[Music] Hey everyone, welcome back to the show! Happy Wednesday, and thanks for tuning in. My name is Mike, and today we're going to be talking about three considerations for losing trades.

I've talked about a few aspects of what we look for when we're opening a trade, but one of the more difficult things, along with rolling trades or making adjustments, can be determining when we want to get out of a trade and what sort of things we want to think about when we're looking to get out of a trade. So today, we're going to highlight three things, and these are the most important considerations I have when I'm looking to close a trade. I’m going to discuss these with you, and we’re going to talk through why they’re important to me and why it might make sense when we look at different trades over our portfolio and consider whether we should get out or maybe roll for duration.

Let’s dive into the first three things we’re going to discuss today, which I've laid out here. When we’re thinking about closing trades, especially losing trades, there are a few key points I'm considering. The very first thing is going to be the directional assumption.

I’m going to ask myself, "Has my directional assumption changed, or is my directional assumption the same? " We'll walk through that. I’m also going to look at the rolling amount for credits.

If I'm looking to roll the trade as opposed to closing out of a losing trade, I’m going to assess the credit amount I can potentially receive. It is much easier to get a credit when we roll the same strike into the future for naked options than it will be for defined risk trades. Therefore, I’m going to examine this from a naked option standpoint.

The key question I’ll be asking myself is: "Is the credit large enough to merit this roll, or are there other opportunities elsewhere where I can move this capital—this buying power reduction—that I'm using up for this trade? " Should I take this trade off and allocate that capital elsewhere into a higher probability trade? Now, let’s get into the first point, which is the directional assumption.

I’ll lay out a hypothetical trade for you here. We’ll just look at a short put, and I’ll explain what might happen over the course of the trade’s time frame. The first thing we do is note the stock price right here, and let’s say I have a neutral bullish assumption, so I’m going to be selling a put.

I’ll look at a 45-day until expiration time frame, and I'll sell an out-of-the-money put, which is simply a put that’s below the stock price. When discussing calls, being out of the money would mean they’re above the stock price, but for this example, we’ll focus on selling a put. I’ll be profitable if the stock price is anywhere above my short put at expiration, but in this example, since we’re talking about losing trades, that’s not going to happen.

Fifteen days go by, and we find that the put is now in the money. The stock price has moved from here to here; my stock price is now below my put strike, so my put is in the money, and I’ll be seeing a loss at this point. Since there are still many days left until expiration, I’ll have a combination of extrinsic value, which includes time and volatility value, but also intrinsic value.

Initially, I only have extrinsic value since this put is out of the money, but the instant it moves in the money, it now possesses intrinsic value. I need to consider the volatility and time value with my 30 days until expiration left, along with adding in my intrinsic value, which will likely increase the worth of this put compared to what it was when I originally sold it. When selling options, I want the price to go down to be profitable.

However, if it goes up in price, I’ll need to buy it back at that higher price to exit the trade, which results in a loss. In this scenario, once the put moves in the money with so many days left, we will probably see a loss at that point. Let’s say another 15 days go by; now we're even deeper in the money.

After 30 days, the stock price has steadily decreased, so the very first question I need to ask myself is: "Is my directional assumption the same? " In this scenario, it might have changed. I might realize that since I've seen the stock price gradually decline over the course of 30 days, I would feel more comfortable just exiting the trade because I’m no longer bullish.

If I noticed that the stock had dipped down but then slightly rebounded with 15 days left, I might decide that we are just experiencing normal price action. However, when I observe a consistent downward trend, it can lead me to reassess my directional assumption. So, when I’m looking at closing trades that are losing, the first thing I’m going to do is… Assess my directional assumption.

So, for this example, we're actually going to assume that the stock price is going to go back up. We're going to move on to the next slide, and we're going to assume that our directional assumption is the same. However, I wanted to highlight that just to put that in front of you: if you see something that's going against you, we don't have to force ourselves to be in that position.

We can assess our directional assumption, and if it has changed, we can be more than comfortable with just taking off the trade. But for this example, we're going to look at that exact same trade, and we're going to look at rolling the trade now. So, instead of closing the trade, I'm going to look at rolling it and see what can happen if I roll that same strike out in time to add some duration to it.

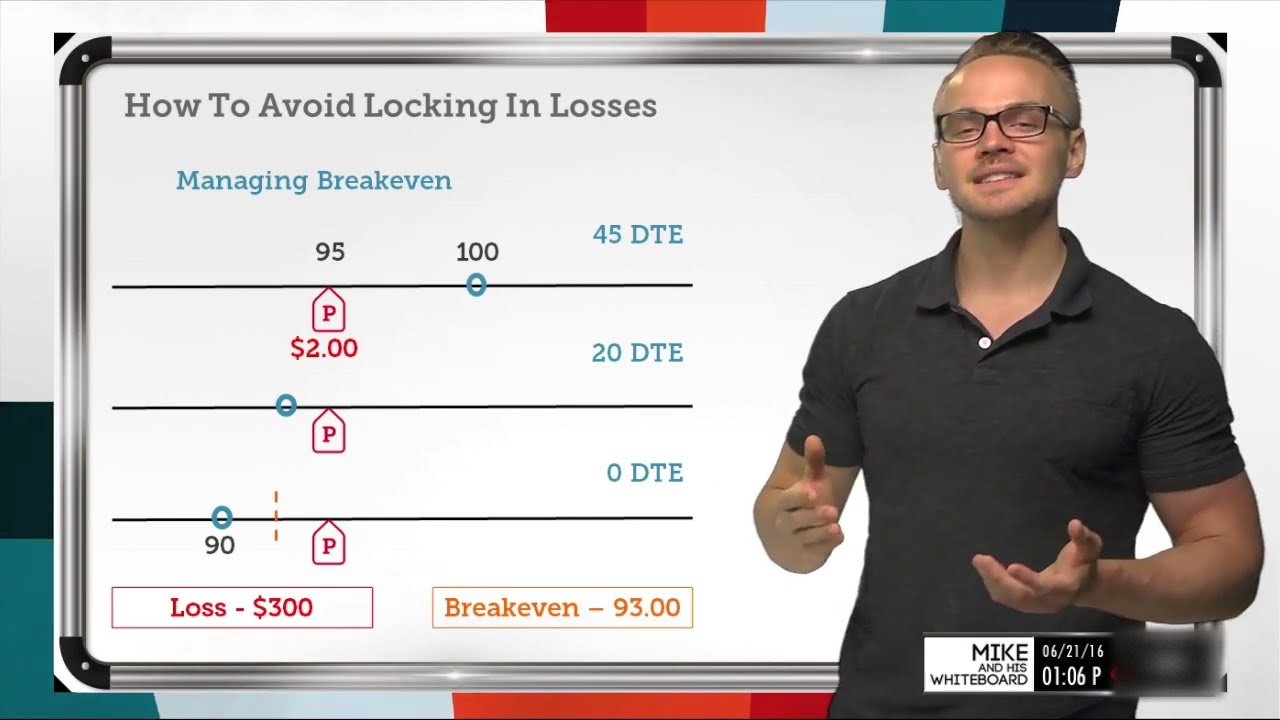

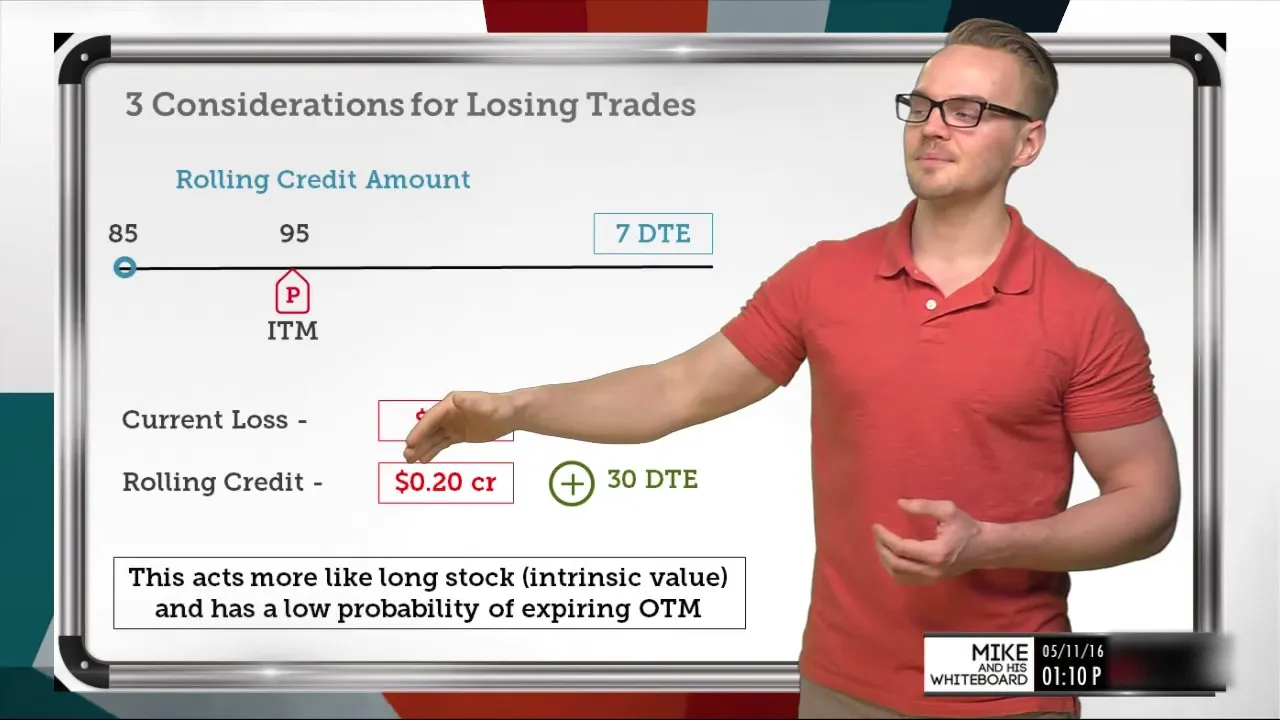

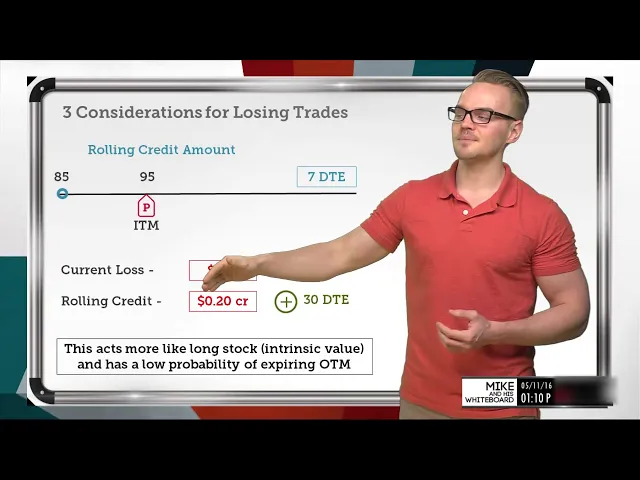

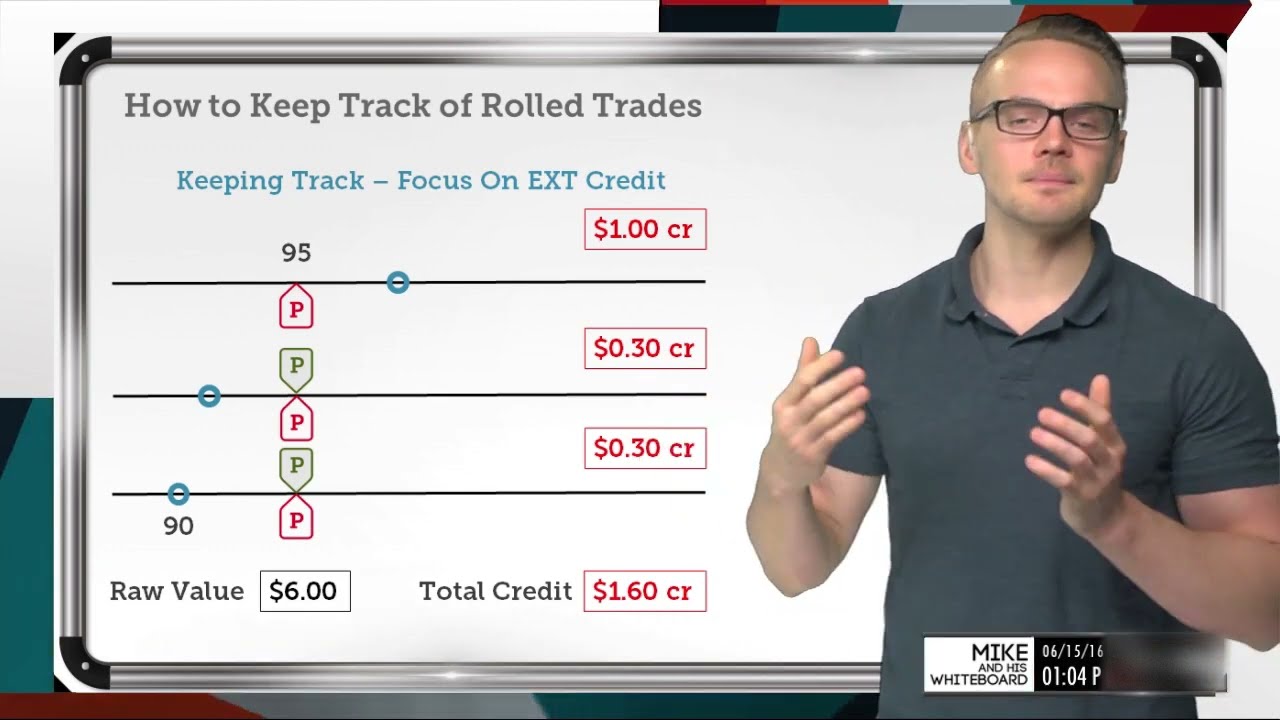

So, let's say another few days have gone by; the very last one we looked at was 15 days to go. Now that another few days have passed, we've got seven days left on that exact same option, and I'm going to throw on some values here. Let's say I originally sold that 95 strike put.

It's now completely in the money, and the stock price is at 85. If my current loss is $900 and we've got about seven days until expiration left, I know that I would have collected right around maybe $90 for it, something like that. I know that because if I have a put at 95 and my stock price is at 85, I have $1,000 of intrinsic value here; it's 10 points in the money.

Since each option contract theoretically is equivalent to 100 shares of stock, we're looking at a loss of $1,000. But if I see a current loss on my portfolio of $900, it's taking into account the credit I received, which is always going to be a good thing. Whenever I take in a credit for selling options, it's going to offset my loss by that amount—by the credit amount.

So, if I only see $900 of loss, even though I'm 10 points in the money, if I didn't collect anything, I would be at a loss of $1,000. That's good because I know that I've offset my loss just a little bit. Now, we're going to be looking at rolling this trade into the future.

So, what can happen here? If I look at rolling and credit, let's say I'm looking to roll this put on the same strike and just add duration. All I'd be doing is buying back this short option for a debit and then selling out that same 95 strike.

In this example, we're going to look at adding 30 days to that, so we're going to look at an expiration cycle that's 30 days in the future, and I'm going to look at a rolling credit of $0. 20. I would have to buy back this option for at least $1,000, regardless of what my loss is.

With my credit that I'm considering here when I'm looking at just the raw value of this option, I know it's got to be trading for at least $1,000 because it's 10 points in the money. So, when I'm looking at my seven days to go, there's still going to be a little bit of extrinsic value there. I'm probably going to be looking at buying back this option for right around $1,010, something around there, or $1,010.

We're going to be looking at just over intrinsic value since there are still a few days left with extrinsic value here, and I'm going to be looking at selling an option that's further out in the money, and I'm going to be getting a credit for doing so. This means if I'm getting a $0. 20 credit, whatever value I have to buy back this option for with seven days to go is $0.

20 less than the new option I'd be selling at the 95 strike with 30 more days to go. So, that's how it works when we're rolling something. We're basically buying back our old option and selling out a new option, and if we're able to get a credit for it, it's simply because we have more days to go on the new expiration, which is going to give it more extrinsic value—this will boost the value of the overall option.

In this case, we're looking at $0. 20 of overlay, so I've got $0. 20 more on the new option than what I'd have to pay to close out this option.

I've got a credit of $0. 20, and I'm adding some data expiration. So, there are a few things that I need to consider when I'm looking at rolling.

The very first thing I'm going to look at is what is my credit amount? Well, my credit amount is $0. 20, and I'm adding 30 days, so at this point, I would have 37 days to go.

If the stock price does not move at all, I would have reduced my cost basis by $0. 20, so my current loss would have gone from $900 to $880 if the stock price had not moved at all. So, the very first thing I need to ask myself is: is that worth it?

Is that something that I want to partake in? Especially because my option is still going to be in the money, and it's going to be mostly intrinsic value since it's so deep in the money, and I'm only getting a credit of $0. 20 of extrinsic value.

Going to be a pretty big differential between the intrinsic and extrinsic value of this option, so for that reason, this option is going to act a lot more like stock. Because of that intrinsic value, since there's only about 20 cents there, we're going to be solely relying upon the stock price going from 85 up to 95 to hopefully wipe out this loss that we have. At the same time, since it's so deep in the money, it's going to have a high probability of staying in the money, which means that it's going to have a very low probability of coming out of the money at the end of expiration.

So really, this is going to act more like long stock because of that intrinsic value, and it’s going to have a low probability of expiring out of the money, which is exactly what we want to happen: to, number one, wipe out this loss that we have, but, number two, get that total profit that we've received from the credits we received from this trade. So, let's go to the next slide, and we'll talk about another aspect that I think of when we're looking at these losing trades. We've got our trade here that we just talked about, and let's say that it was in a tech stock.

I had that $900 loss and I looked at rolling it, but I was only getting 20 cents for the roll because it was so far in the money. I didn’t have a lot of extrinsic value there, so I would only have gotten 20 cents for holding that trade for another 37 days. I would have been solely relying upon the fact that I want that stock price to increase by 10 points to hopefully reduce that loss, totally wipe out that loss, and turn that trade into a profit.

So, I could have done that, or what I could do is look for opportunities elsewhere. A lot of times, we see a loss in our position or portfolio, and we really hold a grudge against that stock. We look at that stock and we say, "Wow, I have a loss in the stock; I need to get that P&L up in that particular stock.

" But that doesn't have to be the case. One thing that we could do and consider is, instead of rolling this for such a small credit, maybe I would see something in a totally different underlying—something that's totally unrelated and uncorrelated, not positively correlated, is what we're really looking for. So, maybe I'd look at something in energy.

I could see an energy stock that's at 85; maybe it's got really high volatility, and maybe I can redeploy that capital elsewhere. So, take this trade off entirely and deploy this put in a new stock. Now, I've got a totally new trade, a much higher probability of success here.

Yes, I'm not going to be able to totally wipe out that loss on this one trade because there's no way I’m going to collect $900 for selling this $70 put. But when we look at our other opportunities, when we consider the roll of 20 cents, there’s probably a big chance that I can collect more than 20 cents by selling this put as opposed to rolling this put that's in the money. So, it's just a different way of thinking about it and disconnecting from the fact that we have a loss in one trade.

We don't need to recuperate that loss in that underlying; we can move our capital elsewhere and be more efficient with our capital. If I'm able to collect more than 20 cents with this trade and use the same buying power, this one is probably going to be a much better option than holding this one that's in the money, which also has that early assignment risk that we don't really like. So, when I'm looking at these different things, I'm also going to look for opportunities elsewhere when I'm considering closing out losing trades.

Let’s wrap all this together with some takeaways for you. The very first takeaway is, again, we don't have to chase our losers in that particular underlying; we can recover elsewhere. It’s always important to be able to pull ourselves off the table on a certain underlying, wipe ourselves clean of that position, and be able to go into a different underlying or different sector that's totally uncorrelated and redeploy that same capital elsewhere, more efficiently.

So, when we're looking at rolling, if we don't want to close the losing trade, we really need to consider the credit amount. Is the credit amount worth it to put myself in this position again with a lower probability of success, or should I take that money and move it elsewhere, as we talked about here? And again, when we’re looking at losing trades, we want to reassess our assumptions frequently.

Even if we have winning trades or if we have trades that are pretty much neutral, it's really important to continually reassess our assumptions so that we don't find ourselves in a trade that we don’t even want to be in anymore. So, thanks so much for tuning in. This has been three considerations for losing trades.

If you've got any questions or feedback, shoot me an email here, or you can follow me at DotTraderMike. Stay tuned though; we've got Jim Schultz coming up next.

![Upbeat Lofi - Deep Focus & Energy for Work [R&B, Neo Soul, Lofi Hiphop]](https://img.youtube.com/vi/THh4fT0O7IY/maxresdefault.jpg)

![Upbeat Lofi - Power and Energize Your Workday - [R&B, Neo Soul, Lofi Hiphop]](https://img.youtube.com/vi/ONcY0BM5EAg/maxresdefault.jpg)