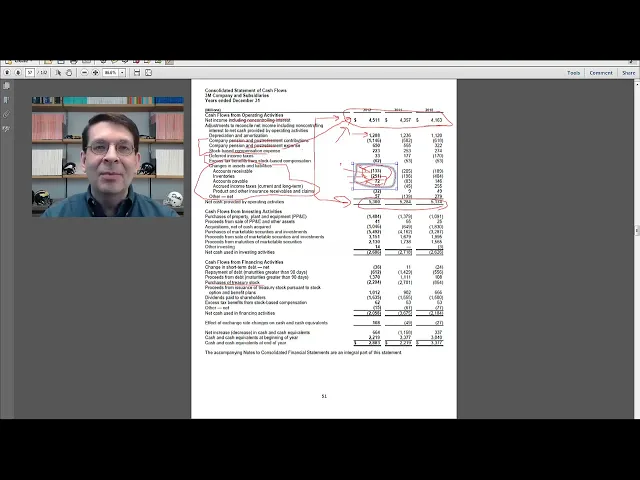

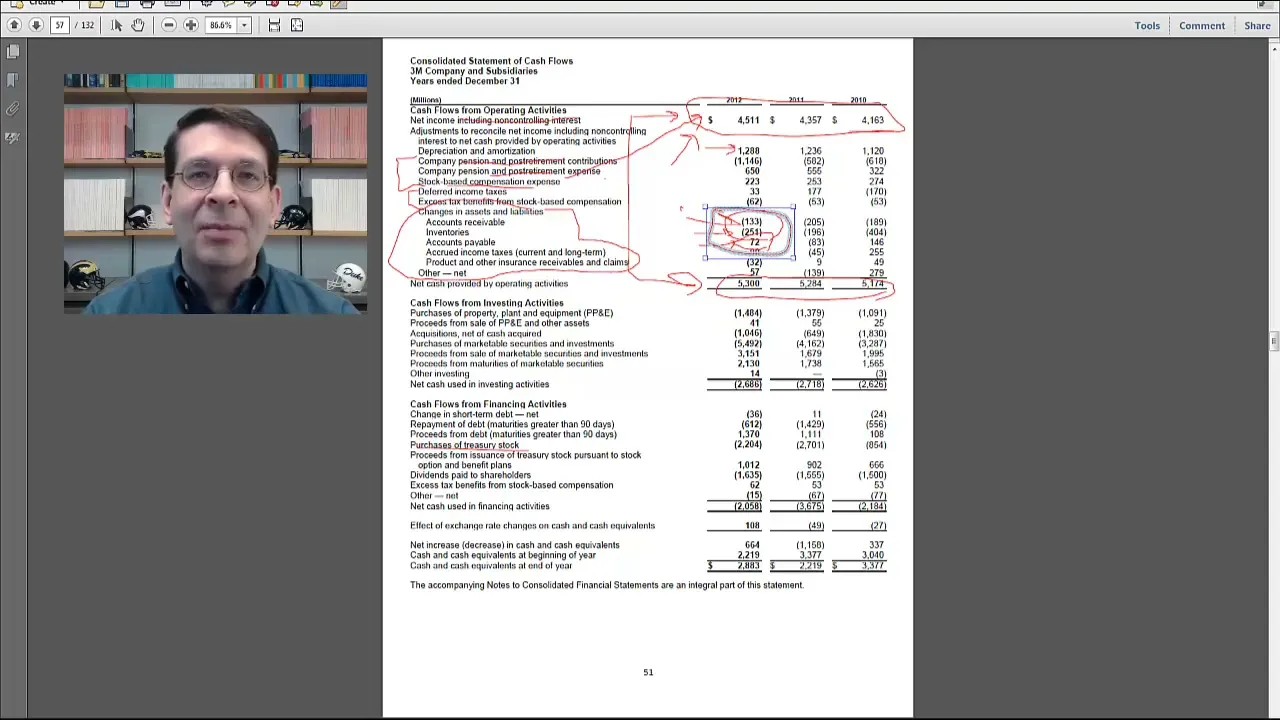

hello I'm Professor Brian Bay welcome back in this video we're going to end our week looking at cash flows with a look at the 3M company's cash flow statement we're going to take a look at their actual statement plus the supplemental disclosures about the statement in the footnotes and the discussion of the cash flow statement in their management discussion analysis or mdna section let's get started 3M statement of cash flows is on page 51 of their annual report first thing I like to look at is this breakdown of operating investing and financing activities to see

what kind of stage or life cycle the company is in so 3M throws off about five billion of cash from operations every year it's pretty steady they have cash outflows from investing activities of about 2.6 billion every year and they also have net financing cash outflows of about two billion other than a blip in 2011 so this is sort of the classic mature company profile you've got products that are essentially cash cows they're just throwing off cash things like Post-it notes and Scotch tape things that we can't do it do without there's still re reinvesting

a moderate amount back into the company back into long-term assets and we'll look at this more in a second and they are net C outflows for financing so they don't have to borrow they don't have to raise money to fund their operations with their Investments anymore instead their operations are able to fund all of their investing activities and still throw off some cash that they can use to um pay off debt or repurchase Equity or pay dividends so just to to get some more insight into this one thing that's often good to look at is

comparing depreciation to purchases of property plant equipment again it's very rough but if you view depreciation as using up your fixed assets Capital expenditures obviously is acquiring new ones it looks like 3m's at about replacement level uh so they are investing a lot in new ppne but it's sort of replacing the things that they're using up they do have though some active Acquisitions so about a billion or so in 2012 and then there's a lot of activity with marketable Securities so they bought about 5.4 billion of 5.5 billion of marketable Securities but then they sold

or had those almost all mature within 2012 so I I think what happens is 3M is throwing off a lot of cash if they don't immediately have an acquisition in mind or immediately have uh purchase of property plant equipment they plow it into marketable Securities and Investments and then when those opportunities to make an acquisition or by PPC they liquidate the marketable Securities and use that to um go out and make their acquisition so it's almost like they're they're serving as their own bank by buying these marketable Securities holding their cash getting some return waiting

until they can invest it and then in the financing section we see a lot of the financing cash outflow is purchase of Treasury stock that's probably for stock options and then there's a big dividend that they pay to shareholders uh which again is another example often times of a mature company that if you don't have a full set of Investments that you can plow your cash back into you may as well just pay it back to your shareholders and let them reinvest it somewhere I think you're ready to do these kinds of life cycle or

growth analyses on your own so here's what I want you to do after the video is over go on the internet find a firm that you're interested in take a look at their cash flow statement and see what you can learn by looking at the companies operating investing and financing cash flows now let's dig into the operating section a bit more so we start with net income uh ignore the non-controlling interest stuff for now and just view it as net income nice steady growth in net income indicating that they are consistently able to price their

products enough to cover the cost of running the business and you know typical of a mature company you have this steady profitability that steady profitability turns into steady cash flows so very mature well performing humming along nicely company one of the big discrepancies between net income and net cash operations is depreciation ammonization now remember that's not a source of cash even though it looks like it here remember depreciation reduces net income it's non-cash so we have to add it back to get from cash to get to cash from operations fairly big number for the three

because it does a lot of manufacturing and manufacturing companies tend to have high depreciation ammonization then we have a number of other non-cash expenses so things like pensions stock-based compensation um and we have some excess deferred taxes and excess tax benefits so first the pension and postretirement contribution stock based compensation these are things we recognize as expenses now which means they're part of net income but the cash is either paid in the future as is the case for pensions and post-retirement benefits or the cash really isn't paid as it is for stock based compensation although

part of it is you're buying back treasury stock to use to satisfy options but in any case there's no cash flow this period for these expenses and we'll talk more about the stock-based compensation later on the pensions and post retirements that's beyond the scope of this course uh you'll have to come and and take my course at Wharton my elective to see more on pensions and post retirements the Deferred taxes we'll obviously get to later in the class so then we get to the section on changes in assets and liabilities these are the changes in

working capital and what we see is the big chunk here are counts receivable and inventory are negative so let's think about what that means negative number on the oper cash flow under the indirect method means that these amounts must be going up on the balance sheet counts receivable goes up as a non-cash asset to stay in Balance we have to subtract it on the cash flow statement and yes even though you can't see it I am doing up and down arrows with my hand inventories go up on the balance sheet non-cash asset going up we

have to subtract that on the cash flow statement counts payable is also going up now remember that's a liability so if accounts payable a liability increases it's on the other side of the balance sheet equation we have to increase it on the cash flow statement so these could equal these could could represent either good or bad news um bad news scenario would be our customers are not paying us we're having trouble selling our inventory we're having to stretch our payables that's probably not the case here given the nice growth and profitability that's going on and

so a more likely story is it's a it's still a growing company so during the year we're making a lot of credit sales at the end of the period we're building inventories in anticipation of future sales we uh are getting more raw materials at the end of the year in in anticipation of production and So based on other things I've seen it probably is a good news scenario that this is representing growth in working capital rather than bad news where you you can't collect receivables and you can't get rid of your inventories so overall from

the face of the statement it looks like a company that still has some growth potential now we're going to look at some other sections to try to get some additional information about what's going on with cash flows and yes while you're looking at those cash flow statements that you downloaded from the internet you should also take a close look at the operating section look at net income look at Cash operations and look at all the things that cause differences between the two to see what kind of items that you would have questions about or want

to learn more about to understand why the company's net income is different from its cash flows now I've jumped ahead to page 69 where we have footnote 6 which is supplemental cash flow information so if you remember back to the first video of the week I said that there has to be a disclosure of cash taxes paid and cash interest payments and as we talked about in I think the second last video that disclosure is there so if people want to remove cash interest and cash taxes from operating cash flow flow they have the number

so in this footnote we see the cash taxes and the cash interest so if you want to start with the cash from operations on the cash flow statement in terms of you know doing some kind of valuation to measure operating cash flow but you don't want tax or interest in there you can pull those numbers out using this disclosure one last section to look at related to cash flows is in the management discussion and Analysis which is on page 36 remember this is the the mdna is the section where 3M management is supposed to provide

their own narrative to explain what happened during the year so it'll give us more insight into some of the numbers that we saw in the cash flow statement they repeat their operating section and talk about what happened in terms of their cash flows during the year The Big Year for the big reason for the year and year increase in cash flows is net income went up um they do note that accounts receivable inventories and payables increased by 3 12 compared to increases of 484 last year but they really don't talk much about what happened with

that then at the bottom of the page they disclose free cash flow and as I said a couple videos ago this is a voluntary disclosure notice it's labeled as a non-gaap measure that means that there's no requirement by the SEC or the fby to provide this measure which also means there's no standardization companies can Define this measure however they want and and when they do that they have to alert investors and analysts that this is a non-gap measure so it's not standardized so remember free cash flow is supposed to be operating cash flow minus um

investment in the future so we've got net cash operations on from the cash flow statement as 3m's operating cash flow and then they use purchase of PPN as their measure of investment in the future investing in new property plant equipment which gives them a pretty high free cash flow and there's actually a pretty good definition I've seen a lot first um so this is a pretty good definition of free cash flow but again before you would use this number you want to make sure you know what's in the definition and that you're comfortable with it

on the next page we have cash from investing activities and what they've done here is they've netted all the marketable Securities action into a small number so instead of showing on the face the five billion they bought and then the almost five billion that they sold they just show a net number so it really highlights that the big drivers of cash outflows were purchase of ppne and Acquisitions and they tell you the ppne is expanding manufacturing capacity in key growth markets especially International like China turkey and Poland and so we can see that they are

they do still have growth opportunities and a lot of those growth opportunities see seem to be International uh for Acquisitions they refer us to note two um you can go there and look I'm I'm probably not going to jump ahead and look at that and then finally they talk about cash flows from financing activities so remember the big chunks here were proceeds from uh I'm sorry purchases of Treasury stock and the treasury stock they say is for stock-based compensation we'll talk about this later in the course but basically stock based compensation is where you award

your employees either stock options or stock grants you could either issue new stock to satisfy by that or what most companies do is they just buy back their own stock and then either sell it to employees or give it to employees under these stock-based um ownership plan or compensation plans and then the other big chunk here is dividends to to stockholders uh 3M has paid dividends since 1916 so we're almost on a 100 Years of dividends and and that's again just consistent with uh companies that are very very mature products uh throwing off a lot

of cash one thing they tend to do is they start paying dividends 3M started pretty early um not sure it was Post-it notes in 1916 and the thing about dividends is they tend to be sticky once you start paying them you always want to start pay you always want to keep paying them if you ever cut them it would be viewed by the market as bad news so that's where we find all of the cash flow information in the annual report and that's going to wrap it up for our week on cash flow statements hey

I was going to say that well this does wrap up our weeklong look at the cash flow statement I know it was difficult and there were some parts that didn't probably make a lot of sense right off the bat but the cash flow statement is a very important statement and we're going to be seeing it again and again and again as we look at more advanced topics and the more you see it the more you'll get the hang of it I'll see you next time