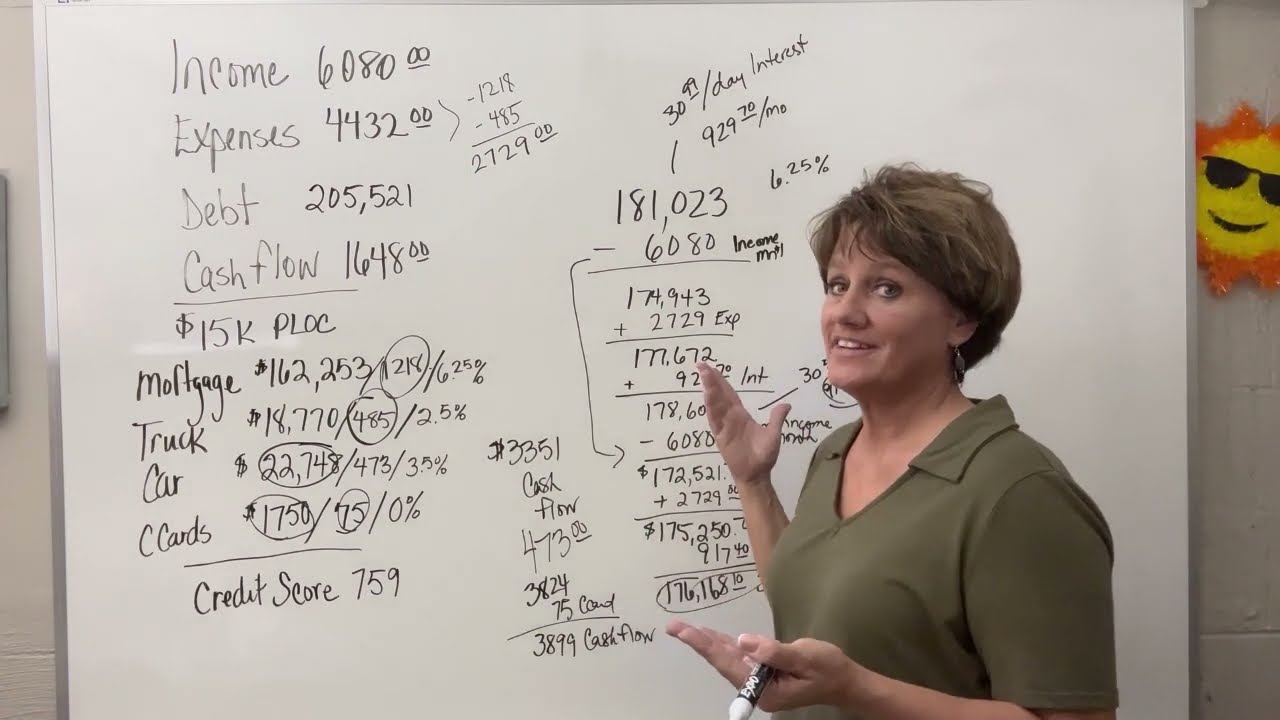

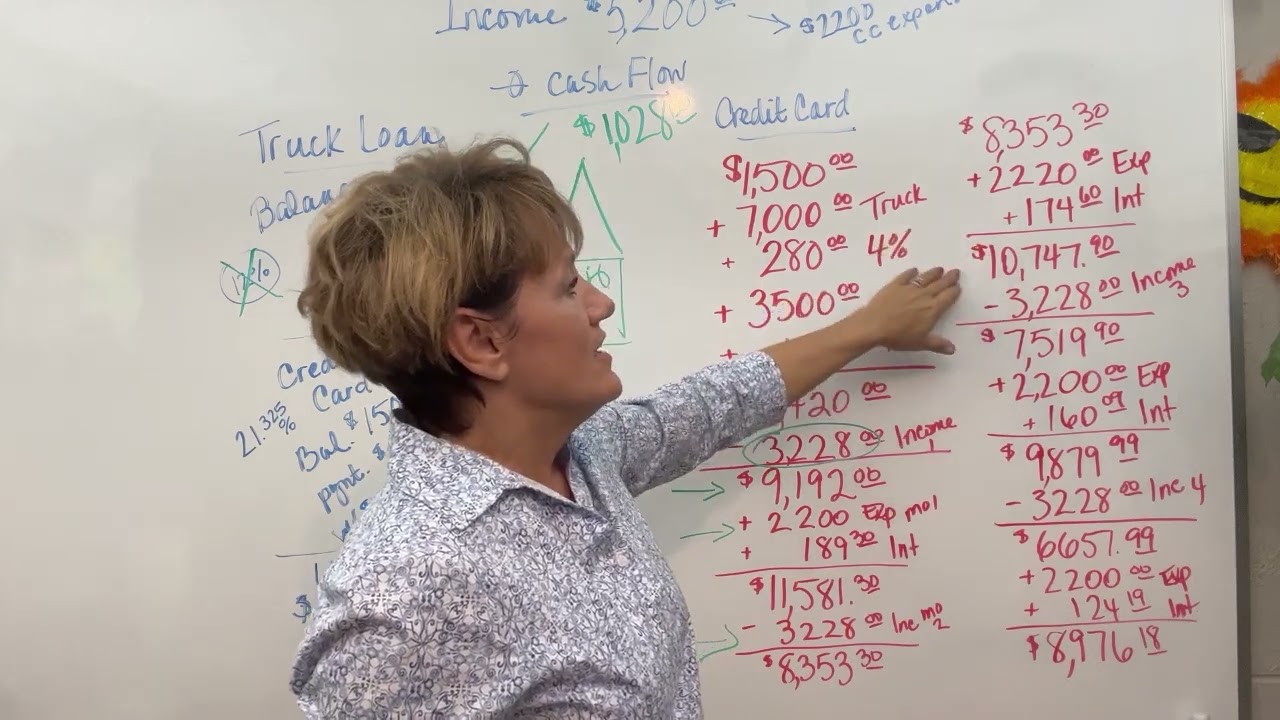

hello and welcome back to my channel I am Christy van with fantastic finances and on this channel I teach velocity banking so today we are working with a man out of West Virginia and He is wanting to pay down his credit cards as quickly as possible so we have run a scenario on his current debt and we find that he can probably get rid of those credit cards and the cars very very quickly so we start with the income which is at 8200 expenses are 53. 77 and his cash flow is currently at twenty eight hundred twenty dollars so we're going to start with this HELOC at 10 percent twenty seven thousand dollars is income the 8200 will go in in month one his expenses at 51. 27 will come out now the 5127 is the 53.

77 minus a helix 250 dollar payment because once we start doing income transfers that knocks out the payment we added the interest at 225 and month 2 income goes in expenses interests come back out month three the same thing happens but at the end of month three he is going to pay off Flagstar the 291 will now become cash flow and his expenses will go down to forty eight hundred thirty six dollars his interest is added at 199 and he stands at twenty thousand six hundred twenty one dollars and month five is income goes in is expenses and interest come back out and month six he'll do the same thing in them in expenses out month seven he comes in and he's going to pay off five of his credit cards the Discover one the Discover two the synchrony card Capital One card and Capital One card number two bringing him to a total of fifteen thousand five forty one on his balance his expenses will then be reduced because all of these payments that he was making has now been turned into cash flow and he is at 42. 61 for his expenses now the interest comes out he's back up to nineteen nine thirty two the income comes out in month eight the expenses come out month nine the same thing month ten he is going to pay off first United at ten thousand nine hundred yes these balances will probably be lower when we get there because he's been paying on this for the whole time but we just left it the same to leave room for air the expense is now are at 39. 49 after reducing this payment by three hundred and twelve dollars the interest now comes out in month 11 he transfers 8200 income back in expenses and interests come out month 12 the same thing but he's going to put 27 600 which is the car he's going to pay it off bringing his balance to thirty four thousand four Seventeen his expenses come down again because we took off that car payment over here at 485 dollars his interest is pulled out again now remember on the interest I always charge on the high balance so the 316 is 10 of the high balance in this month then in month 13 he's going to put in the income the expenses and interests come out again month 14 the same thing month 15 the same thing month 16 the income goes in the expenses and interest come out again month 17 income in expenses out month 18 the same thing month of 19 he is going to put in his income he'll be at a balance of 2833 dollars and we're going want to pick up 28 900 of this truck right here now it's forty eight nine currently but by the time he gets all the way over here to his 19th month it's probably going to be quite a bit lower but we're just going to take the 28.

9 put it in the loan because this is a fifty thousand dollar HELOC and we don't want to exceed that and we don't want to even get close to those limits so we're going to just put in a partial amount of the truck then we're going to pull the expenses and the interest back out he's going to be at 35 297 in month 20 the income is going to go in the expenses and the interest come out 21 the same thing 22 he's going to put his income in he'll be down to 18 178.