The US is overspending. >> The last time US debt was this much was during World War II when military spending hit record highs. >> It leads to there being deficits every year and not just in the bad years, which is wrong. This is not sustainable. >> He doesn't understand double entry bookkeeping. He's making mistakes which I can prove are mistakes using double entry bookkeeping. How does the Government create money? It creates money by spending more than it gets back in taxation. Now, if you say the government should never do that or should only do it

during a crisis period, you're saying the government should never create money. Welcome everybody. This is yet another video on money creation and this time round for trying to make this more accessible to people who haven't spent their lives buried in accounting as I've ended up Being. I'm invited along Nevi Yajwell and Nevie is a member of my school group. She told me that one of her reasons for being involved in my class is to understand the economy because she felt like she's being gas led by economists and she thinks this also has a major impact

on causing the stress she sees in particularly in American society which she talks about thirdderee burnout. >> Well, thank you so much Steve for having Me here. We do research at the nonprofit and as you pointed out we've also produced a documentary film called Thirdderee Burnout a survivor's guide. Now as part of surviving as human beings, we have to kind of like survive complexities like you know cost of inflation and uh you know the impact that it has on our mental health and pandemics and how they've impacted the economy and this everpresent discussion on the

debt crisis, >> right? And and so I happened to listen to Nile Ferguson um who's an acclaimed scholar on the history of money and you know you know him as well. We'd love to kind of like watch that together video >> and understand Nile's point of views and and also your perspective on what he seems to be saying about the debt crisis. >> Yeah, because from my point of view, he's Nile Ferguson said it's going to be A real crisis. The government's going to go bankrupt effectively. Just think this is not understanding how the monetary

system works and that's typical of people who call themselves experts on money. And of course, the tragedy is for non-experts like yourself. It's incredibly confusing. take a look what he has to say and then I'll go and pull it apart. >> But there's one other thing on economics and finance that I wonder if you know How it's ever going to get solved, which is why borrowing can be a really useful tool and it has been. But when you become addicted to it in the way that we have I mean we really are in trouble in

that aspect of things, are we not? >> Yes, deep trouble. If you borrow to invest and you acquire some productive asset, then what's not to like? It'll probably help you repay the debt. But if you borrow to consume, well, that way lies trouble. And that's what we've been Doing. The systems of public debt that evolved in the 20th century to finance wars, particularly the world wars after the 1945 uh allied victory began dra to transition to financing welfare. So we went from warfare to welfare states. It leads to there being deficits every year and not

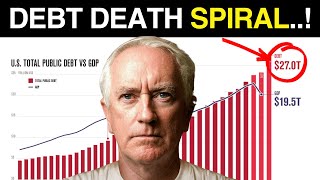

just in the bad years, which is wrong. the deficit every year in the US six plus percent of GDP every year as far as the I can see gross debt now above 120% of GDP higher than it was at The end of World War II this is not sustainable I said Ferrison's law states that any great power that spends more interest payments on its debt than on defense won't be great for much longer >> what's your reaction to that so far non-expert on the topic does he sound like he's making sense is it right to

cut back welfare >> well you know there's a big public health crisis there is obviously what they call a debt crisis. As a lay Person, when the media tells me that there is a crisis, then obviously my ears perk up and I'm find myself in an alarmist state. There is also uh the post pandemic, you know, economic situation that a lot of people and businesses are reeling with at this point in time. We have, you know, novel viruses floating around. There's the super flu that's going on at this point in time. Steve, I know you've

been struggling And uh and obviously then there is the climate crisis. >> So with all of these crisis put together, the meta crisis, the concept that you know my film deals with and on top of it when Nile's talking about for instance law and and and he's almost making it sound as though the elderly are a problem. >> They you've got to get rid of them honestly the elderly. Who who needs them? >> It does sound like that. And >> it does, doesn't it? Yeah. Yes. And it felt denigrating uh to a certain degree uh

you know and and also it sounded as though financing of wars and that financing second world war you know scenario financing or needing or having to finance the welfare state creating a drag. I mean all of this feels like first of all not in the interest of humanity. >> Second of all it doesn't feel logical to Me. Third of all, it also seems to put conflict on a higher pedestal or financing conflict on a higher pedestal versus doing things that are in in interest of, you know, public good. So, I'm a little confused, you know,

and dare I say more than confused. >> The person that responsible for that confusion is Nile Ferguson. Okay? Not because he's uniquely wrong. He's repeating the same stuff that virtually everybody says about the dangers of Government debt. Imag maybe at one point he said deficit every every year rather than just bad years which is bad. So he's saying running a deficit when the the economy is in like a what you might call a noncrisis state that's bad. You should only run deficits during crisis is part of what he's saying. And he's also saying that because

we we set the funding levels for the government was set up after World War II and for some strange reason we wanted to make people Feel healthy after World War II. with welfare you had insurer we had public health we had p state pensions and now because there are so many old people we can't afford them anymore so we've got to increase the retirement age we've got to reduce health cover etc etc all this stuff is the conventional wisdom on money creation and it's all coming out of the fact that despite the fact that Ferguson

is an expert on the history of money I prefer other the historians to Him but he's a scholar on that topic he doesn't understand double entry bookkeeping he's making mistakes which I can prove are mistakes using double entry bookkeeping. So that's why I want to build this with you and show you how you can see the actual dynamics of money creation. Ferguson doesn't realize it. All the people who panic about government deficit spending don't realize it. But a deficit is actually necessary to create government money. If You're going to have a system with money in

it where the government created that money, then the government has to run a deficit. Okay? And so I want to show that but working from first principles now of double entry bookkeeping. >> What is Revel? What is this? >> It's it's a software package for analyzing financial dynamics that it does both modeling of monetary transactions, dynamic processes in general and that it can also analyze Data. So a combination but the the main thing which is which is necessary now is to use it to explain how money is created and that comes down to understanding double

entry bookkeeping. So what Revel does is enable you to to create an in integrated look at a financial system using double entry bookkeeping. The concept they worked out is that every transaction has two parties. So you have to show two entries on every line if we're going from one One person's account to another person's account and you've got to show it in two perspectives. You got to show it from the the buyer and the seller or the borrower and the lender and so on and so forth. So everything turns up twice on each line and

has to be shown a minimum of four times before you've got a complete picture of how it sets up in the economy. So what Rabbel does is create these things we call godly tables. You describe all claims that People have on each other as either assets or liabilities. A financial asset is your claim on somebody else. Okay? A financial liability is somebody else's claim on you. The gap between the two is your financial net worth or financial equity. And so that's the starting point. And because every financial asset is a claim on somebody else, every

financial liability is somebody else's claim on somebody else. The sum of all financial assets and liabilities is Zero. Very important conservation law. There are other things which I we call non-financial assets and they're things like, you know, if you own your home, that's your asset and nobody else's liability. You might have a mortgage attached to the house, but it's still something you own outright. That's your asset, nobody else's liability. They're different and they sum to being worth more than more than zero obviously, but financial assets sum to zero. What we're Talking about with money creation,

we're just talking about financial assets. That's what I want to now explain. >> And I just have a quick question um around, you know, ownership and and we know that, you know, human beings have um employed other living beings on the planet, you know, to serve uh our needs and and things like that as well. So >> slavery. Yeah. >> Yes. So one obviously from a geopolitical and a historical situation Is slavery was sanctioned by you know certain European states. We know that was part of you know sanctioned state policy. But really what I want

to talk about is when we discuss you know animals that are owned by humans. >> So and the popular term for that is livestock. How are they treated? How is >> the livestock are also a non-financial asset because if you own you know a cow or a sheep or whatever else legally speaking it's your asset and it's nobody Else's liability. So anything that produces output in fact for anything physical pretty much is a non-financial asset. So when you look at all the arguments made about the government running out of money and all this sort of

discussion it's all about financial assets. What I'm going to do here is show buildup models showing the actual dynamics of financial assets. I don't need to bring in non-financial assets to show where this perspective is wrong. It's wrong in terms of financial assets only. So if I build a model just of the financial system, I can explain why Ferguson and virtually everybody else except Richard Murphy and me are wrong on how this system works. Okay. >> Okay. So, so just to sort of summarize and especially for my viewers as well, when we're talking about the

debt crisis, when we hear about the debt crisis and all of these, you know, alarmist videos or on, you know, popular Newsrooms and and so on, literally, we're only talking about financial assets. We're not talking about the non-financial assets um including livestock or animals that are historically used and currently being used and abused and exploited for humanity. >> Now, we've got to classify financial claims as either assets or liabilities. And what I've got here is the large window for the banking sector. Private Debt is an asset of the banking sector. So I put debt as

an asset there. And it also has deposits, our assets, and their liability. So I put debt and deposits there together. I'll just go back down now to the overall view here where I see all four tables at once. What we've got is I've got debt as an asset of the banking sector and deposits as a liability of the banking sector. Okay. Now what that means is debt being an asset of the banking sector is a Liability of the people who borrow from banks and I'm lumping households and firms together and calling them the basically the

non-bank private sector. So this little wedge here, if I click on this little wedge that goes looking for any asset that hasn't yet been recorded as somebody's liability. So I click there and it's going to show me debt. And I put debt in the side there and now I've got debt turning up. Asset of the bank, liability to the borrowers. And We've got deposits which are liability to the bank. They're an asset of the borrowers. So that's that's the basic starting point those two. Okay. So any financial asset as a financial liability. Any transaction has

to be shown a minimum of four times to be able to show the complete thing from the point of view of both one agent and the other agent in the whole system. Now what I've got here is also initial conditions and this is a very Mathematical thing and mathematicians use initial conditions to model dynamic processes. But what they means here is the amount of money at a particular point in time in all of these accounts. So if I say for example there's debt of 100 and deposits of 90 and that could be in millions or

billions of dollars or whatever currency you're working in then the bank is going to have net worth of 10 coming out of that. And this is because as I said your net financial Worth is the gap between your financial assets and your financial liabilities. Okay? So I've got assets worth 100 liabilities worth 90. Therefore the equity of the bank is 10. Okay. Now look what happens down here for the private system. They've got assets of 90 and liabilities of 100. They're minus 10. >> Yeah. >> Okay. Now that's absolutely unavoidable because the fact that all

financial assets and liabilities sum to zero. Then If one part of society has positive equity, the rest of society has got identical negative equity to the same magnitude. And that's going to become very important in explaining why we actually have government spending in the first place when it's greater than taxation. So that's the starting point. Now add operation for bank lending for example then what bank lending does is put an amount of money in people's deposit accounts and exactly the same Amount in their debt. So if I call this loans to indicate it's new loans

being made by the banks. Initially what Rabble is doing is saying well you've got one entry and you need to have two and those two entries have to be such that assets minus liabilities minus equity equals zero. That's not yet the case. So the bank will put money in your bank account if you agreed as them you're saying oh we I now owe you exactly that same amount of money. So type loans over here You're now seeing this from the point of view of both the bank and the the borrowers. The asset of debt rises

liability rises. So there's no change to the overall worth of the banking sector from those operations. Same thing for the households but the other way around. Okay. So that's the starting point but finish with here in terms of the private sector before I go on to build an actual model. The private sector starts in negative equity and it'll stay there if There's only private money creation. It's like a seesaw because the sum of all financial assets and liabilities is zero. Then you got you're on a seessaw and if one side is up the other is

down. >> Yes. >> Okay. Okay. Well, the bank has to be up by by 10 here. So, the private sector is down by minus 10. That's an absolute given. You can't get away from it. So, that's that's the situation for private money creation. What about when you Include taxation, for example? And I'll just going to now make space to include taxation here. So, I'm going to have taxation as an operation that happens through bank accounts. And what happens with taxation is that the government takes tax dollars per year out of your bank account. Okay? So

I've now got minus tax turning up there. Now I now need to make two entries to balance that row. Where does the tax revenue go? Initially it goes into the accounts we Call reserves. The reserves are fundamentally the accounts that private banks have at the central bank. So now if deposits go down the matching up entry for reserves is the same entry minus tax. And now that's properly balanced between the two. What does that mean? If you've paid tax, your bank account's gone down. >> You don't you don't get any compensating increase in anything else.

So your your final equity has been reduced. Okay. So To balance this, I need a minus tax in the equity column here. So taxation reduces your financial net worth. >> Yes. >> Okay. >> It does. Sadly, >> everybody knows that. This is something everybody's conscious of it. You've got to see the double entry to realize what this means in terms of what does government spending do. I've now got to show that reserves are a liability to The central bank. So if I click on this down arrow here, there's the wedges. The wedges go looking for

incomplete recording of financial transactions. So I've got minus tax there. Now the question is who gets the tax? The money goes to the treasury. So I've now got to include another liability at the central bank which is the government has accounts there, lots of accounts. What the taxation does is increase the value of those accounts. So now I've got the Government having that extra amount of money and now I've got the government account there as a liability to the central bank. I've got to show it as somebody's asset. Of course, it's an asset of the

treasury. So I click here and that operation comes across. Now the government's got tax money. Is there any offsetting liability for the government in that? No. So the tax taxation increases the net worth of the government. And this is something which People are aware of it but they don't let their minds get around it. Obviously taxation reduces increases the net worth of the government and reduces the net worth of the non-government sector. So spending must do exactly the opposite >> logically. >> Okay. So now what I'm going to do is include government spending. So we've

got taxation up there. So I'm going to have government spending and that is going to be that's going to be a Negative for the government's account here because it's going to come out of the government's account to do it. So we need a minus spend and I'm going to put a subscript G. So it's indicating government spending rather than spending by banks for example. And that reduces the government account. Where does it go? It goes into reserves. So that is a negative for the treasuries account and a positive reserves. Now again this is is going

to be a minus spend by the Government here that goes through reserves. So reserves are going to be affected at the level of the banking system as well. So of government spending and that is therefore going to be an increase in reserves and that turns up as an increase in deposits because that's where the money gets put and then if you look at it from the point of view of the what happens for the non-government sectors of the economy government spending is Increasing the amount of money in deposit accounts and therefore it's increasing the net

worth of the private sector. Government spending increases the financial net worth of the private sector and it reduces as it happens the worth of the government. So you take a look at this the color and the signs here. Taxation reduces the net worth of the private sector. Spending increases it. The opposite applies at the government level. Taxation increases the Net worth of the government. Spending reduces it. Okay. So if the government >> when you say the private sector you mean the industry as well as individuals. >> Yeah. Indiv ind basically industry and households. industry and

households. >> Yeah. Okay. So now we've got the outcome if the government spends more than it takes back in taxation. It creates money. It doesn't there's no borrowing on this system at all at the moment. I've got debt for the private sector, But I've got no borrowing for the government sector. So just by the act of spending more than it takes back in taxation. Government creates money that turns up into people's deposit accounts. It increases the net worth of the non-government sector, but it does it by the government going into negative equity. government has had

to create the money to be able to flood it into the private sector >> fundamentally. Yeah. Modern days this is Used to buy aircraft carriers and nonsense like that. But welfare equally welfare spending is going to increase the financial net worth of the private sector but push the government sector into negative financial equity. And people often go, "Oh, it's terrible the government's in debt." Okay. Okay. Terrible that it creates liabilities for itself. But the thing is if you think about it currency of a particular country where that currency is accepted Defines the boundaries of the

country in the same way that having customs agents and you know military and so on says where your border is where your government liabilities are accepted as money in in private transactions that's where your government reigns. So the government needs to create liabilities for itself effectively to create a financial system for its overall economy. So, it's not a bad thing that the government runs a deficit. And this Is why one of the first reasons why Ferguson and all the mainstream thinkers are wrong because they're thinking that the government should only run a deficit during bad

times. Well, that translates to saying the government should only create money during bad times. During good times, it should create no money at all. >> We're fighting and, you know, advocating for welfare. We're advocating for, you know, potentially universal health care System. We're uh advocating for the government spending in all of these things that are in the interest of both public good as well as uh in the interest of planetary health. >> What Nile Ferguson seems to be saying is that the only time government should be spending is when there is conflict and when there

is a negative situation. Now does that negative situation only described as a war situation or is it also in case of a crisis such as you Know the 2008 crisis you know where there is a recessionary situation and and is he also advocating for uh bettering the status and the situation of the public and the private sector by government spending. Does that extend over to that kind of goodwill? >> It does but it's all based on a fallacy. Fallacy is the government has to borrow before it spends. This is the belief the government has to

borrow money to be able to spend. By starting by absolutely From first principles, I've got no borrowing by the government in this system. It's the government deciding to create negative equity for itself by spending more than it gets back in taxation which actually creates money. And then the question is what sort of economy do we live in? Do we live in a pure private sector economy or do we live in a mixed sector economy where there's both private money creation and government money creation? And we can See that the private sector creates money by creating

loans. Okay? How does the government create money? It creates money by spending more than it gets back in taxation. Now, if you say the government should never do that or should only do it during a crisis period, you're saying the government should never create money. >> Okay? So, he's getting confused. And this is why I've left that out, government debt out of the model so far. Getting confused by believing that the government when it when it runs a deficit is funding it by going into debt. No, it's not. It funders by going to negative financial

equity which creates money in the form of extra deposit accounts here. If spending exceeds taxation, then government accounts deposit accounts have increased. >> Again, just for clarity, deficit does not equal debt. >> No, no. Deficit is I I call it fiat. Okay. A better a better word would be fiat because this is how a government creates money. The whole idea of by fiat is by basically proclamation. Okay. Okay. So the way that you create money by proclamation in a modern capitalist economy with with the government sector is the government spends more than it takes back

on taxation. If it doesn't do that, it doesn't create fiat money in the very first place. >> Okay. >> Okay. So now let's look at what that can mean for the private sector. Then I'll bring in debt in a moment. So if you look at the situation that the government that the private sector is in here, negative financial equity, okay, if you want to have the private sector having more financial assets than it has financial liabilities, the only way that can happen is the government spending exceeds taxation. >> Mhm. >> Okay. So it's the requirement

if you want the private sector to to have financial net financial assets, financial assets greater than its financial liabilities, the government must spend more than it takes back in taxation. Okay. So this reverses all the thinking you get out of people like Ferguson and mainstream economic textbooks and all the political parties, conventional political parties and so On. >> Yeah. So so meaning that government spending is essential for the greater public good. >> Yeah. Uh and then there's a there's a whole lot of reasons for that as well. I mean you if if RIP Murdoch gets

sick, he can buy the hospital in which he gets operated upon. Okay. If you and I get sick, we can't afford it. Okay. uh you know incomes don't give us sufficient to cover you know like a serious cancer Operation or that sort of thing. So we have two choices. We die okay or the government spends to enable public health. And what we got after World War II travesty of the Great Depression and World War II was such a shock to the body politic that countries around the world England being one of the main ones to

lead off with it but also America started introducing welfare. You had unemployment benefits which didn't exist before the great depression. public Health, public education, etc., etc. So that's providing services that the whole society needs. You you can't run a factory with dead workers. Okay? You you actually want people to be healthy. And therefore, it isn't just the the the poor who benefit from this. It means that capitalists get a healthy workforce. Uh people don't have to take time off for medical problems because they've been addressed by public health and so on. They don't they're not

stupid Because they've been taught in public schools. They can't afford the schools but we educate them. They can therefore work in the factories. They can follow instructions. So all this stuff is necessary for a well functioning system. But the obsession with eliminating government debt means they say we can't not produce the weapons. We can't not make the guns and the ships and but we can stop giving the poor public health. We can stop giving them public Education. So again, in simpler words, it's just a matter of prioritization because they've got the fundamentals wrong and they

believe that the deficit equals debt and they're uh so fearful of debt that they want to minimize it and and it's sort of >> filtered in, you know, down to public opinion so that that even the public votes Yeah. >> and engages in the with the voting system and so on and responds favorably To somebody who says, "I'm going to reduce government debt." >> Yeah. And and the way in which they're choosing to reduce the government debt is not necessarily through public sector uh you know public health reform or healthcare reform or education reform but

really to focus on issues of national security. >> They they cut they cut they cut spending on all those things. >> They cut spending on all of those things >> and they keep the spending on the on on warfare. You know >> exactly and this is exactly what we're seeing at this point in time in the United States. >> And none of it's necessary. It's all a mistake starting from not understanding double entry bookkeeping. And Ferguson is as guilty as that of all the rest of the commentators. As I said, it's a bit of a

joke in some ways, but it's almost true. The only people on the planet who Understand double entry bookkeeping in the context of the economy are myself and Richard Murphy. So when you do it, that's why I'm doing right from the very basics. I haven't even discussed government bonds yet because let's just take a look at the system now and see what is one of the impacts of if the government spends more than it takes back in taxation then what does that do for various parts of the system? Well, down here it creates more deposit Accounts.

So the amount of money the private sector has is increased by the government spending more than it takes back in taxation. So they come out ahead. It doesn't affect the banks at all because taxation reduces reserves. spending increases it. Effectively, if government spending exceeds taxation, then the assets and the liabilities of the banking sector expand. It gets bigger, but there's no change in the net worth of the banking sector. For the Central bank, same sort of story applies that taxation reduces reserves and spending increases it. What happens over here? If your spending exceeds taxation, reserves

are going to rise. Okay? So reserves will rise for the banking sector and rise as a liability to the central bank as well. What happens if taxation if spending always exceeds taxation for the government account at the central bank? If this spending exceeds taxation, this is going to go Negative. If the government spends more than it takes back in taxation and doesn't issue bonds, it will have a overdraft at the central bank. So let's bring in bond sales. But I'm going to sell the bonds to the central bank. Want to show that first of all

because at the moment it's legally most countries have passed laws saying the Treasury cannot sell bonds directly to the central bank. That's just a law written by lawmakers virtually everything else wrong and They've got this one wrong as well. So I want to show there's no problem with the government having an over overdraft at the central bank. Okay, you and I if you and I have an overdraft, we've got to pay a penalty rate of interest on it. Okay. If the Treasury has an overdraft at the central bank, effectively the Treasury owns the central bank.

>> Yeah. >> So, it can it can allow itself to go into negative balance in the Treasury Account there. It doesn't pay any interest at all. So, there's no penalty. >> There's no penalty. It's very different to you and me. I've had overdrafts on occasions and you pay a high rate of interest, you know, and you don't get rid of it till you reduce the overdraft to zero. Okay. That's the situation for a private individual. But the government owns the central bank. Okay. Yeah. it doesn't pay interest on any bonds that it sells to the

central bank. So I could Bring in bond sales here by the treasury to the central bank and that would get rid of the problem because in that situation the problem is that it looks bad for the government to have an overdraft at the central bank. But if the government issues, if the treasury issues bonds and sells those bonds to the central bank, then the assets of the central bank rise, the liabilities rise at the same time, but you don't get a negative in that account. So I'll now Just add that in here. Have the treasury

bond bond sales to central bank. Then what that would mean is the government's now got a new liability and I'll call this bonds that are owned by the central bank. just use CB initials bond bonds subscript CB for the central bank. So that's going to mean that there's CB bond. So if the central bank buys bonds that means that the liability that the treasury has the central bank rises but of course that puts money in the account Of the treasury. So now we got that at the level of the treasury. What does that do at

the level of the central bank means that the government account rises by that amount? See that increases the liability it has, but it also increases the bonds that are owned by the central bank. So now you've got this new situation if those some bonds are sold to the central bank. There's no an inflow of funds into the government account. So if this inflow equals the Gap between spending and taxation, the government account doesn't go into overdraft. So we can actually have it all done at that level. There's no reason to sell the bonds to the

private banks. It's just the law that forces us to do that and then it makes it look like we're borrowing from financial sector which is not the case. >> Um so Steve C could you throw some light on why was that law created in the first place >> because >> was there a reason >> it it it can it can relate back to preloading currency period when the government was effectively said that it was going to enable money to be converted into gold for example. >> Mhm. >> Okay. And and this is the stuff that

Ferguson covers quite reasonably when he's talking about all the wars in Europe, Holionic Wars and the 30-year War and the 100redyear war and all that sort of thing. What the government was doing back then was hiring mercenaries. Most of the time a lot they had their own armies as well but large numbers of mercenaries and particularly during the 30 years war and the hundred years war. If the king tried to pay the mercenaries in his own coin the mercies say sorry hope you win but you might not. If I if you lose and I survive,

I want to be able to go shopping on the other side. So I insist on being paid in gold or silver. Okay? So those walls in those days, you had to have gold or silver to pay the mercenaries and therefore you had to issue bonds to get people to give you the money and then you could buy the gold and so on. So bonds were in that sense they were an essential part of the preflating exchange rate, pre- nonwarfair stage, relatively non-warfare stage of European history. So we've then made the mistake of thinking that what

Happened back under those days which is the time when Ferguson knows what he's talking about applying it's now and it's a different system. >> Yeah. >> It's anacronistic in that sense. >> It's anacronistic and the anacronism is what we're torturing ourselves with and causing some of the stress you know you focus on in your work. That's the the situation that could apply. Now instead what does apply is that the you have the The bond auctions where the government does sells bonds to the uh private bank. So if I have uh bond auctions here the primary

auction that that happens with the the government. The government sells bonds to the banks. So we have bonds which are owned by the banks down here. And the way that these are financed for is you have the to actually take place in this you've got to have an account at the central bank cuz the central bank handles the auction. So you're going to Have uh let's say auction dollars per year will come out of reserve accounts. So the reserves fall by that amount and the monetary value of bonds rises by that amount and those bonds

are a liability of the treasury. There's bonds B. So now I've got the o overall picture of the modern system as well as what could could apply and if you take a look at what happens in terms of the the auction is that using money is the government borrowing money when it sells Those bonds. Well money is fundamentally the sum of the deposit accounts plus the short-term equity of the banking sector. Nothing has happened over here. >> Yeah. >> Okay. What the auction does is convert the asset that backs the money created by deficit spending

by the by government spending more than it takes back in taxation. It converts it from reserves that used not to earn any interest for banks before the global financial Crisis. So this is where the interesting comes in now. The interest only turns up because we don't do what we could do which is sell the bonds to the central bank. Okay? It's it's not a necessity. If you're really panicking about government debt, there's a simple solution. Let the central bank buy every last bloody bond in existence. Okay? And they could they could do the whole lot.

They could do the whole lot. If you want to get rid of if you're terrified about Government debt, tell your central bank to buy all bonds tomorrow. >> And then what would happen? Those interest payments would go from 6% of GDP to zero. >> Yeah. >> Okay. So, that's not a problem you and I can solve. You know, if you if you end up in financial difficulties with your loans, your husband can't go and buy the loans instead and therefore stop you paying interest. Okay. >> Yeah. The government can do that. >> The government can

do it. It's it's again, you've got to realize and you do. Um but the conventional economists do not and Ferguson doesn't and all the journalists and politicians don't. The different sectors have different relationships to what we call debt. In the private sector, if you borrow money, you're in debt to a bank. You've got to earn the money yourself by the turnover of goods and services, your not profit, My my course and all that sort of jazz to be able to pay uh the interest on that debt. And if you can't do it, you go bankrupt.

But the government could literally get rid of all its debt obligations tomorrow by telling the central bank to buy all outstanding bonds and then it could do it and that would be the end of the problem. They don't even talk about that. Now, that's that's a feasible solution. Okay. You know, it's really interesting because Neil Ferguson and and economists like him, they do talk about the economic system as fundamentally resilient and selfcorrecting. >> Yeah. >> But they don't seem to have this apparently quite simple solution to the debt crisis. >> I know. I know. It

just shows how much they're locked into a mindset which is false. Okay. Because once you look at The set of the accounting up this way and this is what happened during quantitative easing it could look the central bank can literally buy all outstanding bonds tomorrow if it wanted to. Now it did that during QE that affected the amount of money in circulation when they bought those bonds off the private sector the non-banks. Okay. When they buy it off the banks it doesn't affect the money supply at all. So all these things are things you only

Understand if you see the double entry bookkeeping and because you know so-called experts like Ferguson the entire economics profession outside postcanesians and MMTs uh all get this wrong and then we get our knickers in a twist to take an Australian expression then panic about the you know terrible level of debt we're all going to be ruined. If you really think so then get the central bank to buy all the bonds tomorrow and The problem's gone. What's your next problem? Okay, so that's that's the situation. And what I'll do just very quickly, I haven't tried to

model this yet. This is just laying out the double entry bookkeeping, but I can actually build a model and show what happens. And one of the most important points that I'll get to is the one I I made a comment about beforehand. The only way you can get the private sector out of negative financial equity is for the Government to spend more than it takes back in taxation. >> Yep. So that makes a strong argument in favor of running a deficit to create fiat money, which then means households have got more financial assets than they

have financial liabilities. And that's going to mean that households are less likely to panic about being a negative financial equity. And when you do panic about it in the real world, what you do is you think, "Oh god, look, our debts Exceed our liabilities. How can we get out of this?" I know. let's borrow some money from the bank and buy some non-financial assets, buy some shares, buy a second home, uh you know, rent the place out, become a landlord, etc., etc. That's what attracts us into financial bubbles. The real weakness here is that if

you don't have the government creating sufficient money to put the non-bank financial sector into positive financial equity, they're likely to Panic about the fact that they're negative and go and speculate and gamble on share prices or house prices and you'll get a share market bubble like the 1920s or a house price bubble like the 2007s and the the subprime bubble. This ends up with crazy behavior. >> Yeah. Yeah. Absolutely. You know, because consumers don't know. Also consumer spendy go spending goes arai right and then people usually end up thinking really in a in a basic

kind of A way that you know maybe I can try my luck in the share market maybe I can lock money in real estate because after all real estate never failed anyone never even after 2007 in America yeah it's amazing how fast we forget >> we we forget it and obviously now with the climate emergency ever increasing we know that you know homes cannot be insured anymore more um you know there could be a hurricane tomorrow, there could be a wildfire out in California And the housing bubble is experiencing yet another layer of uh uncertainty

at this point in time. >> Yeah. >> Um so so let's model it out. I I'd love to see how all of this turns into the model and what's the impact. >> Okay. Well, that's going to take a while. So let's bring up the bank bank table here and I'm going to make space for interest payments. And what that means is uh to pay the interest you've Got to have interest coming out of your deposit account here and it goes to the banks. So that now means there's money turning up in the bank's accounts. Equally

of course the banks spend. They spend very slowly but you're going to have bank spending which is going to be money coming out of and of course that turns up as an entry in deposit accounts. So now when you look over here interest payments on debt reduce the the worth of the financial net worth of the Borrowers. So that falls down there. And then I've got government spending again or both spending by banks rather that's down here. So this is bank spending and that means that you have spend_b dollars turning up in uh private bank

accounts and that increases the equity of the um non-bank public. Copy the stock variables and copy the flow variables. So now what I've got is I've got deposits here and I want to have accounts as well. So, I take a copy of Those stock variables, too. And so, I've got deposits plus what's in the bank's short-term equity. That's the money supply. So, what I can do is say, let's add those two together and call that money and then have a very simple argument that the velocity of the money turns over so many times per year,

which is a velocity of money. So, I call this call this velocity here. Give it a say a value of two. So, money turns over twice per year. maximum of say three 50% turns Over in a year. And now if I multiply velocity by money, I've got a monetary model of GDP being created here. So loans are going to be some fraction of GDP. So money of 100 times velocity of two gives you a GDP of 200 per year. Loans are currently zero. But if I make them say 1% of GDP, the loans are two

million or two billion dollars per year etc etc. So you can simulate that and see what happens. taxation and government spending being a fraction of GDP. So here we have tax and spend. I take a copy of GDP and then have it well the same sort of thing I've done here. I'll call this tax frack. I won't bother adding the GDP component to it. So make this a fraction. Make it a parameter. Let's say the initial value is 20% of GDP. A maximum tax fraction of 50% minimum say 10%. And then a step size of

1%. So now I can if I now multiply tax frack by GDP then I get tax that way. So tax starts at 40 and then I'm going to Do the same thing have spend frack give it the same values as tax frack. So started at 20% maximum of say 50% minimum 10% step size of 1%. And then if you multiply spend frack by GDP you get spending. So let's put those two together. Okay. So, I've now got loans and taxation and spending all all covered. And what I want to I mean I haven't got interest

or um bank spending defined there, but I think that's probably enough to give a simulate the System as it stands, >> is it? >> To show the main point about what government spending does to the equity of the private sector. So, let's just now bring a chart down. And what I'm going to graph here are the equity positions of the treasury and of the private sector. So I've got treasury there. I'll take a copy of treasury. That's the net worth of the government. And then I want the net worth of the Worth of the private

sector which is private up here. So that's over here. And then we're going to have the net worth of the banks as well. And there's banks. So take a copy of that. And now let's actually graph each of them. So net worth of the banks, net worth of the private sector, net worth of the treasury. This is going to be net equity and this is the years down here and this is now dollars if we're working in terms of dollar currency and put a legend on There. Okay. So now uh I'm now going to take

a copy of loan frack tax frack and spend frack and use those as controls. What I want to look at is what's the financial situation of the non-bank sector uh with and without taxation. So we run it first of all and you see that the treasury's got zero equity. Uh the banks have got 10 and the non-banks have got minus 10. If we increase the loan fraction, you don't do anything to change it. I haven't got interest Payments in there yet. So it's not going to affect that. What if the government spends more than it

takes back in taxation? Notice. Okay. instantly because the government spend the treasury's gone into negative equity and the private sector and the banks are both in positive equity. >> Yeah. >> Okay. So unless you have government spending the government is not spending more than it takes back in taxation or If it tries to run a surplus it pushes the private sector to negative equity. So your real guide should be you want the private sector to be in positive equity. The only way to do that is for the government to run a deficit. >> Yeah. >>

Okay. So it's the opposite. All right. So that's absolute basics. We got much more to do to finish the whole argument. But as you can see, when you put the accounting together, you get a Completely different answer about what's a good idea for government to do than if you put up with the so-called experts who like Neil Ferguson is either Ferguson probably takes seriously what he gets told by economists because he's a historian. >> Yeah. >> He doesn't know any better in that sense. Economists do everything using supply and demand curves, you know, intersecting lines.

They don't do the Accounting. They think they understand the accounting, but they're wrong. And so that's why we we get all this politics based on the wrong idea that says the government shouldn't run a deficit at all. And that therefore means the government shouldn't create fiat money, which means we get stuck in a world just with credit money, which means the private sector has financial liabilities that exceed its financial assets, which leads to all the Speculative behavior we saw in the 19th century and uh the 1920s and also the subprime crisis. >> Yeah. and and

you know thank you first of all Steve for you know explaining the basics because a lot of the times you know as as adults who've since graduated from high school a long time ago >> somebody has advanced education in economics but ended up with you know what's the dominant paradigm of economics which is neocclassical at this Point in time you get caught up in in the theory of what we're taught but when we go out in the real world it's all based on all of these dynamic situations and and human erratic behavior and speculative behavior

happening all over the same you know time leading to you know as consumers being confused. >> Yeah. >> Uh left alone to do whatever it is with our basic understanding to do and and secondarily an entire financial system An entire monetary policy fiscal policy of the government like the entire government functioning on fundamentals that don't even apply anymore. That's right. What I hear you say and and educate people about is that this silo behavior where the economists aren't talking to accountants, aren't talking to historians, aren't talking to politicians, aren't talking to maybe consumer behavior marketeers

like myself. That's right. You know, because I know from the four Ps of marketing that price is definitely a dynamic, you know, criteria. It's not something that is fixed. And I remember that we were talking about it yesterday in in the course uh where sometimes price is just held as a as as a fixed you know thought of as a fixed variable but marketers don't think of it that way. So imagine all of this interdisiplinary thinking to happen so that we have solutions for society as a whole versus this entire Elephant that doesn't know the

trunk from the tail. >> Absolutely. And we're stuck in that world of, you know, partial understandings of everything. And our policy makers are making it worse by believing they've got to cut back on government spending when in fact they're cutting back on government money creation. And that means the private sector actually grows less rapidly and gets more caught up in unproductive Speculative behavior rather than the productive investment behavior we'd like to see. >> Yeah, absolutely. when the consumer confidence goes down that, you know, we we see mental health issues around financial insecurity and it all

leads to, you know, a subject that I talk so much about, you know, in in my nonprofit and all the work that I do is around burnout >> and and I guess that economists like you Burn out anyway because you're sort of shouting about all of these solutions from the rooftop and you know, nobody seems to >> Richard and I get burned out. The rest of them are actually perpetuating these myths. Not all of them. And modern monetary theory is correct about government money creation. Postcanesians are correct about private credit money creation. Uh we do

have the potential to understand the system properly. But it Means abandoning the neocclassical way of thinking about everything. And this is why I say neocclassical economics is actually bad for the health of capitalism. >> Yeah. And and bad for the health of the planet and and for the people that live on it. >> Absolutely. >> Yeah. Professor Keem, thank you so much for sharing your thoughts on this. I think that this has been super valuable. Is there any other last words that you'd like to leave our viewers with? >> No, I think we'll leave it

at that. We'll have to obviously elaborate, but hopefully it's a good useful guide for people as why they shouldn't take mainstream economists or Nile Ferguson on money seriously. >> Thank you so much for the question. If this helped you to see that the equations economists use were wrong and not you, you're probably like the 22,000 Others who recently requested one of my three books inside my new Rebel Economist book bundle. The bundle is worth $50, but you can get it while it's free this week. Click the link in the description or go to steveken.com. Once

there, click on the black button, enter your email, and in about 60 seconds, we'll email you free access. After that, if you want to study with me personally with live lectures each week and use the proprietary tool you saw me use in this Video called Revel, there'll be an optional invite to apply and join my private group of like-minded economic rebels. Again, that's stavekane.com or click the link in the description.