[Music] Hey everyone, welcome back to the show! My name is Mike, this is my whiteboard, and today we're going to be talking about Jade Lizard adjustments. The Jade Lizard is actually a strategy that Liz and Jenny coined, where we're selling a put and we're also selling an out-of-the-money call spread against it.

So, we're going to walk through some things that might happen throughout the trade: if the stock goes down, if it goes through the call spread, or if it doesn't change at all. We'll discuss what we can do and some things that we're going to consider when managing or adjusting this specific trade. I did complete some other adjustments with covered calls and a short put in my previous whiteboard segments, so if you missed those, definitely check them out!

Just click on "Find Shows" at the top on Mike and his Whiteboard, and you'll see them there. They're pretty recent. But let's get right into it, and we'll break down the beginning Jade Lizard trade.

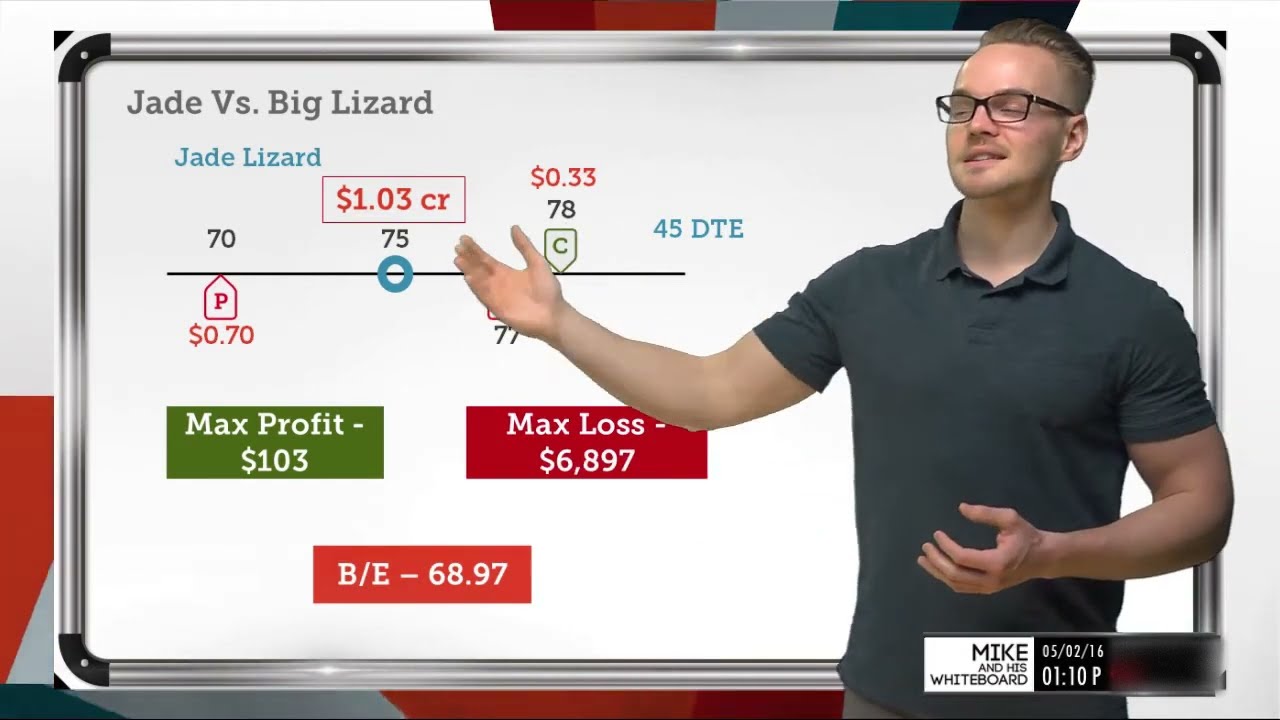

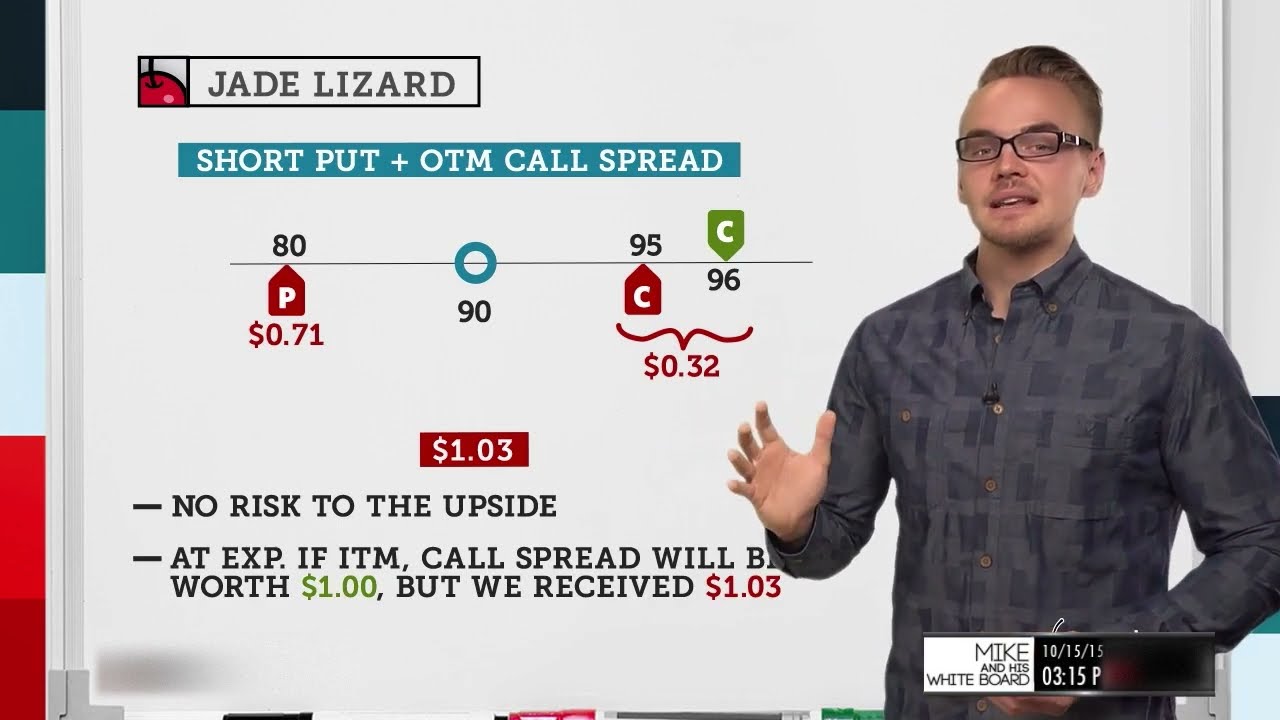

So, when we're looking at the opening trade, again, we're selling an out-of-the-money put, which would be a put below the stock price. In this example, we're looking at a stock price of $75, and we're selling an out-of-the-money call spread against that as well. We're looking at a 45-day expiration cycle.

The key to this trade specifically is making sure that the total credit that we receive—from selling the call spread and the credit from selling the put—equals or exceeds the width of the call spread here. So, I know that if I'm selling a $77 call and I'm buying a $78 call to define my risk, then I have a one-point wide call spread here. I want to make sure that the total credit I receive is over one dollar, and that's because if I do that, then I limit the risk to the upside.

So, let's talk through how that works. Let's say I've got my stock price at $75, and here I've collected 70 cents for my put and 33 cents total for this call spread. I have a max profit of $103, or $103, if the stock price stays between $77 and $70.

That would mean that my put would expire out of the money and worthless, and it would disappear from my account. The same goes for the call spread up here since these are all out-of-the-money options. If the stock price is between these strikes at expiration, I would be able to keep the credit I received and reach my max profit of $103.

That means my breakeven is at $68. 97. If I take my total credit, remember that whenever we're selling premium, our breakeven is going to be helped by the credit we receive.

My breakeven would be to the downside here. So, all I'm doing is taking that $103 value and subtracting it from my short put strike, which gives me my breakeven of $68. 97.

Now, this is also going to be my max loss if the stock price ends up going to zero. However, I'm in a better situation because my max loss would be $68. 97, rather than if I had just purchased the stock outright at $75.

So, it's a great cost basis reduction strategy, and it gives us a reason or way to be correct in a zone: between $70 and $77, I would be able to keep that $103 of max profit if the stock price is there at expiration. So, let's talk about what happens if the stock price goes up through this level here. If it goes up, I'm going to have to buy back my call spread for $1 or maybe $1.

01 at expiration. I know that I collected $1. 03 total, and I have to buy back my spread if the strikes are breached and the stock price goes all the way up to, let's say, $80 or $90.

It doesn't really matter; I know I'm going to have to buy back that spread for the intrinsic value at expiration. Since I have a one-point wide spread here, if it's completely in the money, it should be trading for around $1 at expiration. However, I'm not going to have any risk to the upside because I collected $1.

03. So, if I collect $1. 03 and I have to buy back my spread for $1 or $1.

01 or maybe $1. 02, then the difference there is going to be my profit. Even if the stock price blows through the upside, I would still make about three dollars, or three cents in the options trading world, which would bring me to about breakeven after the commissions with this trade.

But let's talk about some things that can happen with the trade. Let's go to the next slide, and we'll discuss what might happen when the stock moves down. So, what are some things I can do?

The cool thing with spreads is that when we define our risk, we don't necessarily have to move that option. One thing to consider is possibly just moving the short strike down. Maybe I'll look to see what sort of credit I could receive.

The most important thing to remember, though, is that if I do this, my one-point wide spread now becomes a five-point wide spread. So, if for some reason the stock price blows all the way back from $69 up to $79 or $80, I'm going to see a loss on this. Call spread now, because even though I would be collecting more, my max profit would be $153 if I received a 50-cent credit for this roll, rolling my call down to the 73 strike.

I do still have that five-point wide spread here, so I'd be losing about $350 if the stock price blew all the way up past $80 with 35 days to go. So that's one thing to remember when we're looking at just moving the short strike. However, if I do just move the short strike and I'm able to roll it down a couple of strikes for a 50-cent credit, I would increase my max profit to $153.

Now, where is that max profit going to be? Of course, since we're looking at out-of-the-money options, the max profit would be between $70 and $73. So, if the stock price is at $71, $72, $72.

50, or even $72. 99, it's not going to matter because my short put would be out of the money, my short call would be out of the money, and of course, if my short call is out of the money, my long call would definitely be out of the money as well. So, I would be able to keep that total credit of $153, and it's going to help my breakeven go down to $68.

47. So, my breakeven's benefiting by 50 cents since I would be rolling it down. The cool thing about that is that even though my short put is currently breached, if the stock price stays at $69, as you see it here, if my breakeven is at $68.

47, I stand to make $0. 53 on this trade if the stock price stays right at $69 at expiration. Yes, I would have to buy back my short put for $1, because again, when we're looking at in-the-money options, if we want to close them out at expiration, we have to close them for their intrinsic value or close to their intrinsic value.

So, if the stock is at $69 and my short put is at $70, I've got one point of intrinsic value, but I would have collected $1. 53 that I can use to offset that. So, I would collect $1.

53, I would buy back my short put for $1, and that would net me that $0. 53 or $53 profit in the long run. With that said, if my breakeven is at $68.

47, that means that my max loss is also at $68. 47, and again, that's if the stock price ends up going all the way to zero; that would be the worst-case scenario for this specific trade. So, let's go to the next slide here, and we'll talk about if the stock moves up, what we can do.

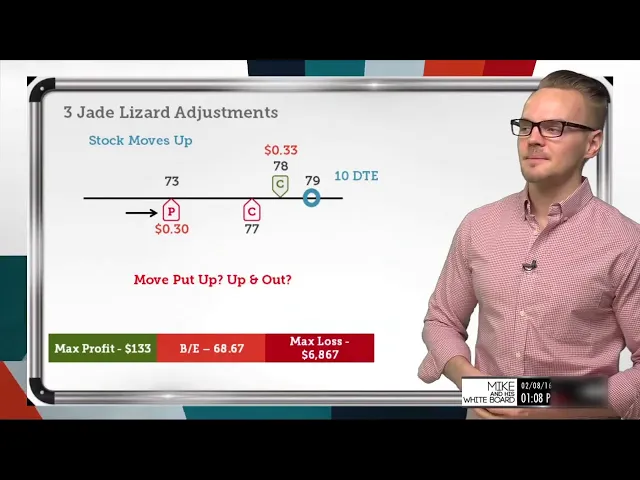

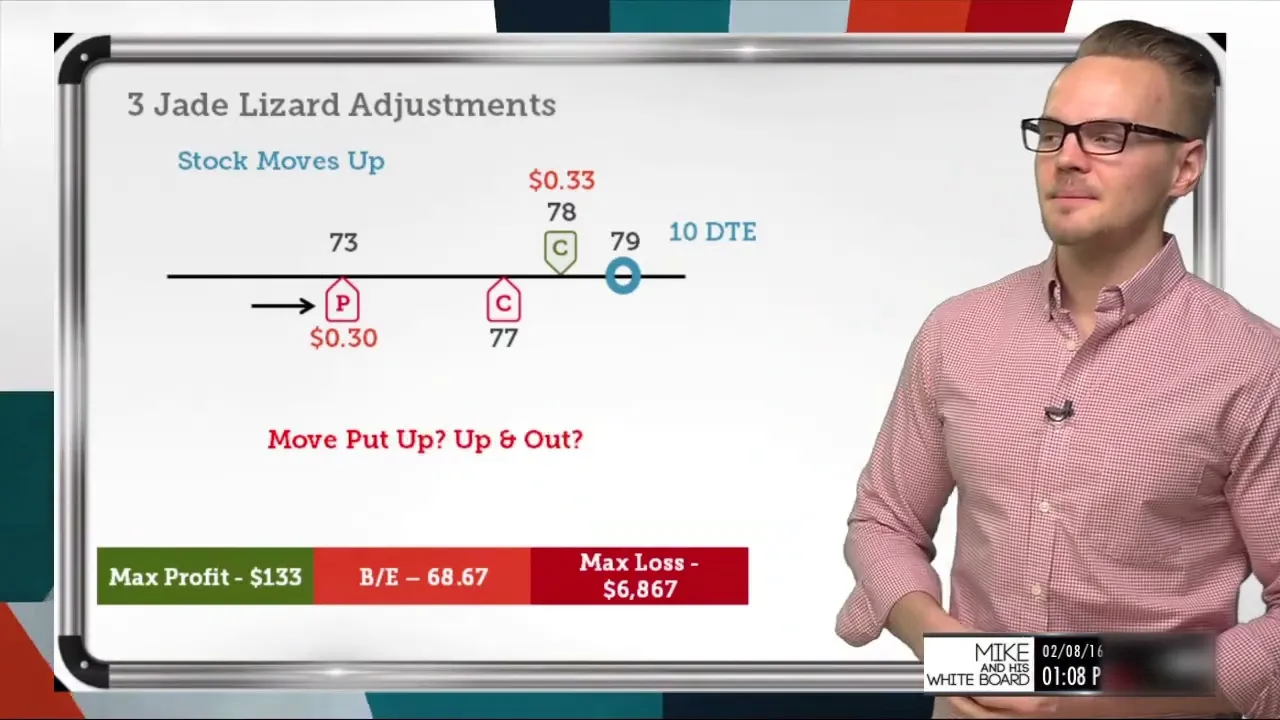

So, if we're comfortable with just scratching on the trade, then maybe we wouldn't do anything. If the stock moves up and goes through our call spread, then maybe we'd be fine with a breakeven, but there is an alternative, and that might be moving the short put up, maybe moving it up and out depending on the expiration. But let's just talk about just moving it up.

So, let's say I can move my strike from $70 to $73 and I can collect $0. 30 with 10 days to go. So, there's only 10 days left; I can get a little bit of a credit here and basically increase my max profit to $133.

So what happens when I reach max profit in this scenario? Well, the stock price would have to be between $73 and $77. The same thing applies; we would need these options to expire out of the money to reach that max profit.

But if we continue to go up with the stock price, and I know that I originally collected $0. 33 for this side and what was that? $0.

70 on the other side for a total credit of $1. 03. If I move this short put up to collect another $0.

30, what would happen? So, if the stock price is above this spread at expiration, maybe I realize that I'm now bullish on this underlying. I'm no longer neutral to bullish; I'm now fully bullish.

So, maybe I'd look to roll my put up and collect another $0. 30. If the stock price stays above this short call spread, number one, I would have to buy back the spread at expiration if I didn't want to have assignment fees or get those assignment fees on just these short options here.

So what I'd have to do is buy back the spread for close to $1. If I collected $1. 33 and I have to close this spread specifically for $1 now to avoid those assignment fees, then I would net the profit of $0.

33. So, instead of breaking even on this trade, if I roll my put up, I can now profit to the tune of $0. 33.

Although I collected $1. 33, again, I would have to buy back the spread that these options are in the money at expiration with 10 days left to go. But since I would be able to roll that for $0.

33, that gives me an extra profit potential to the upside. Another thing to consider is rolling up and out. So, maybe I can get an even larger credit with the put, or maybe I wouldn't have to roll it up so high if I roll it out in time as well.

As we know when we're looking at options that are further out in time, they're going to have more value, just like an insurance policy or any other sort of policy where there's a longer duration, and we're paying something to have that duration if we're selling these options. We're going to be collecting more premium because of the fact that they have more time in the options themselves, so they're going to be worth more. So maybe instead of just rolling up, maybe I'd consider rolling up and out in this situation to give myself some more time to be correct and, at the same time, collect even more profit.

So if I did just roll this up, I would collect another 30 cents, which would reduce my overall break-even from 68. 97 to 68. 67, and my max loss would again be the same as the break-even in this situation, so it would be 68.

67 if the stock price went to zero. Now let's go to the last slide here, and we'll talk about what happens if nothing happens. So if the stock stays the same, I'm not going to make any change at all.

Like I've referred to in the past two examples, if the stock price is right in between our strikes of 70 and 77, then I'm going to reach full profit potential. I would make that 103 that I originally sold the spread for. But one thing to consider is: where is the volatility?

If I've got five days to go and I feel pretty strongly that I would be able to let all these options expire out of the money, maybe I'll look at redeploying this trade if implied volatility has increased, regardless of what these options are trading for. Now, if they stay out of the money, they're going to expire worthless and disappear from the account. But if implied volatility has increased, that means that I should be able to move the strikes out further and collect around the same amount.

So if I'm looking to collect about a dollar three and implied volatility has increased, maybe I can move the put down in the next month to 68 and move this spread up maybe to 79 and 80. So I can make a wider range and collect the same amount when implied volatility is higher. So it's always good to consider, if we have the same assumption on an underlying and we want to redeploy it, where's the volatility at?

Can I get a little bit wider and collect the same amount, or can I keep these same strikes that I'm comfortable with and collect a little bit more? Both are probably going to be the case if implied volatility has, in fact, increased. So let's wrap all these up with some examples here or some takeaways.

So we've got premium selling trends. If you've seen any of the previous adjustment trades, you can see that there's a trend. So if the stock price moves up, we tend to roll the untested side up or up and out in time.

In this specific example, if the stock price does move up and if we collected more premium than the width of our call spread, then we've successfully created a jade lizard, and we wouldn't have any more additional risk to the upside. So it's important to just remember that if the stock price does go through that call spread, it's okay. We're going to be profitable; whatever is over that difference in the call spread is going to be our new profit, and after commissions, we would probably break even on this specific trade.

The second takeaway is that the key to adjusting is reducing cost basis. So you're never really going to see us roll for a debit; we usually try to roll for even money or zero dollars or roll for a credit. If we roll for a credit, we're able to reduce our break-even point and increase our probability of profit in the long run with the trade.

The more we reduce our cost basis, the higher probability we'll have to be successful in the long run. Even though our options would be in the money, it is going to give us the benefit of reducing that cost basis further. And lastly, the long option doesn't have to move.

So in the second example, and especially in IRA accounts, you'll see Liz and Jenny and a lot of other people buying far out-of-the-money options to use to create synthetic scenarios. So maybe with a strangle or even with a straddle, something like that, you might see people buying far out-of-the-money options and leaving them there, even if they're adjusting the short strikes to manage delta or whatever they're looking to manage. Those long options don't necessarily have to move if we're comfortable with the risk that we're creating when we're adjusting the strikes within them.

So, like the second example with the jade lizard, we can move just the short call down and collect more than if we would have moved the entire spread, but it is going to expose us to the upside risk there, so it's something to be aware of for sure. So these have been my three jade lizard adjustments. Hopefully, you enjoyed them.

Thanks so much for tuning in! If you've got any feedback or questions at all, shoot it over to support@doe. com, or you can tweet me at @doTraderMike.

We've got Jim Schultz coming up next, though, so stay tuned. Hey everyone, thanks for watching our video! If you liked this video, give it a thumbs up or share it with a friend.

Click below to watch more videos, subscribe to our channel, or go to our website.