The moment your paycheck hits your bank account, you have exactly 15 seconds before your brain starts making terrible financial decisions. I'm not kidding. 15 seconds is all it takes for most people to mentally spend money they haven't even seen yet.

Your brain starts calculating how much you can blow on that new gadget, how many times you can order takeout this month, or whether you can finally afford those shoes that have been sitting in your online shopping cart since last Tuesday. But what if I told you that those same 15 seconds could be the difference between staying broke forever and actually building real wealth? What if there was a simple routine you could follow every single time you get paid that would automatically put you ahead of 90% of people financially?

My name is Nick and I've spent years helping people figure out what to do with their money the moment it shows up in their accounts. If you're tired of wondering where all your cash goes every month and you actually want to build something meaningful with your income, make sure to subscribe to this channel and hit that like button if this information helps you out. Here's something that might shock you.

The average person has no clue what happens to their money after they get paid. They know their rent gets paid somehow. Food appears in their kitchen and their Netflix subscription magically renews itself.

But beyond that, it's complete financial chaos. like they're basically financial sleepwalkers stumbling through life wondering why they never have anything left over at the end of the month. The reality is that most people treat their paycheck like a surprise birthday gift instead of treating it like the powerful wealth-b buildinging tool it actually is.

Uh they get excited when it arrives, spend most of it on random stuff they probably don't need, and then spend the next two weeks eating cereal for dinner and checking their bank balance obsessively. But successful people do something completely different. They have a system.

They have a routine. And that routine starts the moment their paycheck arrives. It's not complicated.

It's not sexy. And it definitely won't get you a million followers on social media, but it works. And it works so well that once you start doing it, you'll wonder how you ever managed your money any other way.

The secret is understanding that your paycheck isn't just money you earned. It's your future financial freedom chopped up into monthly installments. Every dollar that comes into your account is a tiny building block that can either contribute to your wealth or disappear into the black hole of mindless spending.

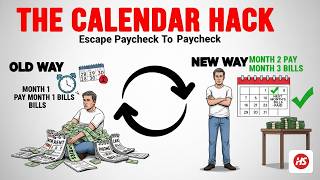

Most people approach their finances backwards. They pay all their bills, buy whatever they want, and then try to save whatever's left over. Spoiler alert, there's never anything left over.

It's like trying to fill a bucket with a giant hole in the bottom and wondering why you can't hold any water. The people who actually build wealth flip this entire process on its head. They pay themselves first, allocate every dollar with intention and make their money work as hard as they do to earn it.

They understand that financial success isn't about making more money, although that certainly helps, right? It's about having a system that works regardless of how much you earn. Think about it this way.

Um, if you make $50,000 a year and you save and invest 10% of it consistently, you're going to be in better financial shape than someone who makes $100,000 a year but spends every penny they earn. The person making less money but following a system will retire comfortably while the higher earner will be working until they're 80 because they never learned how to manage what they had. This brings us to the foundation of everything we're going to talk about today.

Before you can build wealth, you need to know exactly where your money is going. And I mean exactly. Not some vague idea about your major expenses, but a precise understanding of how every dollar gets allocated.

The first step in our paycheck routine is something that sounds boring, but is absolutely critical to your financial success. You need to determine what percentage of your income goes toward necessities. These are the things you literally cannot live without.

Um, we're talking about housing costs like rent or your mortgage payment, food that actually keeps you alive, basic transportation, essential utilities, and healthcare. Notice I didn't include your premium cable package, your gym membership you never use, or your subscription to 17 different streaming services. Those might feel necessary when you're binge watching your favorite show, but they're not actually required for your survival.

Here's where most people get this completely wrong. They look at their expenses and convince themselves that everything is a necessity. That expensive car payment becomes essential transportation.

The daily coffee shop visits become necessary fuel for productivity. The weekly restaurant meals become crucial social activities. But here's the reality check you probably don't want to hear.

If you're spending more than 60% of your take-home pay on true necessities, you're either living somewhere too expensive for your income or you're calling luxuries necessities because it makes you feel better about your spending choices. Let me give you a real example that might help put this in perspective. Imagine someone earning $75,000 per year.

After taxes, they're taking home roughly $4,750 each month. If their rent is $1,800, their car payment is $400, and they spend $500 on food, they're already at $2,700 in monthly expenses. That's about 57% of their take-home pay, which is actually pretty reasonable for someone living in a higher cost area.

But here's where it gets interesting. That same person might look at their budget and think they're barely scraping by, especially if they're also paying for streaming services, eating out regularly, buying coffee every day, and making other small purchases that seem insignificant individually, but add up to hundreds of dollars monthly. The key is being brutally honest about what you actually need versus what you want.

Your future financial freedom depends on your ability to make this distinction clearly and consistently. Once you know your true necessity percentage, you'll know exactly how much money you have available for everything else. And everything else is where the magic happens.

This is where you can start building wealth instead of just surviving paycheck to paycheck. The second critical step happens before you even think about spending money on anything fun or optional. You need to make sure you're staying current on any debt payments you might have.

This isn't about paying off all your debt immediately, although that's certainly a worthy goal. This is about protecting your credit score and avoiding late fees that can destroy your financial progress. Your credit score is like your financial reputation.

And in our current economic system, that reputation affects almost everything. It determines what interest rate you'll pay on a mortgage, whether you can qualify for a decent car loan, and sometimes even whether you can rent an apartment or get certain jobs. Here's something that might surprise you about credit scores.

The difference between excellent credit management and terrible credit management often comes down to just one missed payment. If you make 99% of your payments on time, that's considered good. But if you drop to 97% on time payments, your credit score tanks dramatically.

Think about that for a second. In school, 97% would get you an A+. In credit scoring, it gets you labeled as a high-risk borrower.

The credit system is unforgiving, but the rules are simple. Make your minimum payments on time every time, and your credit score will take care of itself. This step isn't glamorous and it won't make you feel wealthy, but it's absolutely essential for long-term financial success.

Consider it the foundation that everything else gets built on top of. Now that we've covered the foundation, it's time to talk about something that most people completely ignore until it's too late. Building an emergency fund.

I know, I know. Emergency funds are about as exciting as watching paint dry in slow motion. But stick with me here because this might be the most important part of your entire financial strategy.

An emergency fund is exactly what it sounds like. It's money you set aside for when life decides to throw you a curveball. And trust me, life loves throwing curveballs.

Your car breaks down the day before your big presentation. your laptop dies right when you need it most. Um, your dog eats something expensive and needs emergency surgery, you know, Tuesday.

The goal is to have 3 to 6 months of your living expenses saved up in an account that you can access immediately, not invested in the stock market where it might lose value right when you need it most. Not locked up in some certificate of deposit where you can't touch it for 6 months. just sitting there in a boring savings account, ready to rescue you when everything goes wrong.

Let's go back to our earlier example. If someone's monthly necessities cost $2,700, their emergency fund should be somewhere between $8,000 and $16,000. That might sound like an impossible amount of money to save, especially if you're currently living paycheck to paycheck, but remember, you're not trying to save it all at once.

Here's the thing about uh emergency funds that nobody talks about. They're not just about the money. They're about peace of mind.

When you have three to six months of expenses sitting in your savings account, you sleep differently at night. You walk into work with more confidence because you know that if something happens to your job, you won't be eating ramen noodles and living in your car next month. But here's where most people mess this up completely.

They think their emergency fund needs to be earning amazing returns. So, they invest it in risky assets or lock it up in accounts they can't access quickly. Then, when an actual emergency happens, their money is either worth less than when they put it in or they can't get to it without paying penalties.

Your emergency fund should be liquid and boring. Put it in a high yield savings account that's insured by the government and call it a day. You're not trying to get rich off your emergency fund.

You're trying to stay financially stable when life gets chaotic. Once your emergency fund is established, you've officially graduated from financial survival mode to wealth-b buildinging mode. This is where things get interesting, and it's where most people start seeing real progress toward their financial goals.

Step four is where you start investing for your future self. And this is where the magic of compound interest begins to work in your favor. If your employer offers any kind of retirement plan with matching contributions, this should be your absolute first priority for investing.

Think about employer matching like this. You know, if your boss walked up to you every month and offered to give you free money in exchange for you putting some of your own money into a retirement account, you'd think they'd lost their mind, right? But that's literally what employer matching is.

It's it's free money that most people leave on the table because they don't understand how powerful it is. Let's say your company matches 3% of your salary and you make $60,000 per year. That means if you contribute $1,800 annually to your retirement account, your employer will also contribute $1,800.

You just doubled your money instantly. Show me another investment that guarantees a 100% return on day one. Beyond the employer match, you should aim to invest about 10% of your gross income for retirement.

This might sound like a lot, especially if you're just starting out, but remember, this money is working for you over decades. The earlier you start, the less you'll need to contribute each month to reach your retirement goals. Here's something that might blow your mind about retirement investing.

If someone starts investing $300 per month at age 25 and earns an average return of 8% annually, they'll have around $1 million by age 65. But if they wait until age 35 to start investing the same amount, they'll only have about $400,000 at retirement. That 10-year delay costs them around $600,000.

Time is literally money when it comes to investing. and every month you wait to start is money you're throwing away. But um here's what's really crazy about this step.

Um most people overthink it to the point where they never actually start investing. They spend months researching the perfect investment strategy, reading about different fund options and analyzing expense ratios like they're trying to solve world hunger. The truth is, for most people, a simple diversified index fund that tracks the overall stock market is perfectly adequate for building wealth over time.

You don't need to pick individual stocks, time the market, or outsmart professional investors. You just need to start investing consistently and let compound interest do the heavy lifting. Once you've got your retirement investing on autopilot, it's time to tackle any debt that's not your mortgage.

This is where things can get emotionally charged because debt often represents past mistakes or circumstances beyond our control. There are two main strategies for paying off debt and both of them work if you actually stick to them. The first is called the avalanche method where you pay off debts with the highest interest rates first.

Mathematically, this saves you the most money in interest payments over time. The second approach is the snowball method where you pay off your smallest debts first regardless of interest rates. This isn't the most financially optimal approach, but it can be incredibly motivating because you see debts disappearing quickly, which gives you momentum to keep going.

I personally prefer the snowball method because personal finance is more about psychology than mathematics. If paying off your smallest debt first keeps you motivated to continue the process, then that's the right strategy for you, even if it costs you a few extra dollars in interest. The key is picking one method and sticking with it until all your non-mortgage debt is gone.

Don't overthink it. Don't switch strategies halfway through. And definitely don't ignore your debt hoping it will magically disappear.

After you've handled your employer retirement match and you're making progress on debt payments, you can start exploring other investment options like opening your own retirement accounts or investing in taxable brokerage accounts. A Roth retirement account is particularly attractive because all your gains grow completely tax-free. You pay taxes on the money you contribute now, but when you retire and start withdrawing funds, you won't owe any taxes on the growth.

It's like planting a tree today and never having to pay taxes on the fruit it produces for the rest of your life. The contribution limits for these accounts change annually, but the concept remains the same. You're investing money that you've already paid taxes on, and in exchange, all future growth is yours to keep without sharing it with the government.

For your regular investment accounts outside of retirement plans, the tax situation is different. You'll pay capital gains taxes when you sell investments for a profit, but the tax rate depends on how long you held the investment. Hold it for more than a year and you'll qualify for lower long-term capital gains rates.

Hold it for less than a year and you'll pay regular income tax rates on any gains. This is why successful investors think long term. They're not trying to get rich quick by buying and selling stocks constantly.

They're building wealth slowly and steadily while minimizing the amount they pay in taxes along the way. The final step that ties everything together is probably the most important one and it's the step that separates people who actually build wealth from people who just talk about building wealth. You need to automate everything we just discussed.

Here's the thing about willpower. It's like a muscle that gets tired throughout the day. You might wake up Monday morning feeling motivated to manage your money perfectly, but by Thursday evening when you're tired from work and stressed about life, that motivation has completely evaporated.

You'll look at your bank account and think, "I'll just move money to savings next week when I have more energy. " Spoiler alert, next week you'll have even less energy. This is why automation is absolutely critical.

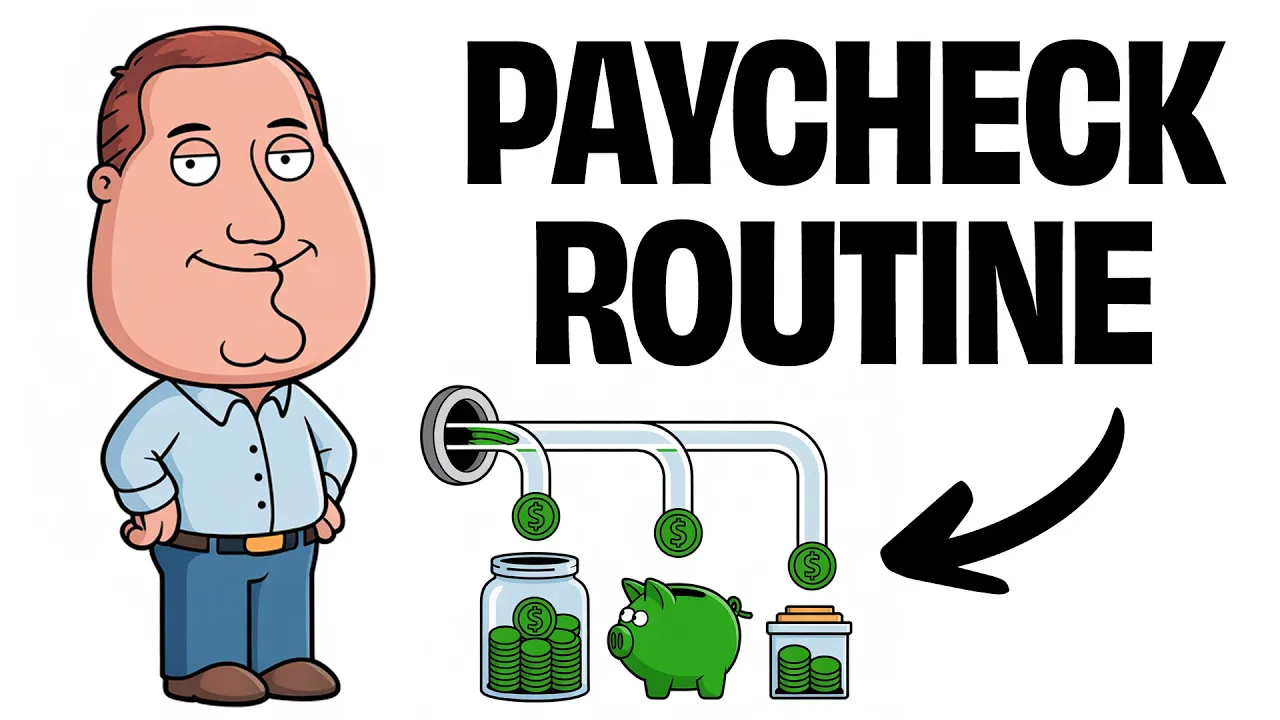

When your money moves automatically according to your plan, you remove human emotion and laziness from the equation entirely. Your money gets allocated properly whether you're having a good day or a terrible day, whether you're motivated or completely burned out. Here's how I personally handle automation.

And you can copy this system exactly if you want. When my paycheck hits my checking account, I let it sit there for exactly one day. Not because the money needs time to settle, but because I'm paranoid about timing and I want to make sure everything clears properly.

Then on the day after I get paid, automatic transfers happen like clockwork. A predetermined amount moves from my checking account to my savings account. From there, other automatic transfers move money to specific goals.

Maybe some goes to my emergency fund if I'm still building it up. Um, maybe some goes to my investment accounts. Maybe some goes to a separate account where I save money for taxes if I'm self-employed.

The beautiful thing about the system is that I never have to think about it. I never have to remember to move money around. I never have to fight the temptation to spend money that should be going toward my future.

It just happens automatically, like my rent payment or my phone bill. But here's where most people mess up automation completely. They set up all these automatic transfers and then forget to adjust them when their situation changes.

They get a raise at work, but keep saving the same dollar amount instead of increasing their savings rate. They pay off a debt, but forget to redirect that monthly payment toward investments. They're running on financial autopilot, but they never update their flight plan.

This paycheck routine isn't rocket science, but it works because most people never actually follow a system. Start treating your money like the wealth-b buildinging tool it is instead of monopoly money you found in your couch cushions. Automate everything.

Stick to the plan. And in 5 years, you'll be laughing at how simple it was while everyone else is still wondering where their money disappeared to.

![Rich Dad Poor Dad - Robert Kiyosaki [Complete Summary ]](https://img.youtube.com/vi/jFNdARDCrKA/mqdefault.jpg)