so let's take a look

at the first one 506 B under rule 506b fund managers can raise unlimited capital from investors as long as they don't publicly advertise or solicit Investments for that fund this means you can't be asking for money on Instagram or talking about your active fundraise in a TV interview you need to stick to raising from your own network it also means you can't do anything that Regulators might otherwise see as a solicitation like announcing your fundraise progress on LinkedIn as a way to try to drum up more interests and finally one more thing your LPS also

need to be accredited investors there's a little asterisk on that one like you can technically have up to 35 non-accredited investors but honestly that takes so much extra paperwork and extra headaches most people choose not to go that route okay you're almost done now let's look at that second one rule 506 C let's say it right up top use of this one is a lot less common but it's still worth knowing about under this rule you can do all that stuff like advertise your raise publicly on Snapchat or LinkedIn or whatever and there's also no

cap on how much money you can raise but not only do all your investors have to be accredited but as the fund manager you also have to take a bunch of quote unquote reasonable steps to verify that they're really accredited you can technically raise my in Instagram but every person that gives you money now you have to go do the work of proving to the SEC that they are accredited investors that means you're reviewing bank statements from them getting verification letters from their lawyers any number of awkward interactions you've just set yourself up for at

the end of the day it's just not super common okay last little thing everything we just covered is basically the landscape for VC regulation on a federal level but it's important to remember states often have additional requirements for all this stuff these state laws are what are often called Blue Sky laws we're not going to get into state by state stuff but one thing to look out for even when you have complied with Federal exemptions many states also require you to file a notice within two weeks of selling any security to a resident of that

state so if you're starting to fund do your research consult with your lawyers they'll help you make sure your meeting every requirement you need to and they'll be the ones to prepare any filings you need for individual states all right you did it and so did I you made it all the way through your first video course on creating a VC fund card has got loads of other resources on our website to help you get started our team's always happy to connect with you we'll provide you with guidance we can also introduce you to great

service providers like fund formation attorneys if we can help you in any way along the road so from all of us here at Carta we wish you all the success in the world as you embark on your VC Journey we can't wait to see what you build