[Music] [Music] Hey guys, welcome back to the show! Thanks for tuning in. My name is Mike; this is my whiteboard, and if you're brand new to this show, this is a show where we take concepts and we break them down and build them up visually for you.

We talk about concepts, strategies, anything under the sun when it comes to options. So today, we're actually going to talk about normal versus dynamic iron condors. So, Nikki Batt and his dad, Big Bat, talk about this on their show at two o'clock every day.

They usually deploy dynamic iron condors as opposed to regular iron condors for a few specific reasons. We're going to break down the differences and explain why one might be better than the other. So first, let's talk about the normal iron condor, and we'll walk through how we would set this up and what we're really looking for when we're deploying this trade.

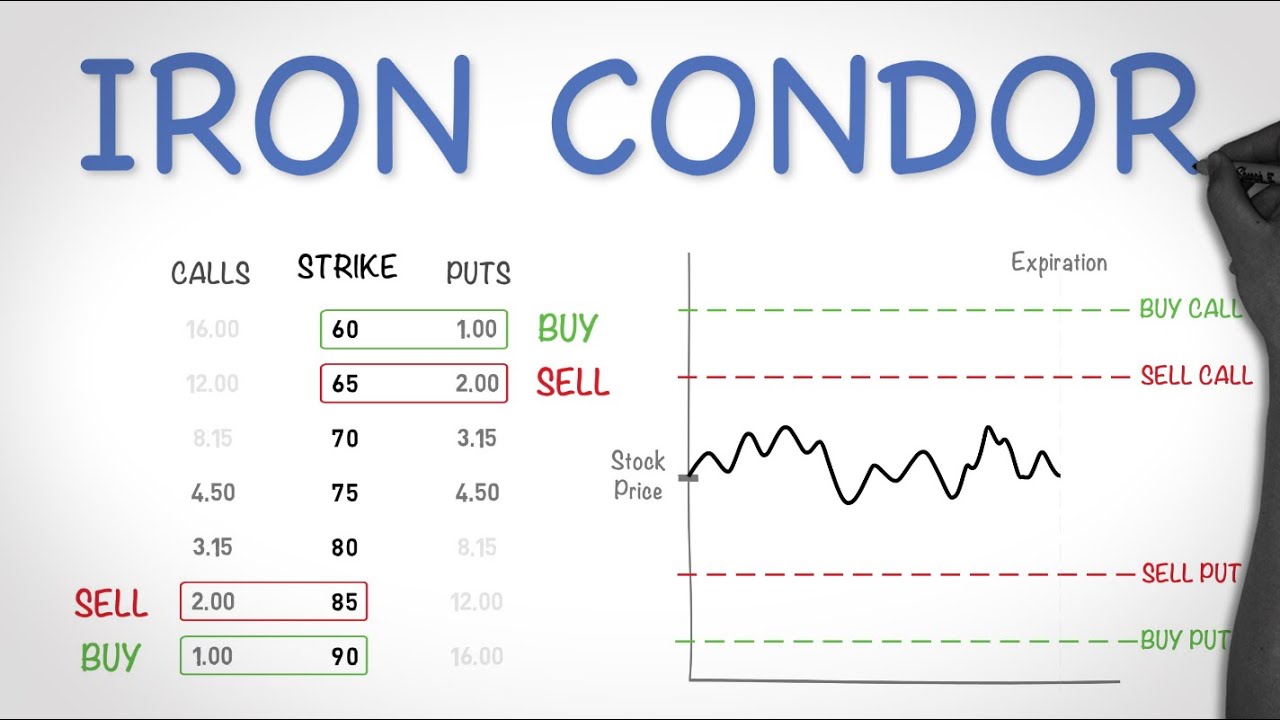

With a normal iron condor, what we really are doing is we're selling an out-of-the-money put spread, as you see here, and we're also selling an out-of-the-money call spread. In doing so, we create these two spreads that are normally directionally opposing if you do them separately. When we're selling a call spread by itself, we have a bearish assumption, and when we're selling a put spread by itself, we have a bullish assumption.

But when we do these together, we basically want the stock price to go anywhere between this range, and in this case, it would be between 90 and 110. Because at expiration, whatever credit we received, we would be able to keep as profit as long as the stock price is between this range, because all of these options would expire worthless and out of the money. So, the very first point I want to make about a normal iron condor is that it is based on equidistant strikes.

We're normally looking at just keeping a very equidistant range here. As you can see, this is perfectly symmetrical. We've got this stock price at 100, and we're selling that 110 call and buying a 115 call, so we're 10 points away on the upside.

We have a 5-point wide wing when we're looking at the call spread, and we have the exact same thing but just to the downside for the put spread. So we're 10 points out of the money, which brings us to 90, and we're purchasing a five-point wide spread there, purchasing that option at 85 to create that five-point wide wing on the downside. So, one thing to note is that this is a neutral strategy, but there are volatility skews that can happen in the market.

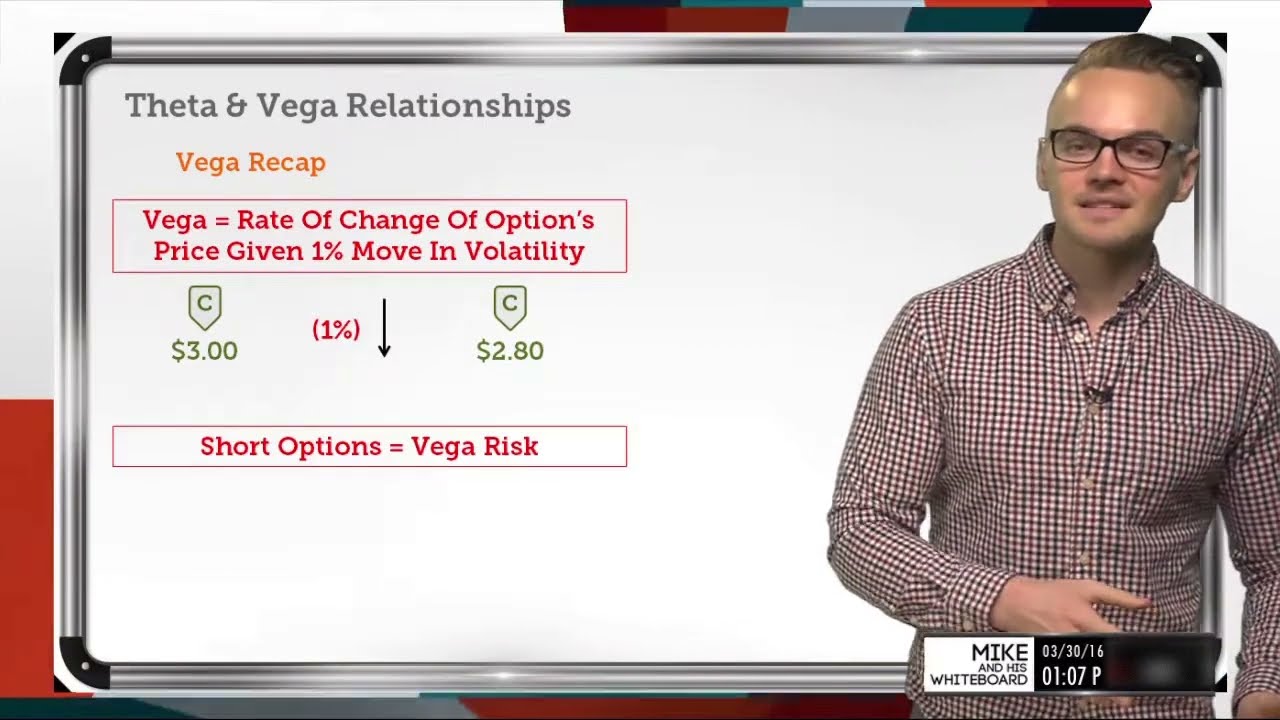

When we're looking at a normal iron condor, while this will be almost delta neutral, it usually won't be perfectly delta neutral because these deltas on the call side will likely have a different delta than on the put side. So, it doesn't account for the volatility skew, regardless of whether we have a normal volatility skew or a reverse volatility skew. On the next side, we're going to talk about a normal volatility skew and how that might affect these options.

When we're looking at a normal volatility skew, basically what we're looking at is an environment where puts are trading richer than calls. So if I were to be looking at a stock price trading at 100, and I went 10 points to the downside and I compared the value of that put to a call that was at 10 points to the upside, where I'm looking at equidistant strikes, in a normal volatility skew, what I'll see is that the puts will trade richer than the calls. That's because there is more downside reluctance, so people are purchasing those puts, which are pushing up the value of those options, as opposed to the calls where people are normally hedging their long stock.

They're looking to purchase puts to completely hedge that long stock, or they're looking to sell calls to hedge their long stock a little bit. In any case, when we're purchasing options on the put side, that's going to push the value up of those put options, and when people are selling calls on the upside, that's going to create a skew and give a difference when we're looking at these equidistant strikes. So what we would do for a dynamic iron condor to account for this is instead of creating an iron condor where we're looking at just creating equidistant strikes, what we would do is actually look at the delta of these options.

When we're looking at different values of options, especially when we're looking on the put side, if the values are spread out much wider across the spectrum of out-of-the-money options, what we'll see is that the probabilities will reflect that as well. So when we're going down to a certain strike, when we're looking at an equidistant strike on the put side and comparing it to an equidistant strike on the call side, if the put options are trading for more value than the calls, that usually means that they're going to have a higher probability of being in the money. And as we know, we can use delta as a proxy for probability of being in the money.

So if I have a delta of 20, for example, I would expect to see that same option have a probability of expiring in the money of around 20 as well. So with a dynamic iron condor, what we're really doing is we're taking this into account. We're taking into account that volatility skew, and as opposed to just creating a symmetrical equidistant iron condor, we're placing our strikes based on delta values.

So the very first thing I want to point. . .

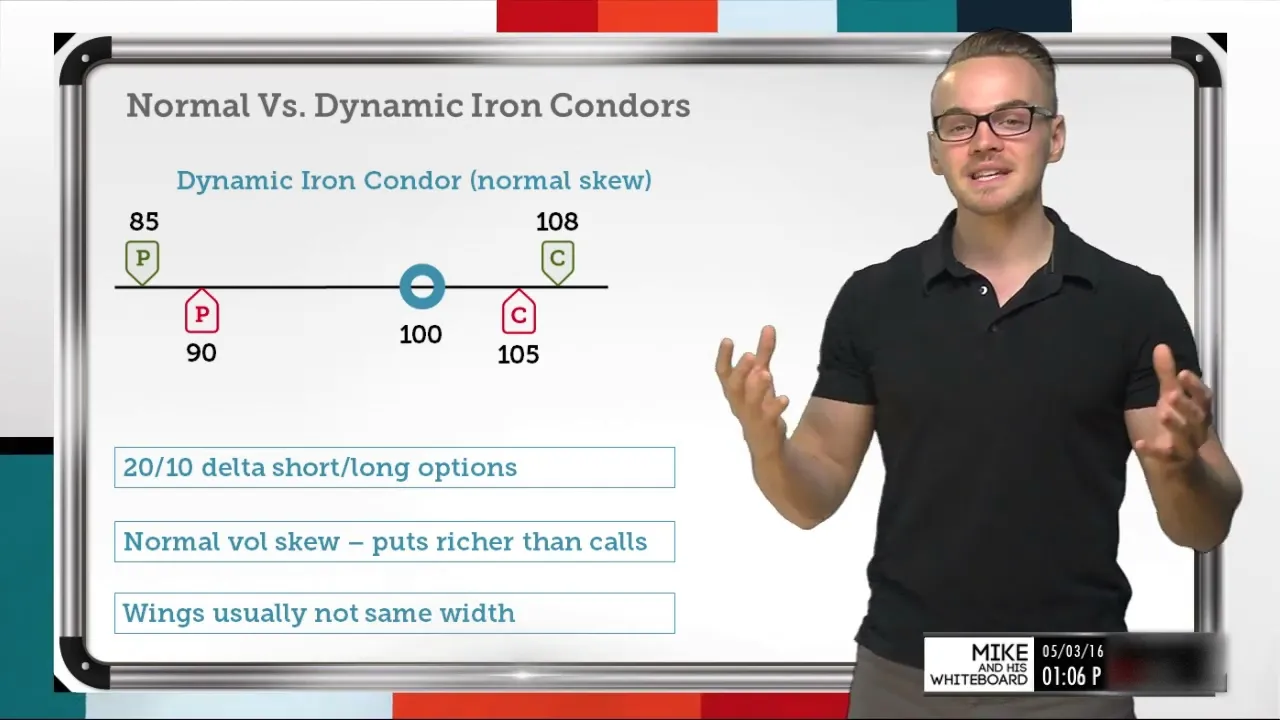

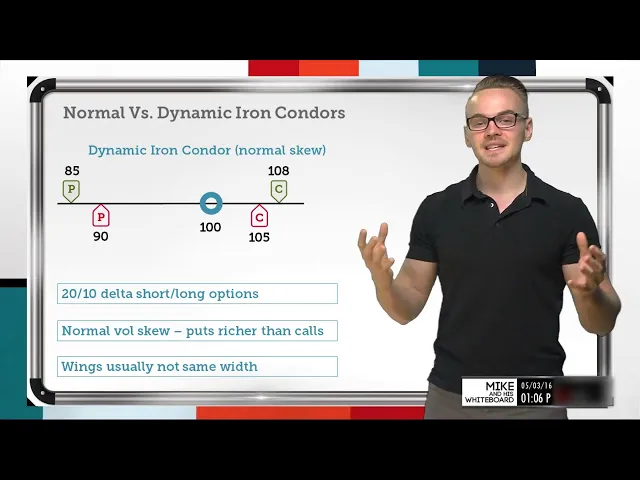

Out is that when we're looking at a dynamic iron condor, we're going to be looking at selling our short options at a 20 delta and buying our options that are even further out of the money to define our risk at a 10 delta option. So, we're going to be looking at selling our options on the 20 delta and buying our options on the 10 delta. With a normal volatility skew, this is what something might look like when we're looking at that normal volatility skew, where again calls are trading for less value than puts at equidistant strikes.

If I'm looking at keeping those deltas very similar and really honing in on that delta neutrality while taking into account that volatility skew, you might look at something like this: I've got the stock price at $100. We've just shifted our alignment a little bit; still got the stock price at $100. Maybe, since we have such a severe skew, as I'm exemplifying in this image here, we might look at a 20 delta option that's just five points out of the money on the upside.

We might have a 10 to 20 delta option here that we would sell, and I could just go three points even further out of the money to get that 10 delta option. So again, I'm looking at selling my 20 delta option here and buying my 10 delta option here. Now, as we said in a normal volatility skew environment, puts are going to be trading richer than calls, and usually we're going to see that probability curve spread even further out of the money.

For that reason, I might have to go much further down. As you can see, to get my 20 delta option with calls, I only had to go five points out of the money on the upside, but in a normal volatility skew, I might have to go 10 points down on the downside for those puts. So, to get that 20 delta value for the short put that I'd be selling, I might have to go to the $90 strike, as you see here.

Another thing to point out is, since I have to go so far down, I might not have to go down three points to get that 10 delta option as we saw here; I might have to go even further down. So, as you can see, we've got a three-point wide call spread here and a five-point wide put spread there. So again, when we're looking at a normal volatility skew, we're looking at a scenario where puts are trading richer than calls, and it's really important to remember that when we're using this sort of dynamic iron condor, the wings are usually not going to be the same width.

We're definitely not going to be very symmetrical if we're taking into consideration that volatility skew. But something that you might not notice is just that wing width here. My max loss potential should be calculated off my widest wing because, if my stock price blows down to the downside—let's say it goes to $70 or $65 or even $80 for that matter—I'm going to be looking at a spread that I'm going to have to buy back for five points on the downside compared to a spread I would have to buy back for three points on the upside.

This is a good example of a regular normal skew; this is normally what we'd see in a market, in a daily market, if we're just looking at the market here. But there are some scenarios where we might see a reverse skew. So, let's go to the next slide, and we'll talk about a reverse skew and how we might envision that.

With a reverse skew, it's going to be just the opposite. But one thing I want to point out is that a reverse skew is a lot more rare. When we're looking at a normal U.

S. equity market, we're going to see a lot more perceived risk to the downside. If we think about how markets move, we usually see markets drift up slowly over time, but when crashes happen, they crash violently.

For that reason, we're usually going to see a normal skew. However, there are some situations where we might see a reverse skew, and I've got some ideas here as to why we might think that. If we have a reverse skew, that means that calls are trading richer than puts.

But there are some reasons why that might be happening. Well, let's talk about upside protection. Maybe people are buying calls; perhaps they've shorted stock or are just speculating that they're super bullish on a stock.

You might see a temporary boost in calls being purchased that might come around earnings or maybe just some hyped-up news that might come out in the marketplace. So really, there's a lot of speculation as to why we might see a reverse skew. I was actually talking to Nick earlier today; we talked about commodities and how this might play into effect.

If you think about something like oil or gold, there's not really that perceived risk of these underlyings going to zero. So, when we have a market that has had a big downturn, like we've seen in the last few months with oil and gold, before it's been rallying pretty viciously, we look at these commodities and really ask ourselves: do we see these things going to zero? If our answer is no, then it makes total sense that we might see a reverse skew.

We might see a lot of people buying calls or buying call spreads to be speculative on that instrument, especially when we're looking at things that have. . .

Beaten up, been beaten up over the past, and we don't really believe that there is really going to be going to zero. So these are a few reasons why we might see some reverse skew. But again, it's really just the opposite of what we just saw.

So when we're looking at a reverse skew, we've got calls that are trading richer than puts. If calls are trading richer than puts, we're going to see the probability curve and the delta curve be much more wide and flat on the upside, as opposed to a normal skew, where it's pretty sharp and all of the probabilities and deltas pretty much collapse right when we get out of the money. So if we see a reverse skew, when I'm looking to set up this dynamic iron condor, and I'm looking to sell my short option on the 20 delta and buy my long option on the 10 delta, it might look something like this: I might have to go 10 points out of the money on the call side, sell that 20 delta option, and then go five points even further out of the money to purchase that 10 delta option.

On the downside here, since the skew is reversed and we see a lot less activity on the put side, and we see that probability curve pretty much drop off, I might not have to go too far out of the money. So I might be able to go five points out of the money and get that 20 delta put and then purchase a 10 delta put that's just three points further out of the money. So again, we see a situation where we're definitely not symmetrical, but it does account for the volatility skew that's baked into the market.

This is going to be much more delta neutral because we're really looking at these options from a delta perspective. If I'm selling a 10 delta here and I'm purchasing a 10 delta here, and I'm selling a 10, 20 delta here and I'm purchasing a 10 delta here, when I look at those deltas from the standpoint of the position, I'm going to be able to hone in on that 0. 00 delta much more than if I were to not take into consideration volatility skew and just look at that symmetry in terms of setting up the trade.

So when we're placing this trade, we usually look to collect one dollar; that's usually our benchmark or right around there, and we're not really concerned with collecting a certain amount of width like we are for a normal spread. So with a put spread or a call spread or even an iron condor, we usually look to collect one-third the width of the strikes to give ourselves a probability of success of around 70 percent. But in this particular scenario, because we are accounting for the volatility skew and because we believe that that is going to be baked into the option prices and that market, we're really just looking to collect right around a dollar to stay engaged.

Really, this is just more of a theta and volatility play than a symmetrical neutral balanced idea, so we're really taking into consideration the volatility skew, which is why we're really just looking to collect that dollar value and not really concerned with collecting a certain amount of width with these spreads. So let's wrap all this up with some takeaways for you here. The very first takeaway we've got is that a normal iron condor is equidistant, but it's not going to account for that volatility skew.

A normal skew, again, is really where puts are trading richer than calls. You'll usually see this a lot more often than that reverse skew, where calls are trading richer than puts. When we're looking at that dynamic iron condor, we're looking to place our strikes at a short delta of 20 and a long delta of 10, and that's usually not going to be equidistant in terms of symmetry.

It's not going to usually be equidistant in terms of the wing width on either side, regardless of whether we're looking at a reverse skew or a normal skew. So it's really important to determine what width is the widest and determine your max loss from that scenario. Thanks so much for tuning in!

Hopefully, you've enjoyed this segment. If you've got any subjects you'd like to see or any feedback at all, shoot me an email, or you can follow me at @dotradermike on Twitter. Stay tuned, though; we've got Jim Schultz coming up next!

![Iron Condor Management Results from 71,417 Trades [STUDY]](https://img.youtube.com/vi/cu1FXt4JEs8/maxresdefault.jpg)